The stereotype of the PM endlessly poring over spreadsheets, whereas the single human being who had pre-programmed when he or she was going to make fund call based on gut and prior track record alas is out of fashion.

Fast forward to 2025 and Artificial Intelligence (AI) is not a concept of the future, but rather a vital, non-negotiable partner and change agent that all active participants are enabled by – collaboratively using it as a vehicle that transforms how financial products & services across specific segments and markets are built, managed, enhanced and orchestrated on a global basis.

In this article, Uncover the significant role of AI in portfolio management by 2025, driving smarter investments and reshaping financial strategies for investors worldwide. We will take a closer look at AI as an advanced system driving precision, mitigating risk and improving access to sophisticated financial insights.

To help you make heads or tails of how AI is making its way into portfolio management, this guide will cover the many vectors at which AI will continue to affect the space; from advanced data analytics and predictive modeling applications all the way through automated execution and personalized client solutions.

Part 1: AI’s Transformative Applications in Portfolio Management (2025 Perspective)

By 2025, AI affects every part of the investment lifecycle from initial research to ongoing portfolio adjustments. The intelligence of this is enhanced by intricate machine learning algorithms, natural language processes aided by computational power far beyond earlier times.

1. Hyper-Personalized Portfolio Construction and Customization

Fundamental AI: Machine learning, deep learning.

- Technology: Rather than simplistic risk questionnaires, AI leverages volumes of individual investor data spanning spending habits and behavioral biases to real-time financial goals, life events, and even how people feel after a market drop. It then builds, bespoke portfolios that move and shift with these individual profiles.

- 2025 Evolution: In 2025, personalization is not just about asset allocation but also tax-loss harvesting opportunities, specific ESG (Environmental, Social, Governance) preferences and even thematic investment choices aligned with your values all automated and optimized by AI. This is a big step beyond what some dub “robo-advisor 1.0.”

- For example: an AI system might detect that a client routinely invests in green energy projects and automatically recommend a drift in their portfolio toward green bonds or renewable-energy ETFs instantly tailored for their individual retirement terms and risk appetite.

2. Forecast The Market More Accurately With Advanced Predictive

Fundamental AI: Forecasting, NLP (natural language processing), Sentiment analysis and Time Series Analysis.

- Working: AI models read and analyze a huge amount of structured and unstructured data at the same time. For example, market data like price & volume, macroeconomic indicators such as GDP or nfp numbers, earnings reports from companies — (Apple Inc is reporting AAR 4/30) & alternative data sources including satellite imagery of retail parking lots, social media trends, news articles [1], and analyst reports supply chain data et al. For exploring data, we need NLP heavily in order to understand the unstructured information.

- 2025 Power: AI of 2025 easily finds hidden patterns, correlations and causal relationships in this vast volume of data It allows to spot emerging trends, to predict market shifts more precisely and even foretell the upcoming geopolitical news or regulatory changes impact on specific asset classes or industries.

- For example: an AI system could read millions of news articles and social media exchanges to spot erosion in public sentiment toward a certain sector, match that with supply chain disruptions seen via satellite, and figure rise stocks that might take a hit soon, helping managers get ahead by adjusting their portfolios.

3. Upgrading Risk Management System and Stress Testing

AI basics: probabilistic modeling, simulation, anomaly detection, reinforcement learning.

- How it Works: AI can monitor and analyze an infinite number of risk factors in real-time that human analysts could never hope to even keep track of. Market volatility, liquidity risk, credit risks, operational risks…and even the “tail risks” are all taken into consideration.

- 2025 Evolution: AI-based systems by 2025 running hi-fidelity stress testing in current space technology conditions attributing multiple economic scenarios (e.g premature interest rate spike, global recession, geopolitical warfare). These systems use reinforcement learning to gradually ‘learn’ the best strategies for reducing risks, adapts hedge sizes on a continuous shift basis so that each risk exposure is hedged against these possible downside cases.

- For instance: an AI system can detect a sharp uptick in the correlation between two disparate assets in a portfolio (an indication of higher systemic risk) and recommend that hedges be put on or the portfolio be rebalanced to lessen exposure for when markets turn down hard, all in real time.

4. Fully Automated Trade Execution, Algorithmic Strategies

AI: High frequency trading algorithm, optimal execution algorithm, reinforcement learning.

- How it Works: AI algorithms can send orders so fast and large that humans cannot, achieving factors such as price, liquidity and market impact optimization. It can help them discover short-lived arbitrage opportunities or place big orders without moving the prices in the Market.

- 2025 (Evolution): Moving beyond simple rule-based trading, AI-enhanced algorithms of 2025 are increasingly adaptable and self-learning, altering their execution strategies based on real-time market feedback coupled with micro-structural analysis. That refers not only to smart order routing, dark pool usage and slippage minimisation but also executing trades at the best possible moments and prices.

- for example: take a large institutional order and break it down into thousands of smaller trades, releasing them into the market over minutes or hours with the trades dynamically sized and timed based on current liquidity and price movements to achieve an average execution price.

