When it comes to investing, there are good reasons why you should know how to decide between mutual funds and ETFs. Let’s face it: You need to align your investments with your overall financial objectives and risk tolerance for the type of investment style that will be best for you.

There are two ways to diversify your portfolio using mutual funds or ETFs, though the vehicles work differently and can fit different types of investors. This primer will walk you through these two popular investment choices, outlining their details, benefits and considerations for 2025.

What Are Mutual Funds?

Mutual funds combine the money of many investors to purchase a broad range of stocks managed by professional fund managers. The primary investment of these funds is shares, whether actively or passively managed, stocks, bonds, or other types of securities, depending on the fund objectives.

Shares are generally priced daily at the NAV after the close of trading. Mutual funds provide convenience, professional management, and broad diversification and are a popular choice for those who prefer an investment approach that requires little more than monthly contributions to their 401(k) account.

What Are ETFs?

ETFs, which stands for exchange-traded funds, are pools of investments that trade like stocks on an exchange. These funds are typically indexed and passive, following particular indices or sectors, giving them transparency and low cost.

Unlike mutual funds, which can only be purchased or sold at the end of the trading day at net asset value, ETFs trade in much the same way as regular stocks, and they can be bought or sold anytime during a market day. This intraday trading ability is another reason ETFs are popular with investors who want more control over when and at what price they buy or sell.

What’s the Difference between Mutual Funds and ETFs

Comparing how mutual funds and ETFs operate and are structured can help you decide which is a better fit for you.

Feature

Mutual Funds

ETFs

Trading

Once a day at end of market; traded based on its NAV

Throughout the trading day by NAV

Management Style

Often actively managed

Typically passively managed

Minimum Investment

Higher minimum investment can be required

Can buy as few as one share

Expense Ratios

Tend to have higher expense ratios because they are actively managed

Generally lower costs due to passive tracking

Liquidity

Limited and more like end-of-day transactions

High liquidity—can trade anytime the market is open

Tax Efficiency

Less tax-efficient, taxable capital gains distribution may be passed on

More tax-efficient for buyers; ETF has “in-kind” redemptions

Diversification

Offering across asset types

Fund that mirrors a specific index or sector

Factors to Consider When Choosing

Investing Goals: If you’re interested in specific index exposure on the cheap, ETFs might hold the answer. Mutual funds may be better for active strategy and professional selection.

Flexibility of Trading: ETFs are tradeable during market hours which is useful if you want the price during the day time. Mutual funds are settled one time a day, better for regular long term buying.

Costs: ETFs typically have much lower expense ratios, but certain types of mutual funds can make sense in some strategies despite higher fees.

Tax Considerations: ETFs have fewer taxable events associated with their tax structure. Mutual funds may make more frequent capital gains distributions.

Lowest Minimum Investment: ETFs make it possible to get started with smaller amounts compared to mutual funds, which typically come with high minimum investment requirements.

Advantages of Mutual Funds:

Active management and specialisation at your fingertips

Larger variety and established options

Appropriate For SIPs

Advantages of ETFs:

Lower expense ratios and costs

Trade like any other stock during market hours

Greater tax efficiency

Which One Should You Choose?

That’s up to you and your goals. For those investors who appreciate optionality, lower costs, and tax efficiency, we believe ETFs can be attractive. If you desire professional oversight and disciplined investment selection, mutual funds may be the better match.

Final Words

Which mutual vs ETF decision to make How you decide between mutual funds and ETFs comes down to your investment strategies, sensitivity to costs, and desire for trading flexibility. Both can help you diversify your investment portfolio and grow your investments over time.

By balancing the pros and cons discussed above and factoring them against your financial goals, you’ll be able to make an informed decision on choosing between what makes the most sense for you in 2025 and beyond.

And don’t forget that speaking with a financial advisor or planner can generate personalized strategies to also use mutual funds and ETFs in tandem as building blocks for an even more holistic portfolio.

Frequently Asked Questions:

1. Can I invest in both mutual funds and ETFs together?

Yes, a lot of investors use both to achieve the right balance between flexibility and active portfolio management.

2. Are ETFs riskier than mutual funds?

Both are subject to market risk, but funds’ intraday trading can leave investors more open to short-term volatility than they may realize.

3. How do the fees on mutual funds and ETFs compare?

Expense ratios for ETFs are generally lower since they operate on a passively managed basis, while mutual funds can charge more for active strategies.

4. Can I purchase a fraction of an ETF share?

Unlike mutual funds, which generally have minimum investment requirements, some brokers offer access to fractional shares of ETFs, so you can get started investing with far less money.

