Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Find out how to make a plan for paying off debt that suits you. Get effective strategies to manage your debt and regain financial control. Start today!

Do you feel like you’re stuck in debt? The road to financial freedom may seem far off, but it’s closer than you think. Debt management Lots of people struggle with debt, and it can be daunting.

Nevertheless, a system of paying back debt on time and regularly is also the most effective method of “How to Create a Debt Repayment Plan That Works” and securing your financial viability.

Not only does a solid plan alleviate some of the stress, but it also expedites your path to being debt-free. In this post, you can walk through exactly how to create an individualized and useful plan to knock out your debt.

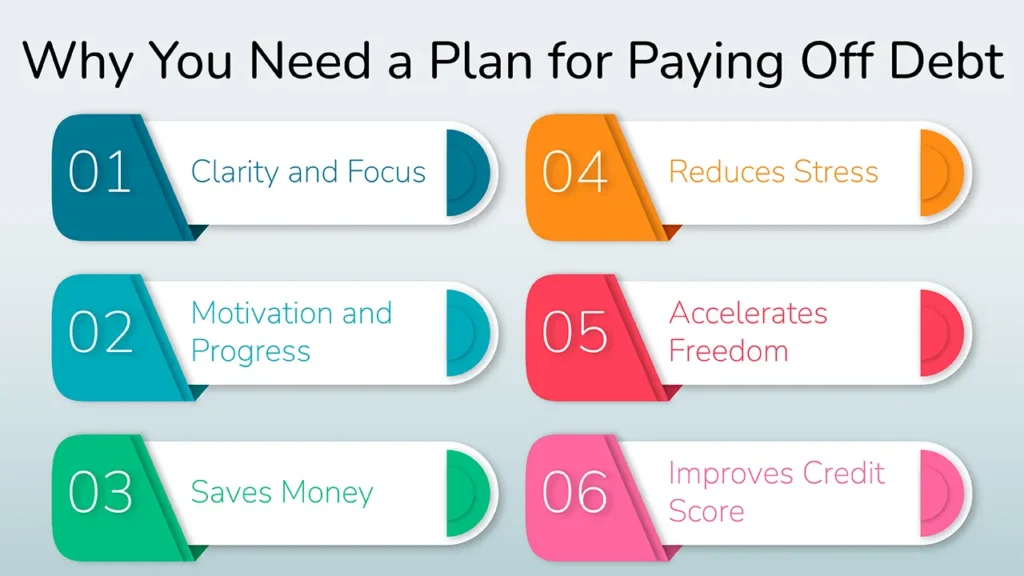

Several reasons why you need a structure for a debt repayment plan:

The guidance of a plan evenly distributes the payments and allows you to focus on what to tackle next, rather than making aimless payments.

So to see the plan on a sheet of paper and to track your progress in such detail, allows you to be disciplined, it allows you to stay motivated and stick with your goals.

By choosing to pay off loans in the best order possible, you can cut back on the amount of interest you end up paying over time so that you will save some money in the long run.

A clear plan can turn feelings of being overwhelmed into a sense of being in control of your finances.

A plan will help you get out of debt faster, so you can move on to other goals.

Credit cards are ideal for building your credit score since regular, on-time payments help increase your credit score and may grant you access to better financial services in the future. For detailed information on how payments affect your credit, see the Consumer Financial Protection Bureau (CFPB) on credit reports and scores.

The first step toward formulating a debt repayment plan is realizing where you stand with your debt.

Make a complete list of your debts, including:

Categorize your debts into categories:

Total all the balances to get your total debt load.

Organize it neatly on a spreadsheet (Google Sheets/Excel).

Here’s a very simple table:

| Creditor | Current Balance | Interest Rate | Minimum Payment | Due Date |

|---|---|---|---|---|

| Visa | $2,000 | 18% | $50 | 15th |

| HDFC Bank | $5,000 | 12% | $100 | 20th |

| Student Loan | $10,000 | 5% | $150 | 25th |

Spend some time doing your financial homework, as this will help you come up with a plan that works to pay off your debt.

Determine how much money you’ll take home each month, being sure to include everything from predictable side money streams.

Categorize your expenses by:

You have to give yourself a sense of where every single dollar went over 30-60 days.

Certainly, allocate money to all of your categories and identify “spending leaks” – places you can cut back without feeling major deprivation. The idea is to recapture extra money you can use to pay down debt.

Find out how much extra cash you have available to throw at debt, over and above any monthly minimums. This reserve will be pivotal in repaying the credit.

The right approach is paramount to paying off debt.

An “in the pocket” strategy is also great for tuning in your motivation and clarity, focusing on one debt at a time (after minimums).

Example: You may focus on paying the $500 loan first if you have three debts of $500, $1,000, and $2,000.

Example: If you have 20%, 15%, or 10% interest debts, the 20% debt should be paid off first.

Choose the system that’s best for you depending upon your financial profile and psychological preference.

Now that you have a plan, it’s time to put it into action.

Never miss any minimum payments by enabling automatic payments. Also, establish transfers to the targeted debt to happen automatically each month from your “debt acceleration fund.” This minimizes a certain degree of human error and generates consistency.

Find ways to earn more money:

Any extra rupee will be used for your targeted debt.

Beyond any short-term contract, I would also expect temporary extreme measures, such as “no-spend challenges” or preparing every meal at home.

Warning: Only combine if you’ve dealt with the underlying spending issues.

Your debt payoff journey is a continuing process that needs frequent checks and balances.

Set up a monthly or quarterly review to check in on your progress. Update your debt inventory spreadsheet and cheer each time you pay a debt off!

As you pay off debts, your minimum payments also decrease, which will free up more money for your next debt. Be flexible and modify your budget as life changes happen (like job changes, and new family members).

Picture their freedom from debt and then tell an accountable friend or your spouse about what you just did. Don’t be daunted by setbacks; concentrate on getting back on track fast.

When you hit debt freedom, it’s very important to stay on the right financial track.

Try to have at least 3-6 months of living expenses saved in order to avoid taking on new debt from unexcepted expenses.

Rechannel payments for old debt instead toward wealth-building investments, like retirement accounts or investment funds.

Concentrate on new goals, such as a home down payment or funding college.

Keep budgeting, tracking expenses, and spending consciously to maintain your financial health in the long term.

In summary, having a debt pay-off plan is one of the most significant steps to ensure financial independence. Awareness of your debt, analysis of your financial planning, executing your plan, and constant review of your plan will keep you from getting buried in your financial future.

Debt is a journey, and just getting control is the most important part of it all. Begin building your plan now, even if Step 1 is all you can accomplish at the moment. The enjoyment of financial peace and the prospects that debt freedom offers is well worth the work.

A debt repayment plan is a schedule for the payment of debts, which specifies how much you can pay and when you’ll make the payments.

The snowball approach is all about breaking the smallest debts first (debt snowball) to gain motivation and momentum.

Look into debt consolidation if you have multiple high-interest debts and can qualify for a lower interest rate.

A debt payment plan gives focus, determination, and an organized system for getting rid of debt, ending in financial freedom.