5. Democratization of Robo-Advisors 2.0 (Advanced Strategy)

Core AI: Machine Learning, NLP, and UI techniques

- How It Works: AI has democratized the use of intricate portfolio-management strategies, previously limited to high-net-worth individuals and large institutions, for regular retail investors through easy-to-use digital interfaces.

- 2025 Evolution: By 2025, robo-advisors are graduating from simple ETF portfolios Some of the things they do are taxoptimization (like automated tax-loss harvesting), personalized financial planning insights, and they let you share all your other accounts which can help with stuff like re-balancing as well or even give you access to alternative investments — and all powered by AI. Many times the trigger to enter a successful wealth management is eliminated.

- Example: a retail investor with an investment using a robo-advisor receives AI-driven notifications that a recent market downturn presents tax-loss harvesting opportunities within their portfolio, and the necessary buy/sell orders to maximize their taxes are automatically traded.

Part 2: The Transformative Advantage for Investors and Financial Professionals

AI integration in portfolio management delivering solid benefits recalibrating efficiency, decision-making and client experience.

1. Resulting conclusion less emotional bias more disciplined

- Advantage: AI-driven systems work based on data and logic alone and completely get rid of human emotions like fear, greed, overconfidence etc which many a times leads to taking irrational investment decisions during volatile market conditions.

- Impact: Ensures that you adhere to your long-term investment strategies and do not start panic selling or buying impulsively, leading to more consistent and possibly superior return.

2. Unprecedented Efficiency and Accuracy

- Advantage: AI streamlines grunt work (such as data gathering, matching and regular reporting), leaving valuable human resource back in… It is faster than a human at this kind of analysis and less error-prone.

- Impact: As a result, financial professionals can now spend more time on the tasks that deliver the highest value to their organizations — complex problem-solving, relationship-building with clients, and even strategic innovation — rather than data entry.

3. Better Data Analysis and Insight Generation

- Advantage: AI can comprehend, interpret and pool together massive heterogeneous data sets (such as alternative data) to reveal invisible patterns, correlations or insights impossible for human analysis alone.

- Impact: This one gives you the important insight on market dynamics that you were uncapable of making earlier, it increases your investment knowledge and allows to more strategic investment decisions

4. Greater Risk Prevention and Portfolio Strengthening

- Advantage: AI can automatically monitor and stress test the system in real-time which keep away from risks.

- Impact: This results in stronger and more resistant portfolios that can resist a bad stock market or any other unexpected economic mess, which protects investor value.

5. Improved Personalization and Client Engagement

- Advantage: AI enables the construction of very precise, personalised portfolios and financial advice for each client based on her unique situation, targets, and investments habits.

- Impact: This results in a more personal, and interactive client experience leading to better relationships (possibly higher client retention rates for financial advisors).

6. Democratizing Sophisticated Investment Strategies

- Advantage: AI-powered platforms and robo-advisors democratize advanced investment strategies previously only available to the ultra-rich for an expanded range of investors at a lower cost.

- Impact: This creates a more level playing field and makes the application of professional-grade portfolio management accessible to more individuals in their journey towards optimal wealth creation.

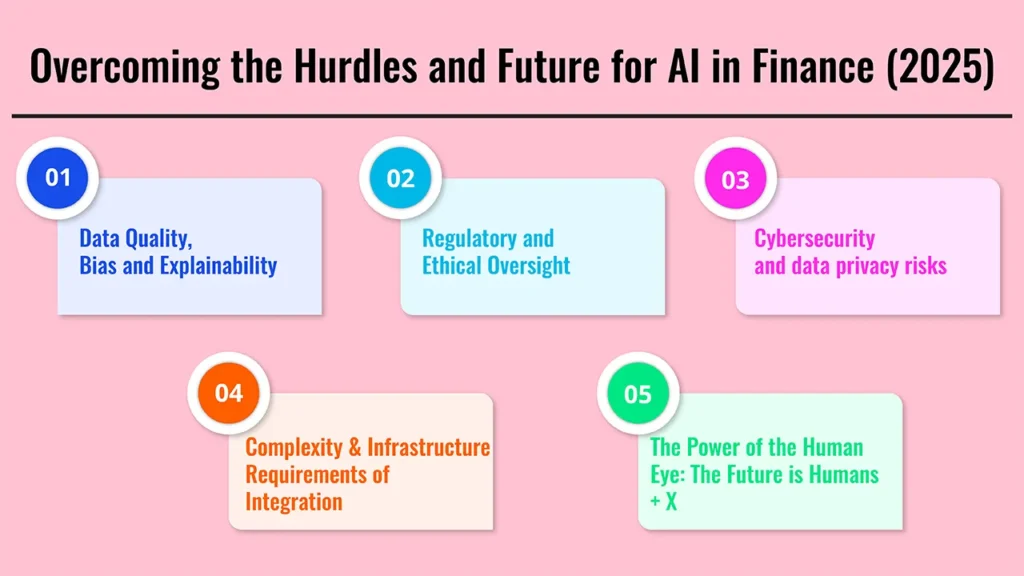

Part 3: Overcoming the Hurdles and Future for AI in Finance (2025)

Though AI possibilities are vast, the road to its ubiquitous use in portfolio management is full of bumps and potholes that must be managed as AI capabilities grow.