5. Are mutual funds available with automatic investment programs?

Yes, mutual funds frequently work for Systematic Investment Plans (SIPs), making sure the investment is regular in nature.

The financial world looks very different than it did ten years ago, and both cryptocurrency and digital assets in wealth portfolios have become a focal point for investors, advisors and institutions.

Where they were once thought of as speculative or exotic and niche cryptocurrencies and digital assets, they are now seen as innovative investment solutions capable of diversified wealth portfolios and hedging against inflation and economic headwinds – in a world that is quickly being redefined by digital transformation.

It details how cryptocurrency and digital assets fit in a wealth portfolio and the advantages they offer, as well as some of the risks involved in investing such funds, and provides investment strategies that can help investors to fit them harmoniously among traditional investments like shares.

Understanding Cryptocurrency and Digital Assets

Cryptocurrency is a form of decentralised digital money that uses blockchain technology to manage and secure transactions. These currencies are based on cryptographic security and development decoupled from central banks. Decentralization and limited supply are the main reasons alternative currencies are so appealing.

‘Digital assets’ is a more encompassing term which encompasses cryptocurrencies, tokenised assets, digital securities and non-fungible tokens (NFTs). To put it in simple words, Digital assets are the digital means in which value is stored, transferred and exchanged, just like physical assets.

Cryptocurrency and digital assets are being increasingly recognised as part of a well-diversified investment portfolio to keep up with growth trends and competitive financial markets for both institutional and retail investors.

Why Cryptocurrency and Digital Assets Are Notable in Portfolios

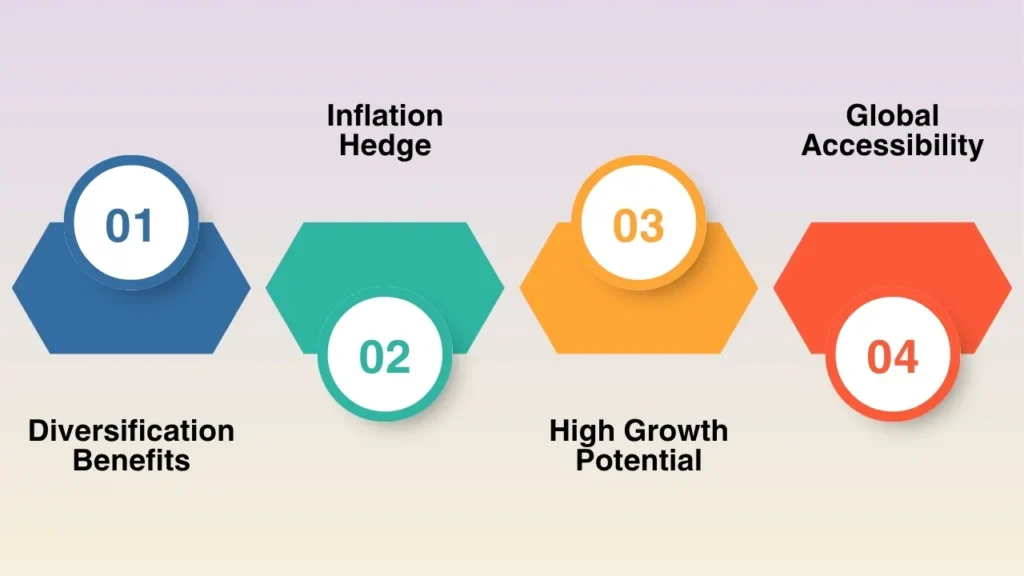

1. Diversification Benefits

Cryptocurrencies and digital assets typically have little correlation with more traditional investments such as stocks or bonds. This can decrease overall portfolio volatility and enhance long-term returns.

2. Inflation Hedge

As inflation concerns grow in many nations, more and more people turn to cryptocurrency like Bitcoin as a hedge given its limited supply and store-of-value features.

3. High Growth Potential

In a world where returns are king, cryptocurrencies and other virtual currencies are essentially bananas, both literally and figuratively. While bananas can be eaten when no one is looking, they are currently more volatile than assets that used to be banana-like (we’re talking about you, Mizuho Financial Group).

4. Global Accessibility

Digital assets are supranational, enabling investors to invest directly into various fast-paced international financial ecosystems without the need for intermediaries.

More on the Risks of Cryptocurrency and Digital Assets

There is a lot of potential in the global tech landscape, but there are also challenges.

Volatility: Cryptocurrency markets are wildly unstable, meaning that prices can rise or fall sharply in a matter of moments — and help you or hurt you way past the average market rate.

