Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A mortgage is, for many Americans, the largest debt they’ll ever carry, one that usually takes 15 to 30 years to pay off. Across those years, so much can change about your finances and more generally about the economy as a whole. what once was a savvy, low-cost loan may not be the best fit now.” Enter the mortgage refinance.

Refinancing is a financial strategy that involves taking out a new mortgage to replace your existing loan — with new terms. The primary reason is to better your financial situation, be that by lowering your monthly payments, reducing your total interest paid, or tapping into the equity you’ve built in your house.

In this complete guide, we’ll cover all the basics you need to know about How to refinance a mortgage, including the process, the different types of loans and the crucial factors you should consider to determine whether refinancing is the best move for you. When you finish, you’ll have all of the information you need to decide what is the best way for you to secure your financial future.

A refinance represents paying off an existing loan with a new one. Consider it a reset for your mortgage. You are not selling your home; you are selling the debt on your home. This new loan is secured by the same property, but with a new interest rate, a new loan term (the number of years over which the loan must be paid back) and possibly a new principal balance.

You may obtain a refinance with your existing lender (rarely) or with another lender, and that’s why shopping for the best mortgage refinance lenders is a key part of refinancing.

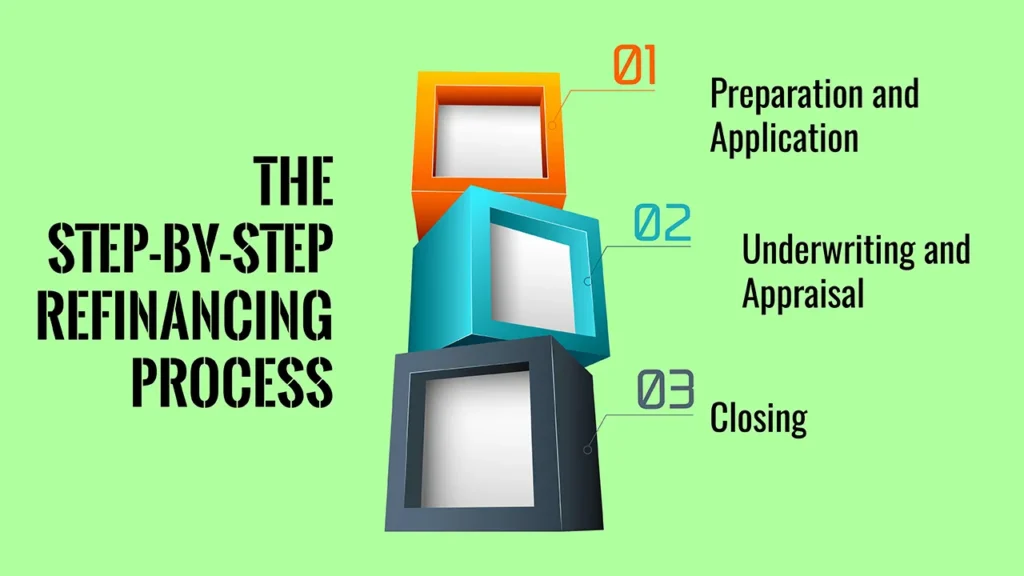

Although the process feels much like purchasing a house, refinancing is generally faster and requires different documentation. But here’s a closer look at what you can expect.

The goal of this is to organise your finances. Be sure both sides bring all necessary paperwork, such as recent pay stubs, statements on bank and investment accounts and tax returns for the past two years. You’ll also have to have a copy of your current mortgage statement.

Now, it’s time to go shopping for a new loan. Shop around Talk to multiple lenders — banks, credit unions and online mortgage companies — to compare offers. Look not only at the interest rate, but at the Annual Percentage Rate (APR), which includes interest and fees, to get a clear sense of the total cost. After you select a lender, you’ll submit a formal application.

This is the verification phase. Your income, assets and debt-to-income ratio will be verified by the lender’s underwriting team when they look through your application and all the documents you submit. They want to be confident that you will be able to afford the new loan.

One of the most important elements of this stage is the home appraisal. The lender will request a professional appraisal to establish the current market value of your home. This is an essential step, since mortgage lenders will not approve loans for a home that is worth more than it’s valued at. If your home has increased in value since you bought it, you might have more equity to work with, which is crucial to a cash out refinance.

Once all your documentation is in and the appraisal is done, your lender will issue a final Closing Disclosure. The new loan’s fee and cost schedule is spelled out in this paper.