1. Data Quality, Bias and Explainability

- Problem: AI models are by design reliant on data for which they were trained. If this data is incomplete, incorrect or biased (by social biases for instance) then the AI’s outputs may just be a perpetuation of such bias, in the worst case: leading to unfair or suboptimal investment decisions. In addition, the decision process of deep learning models is complex and can function as a “black box”, which means it might be hard to disentangle why one investment or another was recommended.

- 2025 Look-ahead & Solution: The industry is heading toward an epoch where Artificial Intelligence that explains its decision making has become significant — i.e. explaining AI (XAI); designing models to lay out the clear rationale behind their recommended output. Greater emphasis is also on robust data governance, cleaning and auditing to reduce bias. And regulators are starting to require it, at least in finance used so far AI models.

2. Regulatory and Ethical Oversight

- Problem: Current regulatory frameworks might not catch up with the blistering pace of AI advancement. But even as these initiatives gain in popularity, the question of who will be held accountable for AI failures remains open, the ethical consequences of automated decision-making need to be addressed and everyone deserves a fair process when investing. As such, various jurisdictions globally are working to launch their own set of rules vying for a complex global regulatory environment.

- Looking Ahead to 2025 & Ideas for a Solid Roadmap: In the year 2025, we hope to have stronger regulators, an army of industry and AI developers giving up working in silos (sharing benchmarks and around guidelines as higher good) having contributed knowledge on limitations and harder lines proven too —to help guide deployment boundaries.

3. Cybersecurity and data privacy risks

- Challenge: The AI systems are built to have access to vast quantities of sensitive financial and personal data by their very nature. With the mounting level of sophistication in cyber threats and an aggregation, centralization of data has become nothing but a liability. If broke, AI rendering could ruin firms and all their clients.

- World In 2025 & Techask Solver: AI technology security solutions are on the rise. Such as enterprise-grade encryption, high-level security practices, live threat intelligence and AI-based anomaly detection for your internal systems. Ensuring the proper compliance with international standards on data privacy (like GDPR, CCPA or India’s Digital Personal Data Protection Act, 2023) is vice as like necessity for AI based solutions adoption.

4. Complexity and Infrastructure Requirements of Integration

- Challenge: Deploying state-of-the-art AI solutions into legacy financial systems is a challenge and can involve significant costs in both time and money. Most legacy systems at financial institutions were “programmed” so long ago that real time AI on a mass data scale was simply not possible.

- Cloud-native AI solutions, API-first In the 2025 outlook & solution: cloud-native AI solutions and API-first approaches have been empowered to integrate in a more flexible way at scale. Banks are spending big to overhaul data infrastructure and embrace hybrid cloud for AI workloads What are increasingly common as well, in order to close the gap of internal capabilities financial AI, is partnerships with FinTech companies focused on particular niche areas within AITech.

5. The Power of the Human Eye: The Future is Humans + X

- Challenge: AI is good at processing and managing data to identify patterns but it does not possess human intuition, empathy or the capacity to handle real ‘black swan’ events well beyond levels of factual data/comparison over time. The heavy usage of AI without some human interference can cause a lot of dangers.

- Some specific solutions provided include: 2025 Outlook & Solutions: The prevailing wisdom of 2025 is that AI is an augmentative technology. That is because the human PMs are essential not only for strategic oversight, translating the AI in a broader economic and geopolitical context, handling with clients both to understand their interests and better exposure it (this subject had been analyzed in our research as well), but they will be also responsible for adding an ethical compass.

Conclusion

Fast forward to 2025 and Artificial Intelligence has irrevocably revolutionized portfolio management, providing unique insights in prediction methodologies, tailoring of portfolios actions, risk protection and execution of low cost trades.

These strategies not only rival those available to institutional investors, but as well serve to remove exclusivity barriers that have historically existed within the retail investing realm. However, the road is not easy — it requires a lot of effort put into data quality, ethical considerations, regulatory clarity and strong cybersecurity aspects — but we are now past the inflection point for AI in finance.

Tomorrow’s best investment strategies will combine the power of sophisticated AI capabilities and human judgment that cannot be replicated. Together, this collaborative future means more durable portfolios, a better and more seamless end-client experience, and a global financial system that is not only faster but smarter.

Call to Action

Ready to Dive into AI on your investing journey? Learn about how AI-driven tools and products can improve your own financial decision-making, or contact an advisor using some of these new technologies. Know more about the changing financial technology world to Invest in future technologies.

Frequently Asked Questions

1. AI is going to replace human portfolio managers in 2025?

2. A desirable alternative data and how artificial intelligence use it in portfolio management?

Data is then gathered from multiple sources and AI leverages advanced algorithms to assess this vast quantity of unstructured data and generate specific insights surrounding the same; inferences, that might get away even with traditional kind of data.