It’s important you read this thoroughly and compare it to the original loan estimate. When you’re ready you’ll sign the new loan docs. The new loan will, in turn, pay off your old mortgage, and your new loan term and monthly payment will start.

The kind of refinance you should look for will depend on your financial goals. Here are the most popular choices:

This is the most common form of refinance, and is used to either change your interest rate or the loan term. It doesn’t permit cash-out refinances.

A cash-out refinance is a type of mortgage that allows homeowners to convert a portion of the equity in their home into cash. With such a loan, the borrower takes out a new, larger mortgage than the existing one and takes the difference in cash.

A lump sum of cash is given to you in the difference. It is often used to pay for large expenses (like home renovations), to pay for a child’s college education, or when homeowners are consolidating debt.

If you took out a government-backed loan, you may qualify for a special type of refinance.

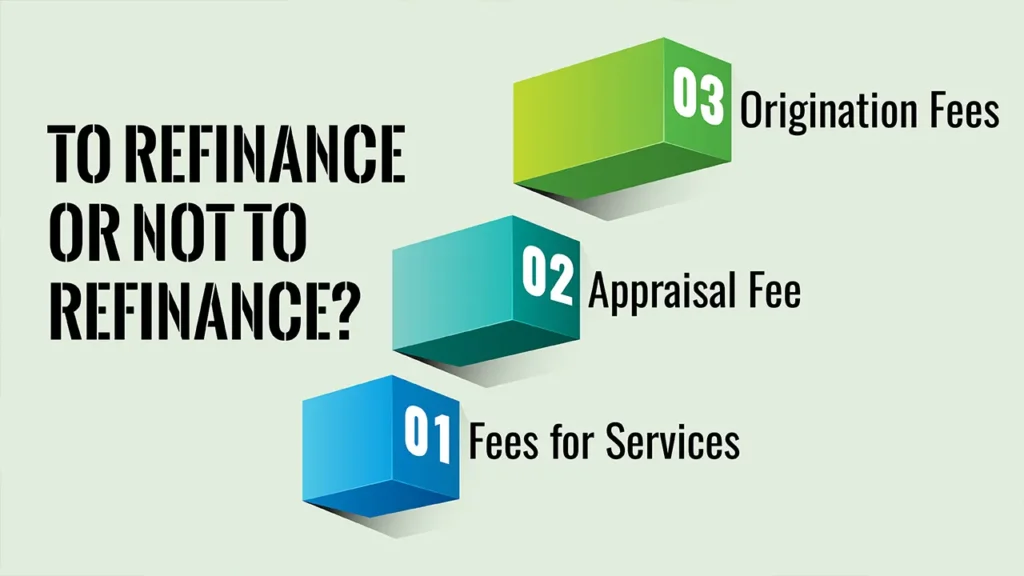

A refinance is not free. You will have to pay closing costs, which typically run 2 percent to 5 percent of the total loan amount. These costs often include:

To figure up whether a refinance makes sense for you, you have to calculate your break-even point. It’s the point at which the money you’ve saved from the smaller monthly payments balances out the closing costs you paid.

If you intend to live in your home past the break-even point, then a refinance makes sense in the long run.

A typical inquiry is whether you should get a cash-out refinance vs. home equity loan. Two different financial products they are.

Let’s see the advantages in an example.

Through refinancing, the homeowner is able to reduce his or her monthly payment by $360. To find out the break-even point: $5,000 (closing costs) / $360 (monthly savings) = Common core……. ~14 months.

That means that a bit more than a year on, there will be a net gain from the monthly savings to cover all that you paid in closing costs.

A mortgage refinance is a financial weapon that helps you to adjust to market changes and your own individual circumstances. It’s a strategic one that can make your debt work for you and put you on firmer financial footing in the future.

By knowing what it is, how it functions, and when to choose it, you can make well-informed choices that keep more cash in your pocket and provide you with a little more financial peace of mind.

It’s tougher to refinance with a bad credit, but not impossible. Your best bet is instead to work on improving your credit score. Or, you could consider FHA or VA loan refinancing, which tends to feature more lenient credit requirements.

The lowest credit score for a refinance depends on the type of loan and the lender, but you can expect a minimum score of 620 for a conventional loan. The lowest rates are usually reserved for people with a score of 740 or higher.

Yes, you can. In fact, it is a good idea to comparison shop and get quotes from several lenders to make sure you secure the best interest rate and most favorable fees.

You’ll want documentation to prove your identity, income (pay stubs, tax returns), assets (bank statements) and your existing mortgage details. Precise needs differ but these are typical.