Regulatory Uncertainty: Around the world, digital assets are not regulated in a consistent manner, providing confusion for investors.

Security Concerns: Hacks, scams and fraud in digital marketplaces are not uncommon.

Absence of Historical Data: Digital assets have yet to witness long-term data that traditional investments could boast about, and this makes forecasting more complex.

It’s important to understand these risks before choosing to add cryptocurrency and digital assets into wealth portfolios.

How to Include Cryptocurrency and Digital Assets in Portfolios

Adding Cryptocurrency and Digital Assets to Portfolios: Best Practices How to Include Cryptocurrency and Digital Assets in Portfolios Investors who are considering these sorts of opportunities need to be thoughtful as they develop a strategy.

Below are approaches to consider:

1. Direct Investment

Purchasing cryptocurrencies such as Bitcoin, Ethereum and stablecoins directly on the exchanges or wallets that offer it.

2. Funds and ETFs

Some risk-averse investors may find it easier to gain indirect exposure to digital assets by simply buying a share of a fund that already holds them, while exchange-traded funds (ETFs) and mutual funds now offer players in the space indirect exposure.

3. Digital Securities and Tokenized Assets

Real assets such as real estate, equities or commodities tokenized to digital form can give access to traditional investment with the cost-benefit of blockchain.

4. Balanced Allocation

Usually, experts suggest keeping the value of cryptocurrencies and digital assets to only a small part of your wealth when other investments are factored in—usually it can range from 3% to 10%, depending on risk appetite.

5. Long-Term Holding

Viewing cryptocurrency and digital assets as a long-term value store, as opposed to yield opportunities in the short-term, can help alleviate emotion from the decision-making process.

Conventional Asset compared to Digital Asset

Feature

Traditional Assets (Stocks/Bonds)

Digital Assets (Cryptocurrency & Others)

Regulation

Well-defined and orderly

Evolving and disjointed

Accessibility

Restricted by brokerages and banks

Global and sometimes permissionless

Liquidity

High on regulated exchanges

Varies; improving with adoption

Volatility

Reasonably stable

Very volatile

Correlation

Linked to financial markets

Often low correlation to traditional

Growth Potential

Moderate, predictable

High, uncertain

This table is meant to highlight what makes cryptocurrency and digital assets so different from traditional asset classes, which is the exciting and risky part of adding it to a wealth portfolio.

Digital Assets in The Future of Wealth

Cryptocurrency and digital assets are mainstream. Latest crypto trends continue to make waves. Despite the fact that we’re better off with banking, financial institutions around the world have continued to change with them.

Institutional Adoption: Big banks and asset managers are introducing crypto services.

Regulation and Compliance: Clarity in regulation is likely to result in higher investor confidence.

Tokenization on the rise: Real assets, property or fine art for example, will be more and more tokenized as the digital asset market grows.

Technology development: If blockchain and DeFi continue to evolve, there will be many more new investment products.

Such trends underscore the fact that cryptocurrencies and digital assets are not a hype but a growing component in long-term wealth solutions.

Strategies to Manage Risks

Investors can minimize the risks around cryptocurrency & digital assets by taking a structured approach to it:

Diversify Among Digital Assets: Don’t have all your eggs (or funds) in one digital asset or NFT. Spread investments.

Safekeeping: Leverage hardware wallets and certified custodians to protect digital assets.

Continue to Learn: Continue to learn about changes in laws, technology and market trends.

Pro Tip: Work with financial advisers to retirement-plan digital assets around overall wealth goals.

Investors who weigh benefits and risks can integrate cryptocurrency and digital assets more effectively into the wealth portfolio.

Final Words

Cryptocurrency and digital assets have become a seismic shift in modern investing. Investors can, however, improve diversification, hedge against inflation and obtain growth in assets that are not available elsewhere by giving them due consideration.

But the dangers are there and victory comes from smart allocation, constant learning and proactive risk management. In wealth portfolios, the mindful integration of both traditional securities and crypto & digital assets can prepare investors for stability and growth in the new era.

Frequently Asked Questions:

1. What are cryptocurrency and digital assets?

Cryptocurrency is a decentralized digital credit card that people carry around, while digital assets are a means of representing value digitally, including everything from tokens and NFTs to securities.

2. What percentage of cryptocurrency should be in my wealth portfolio?

While the pros will always recommend you limit your exposure to between 3% and 10% of your assets, depending on your risk aversion and goals.

3. Are my digital assets safer than traditional investments?

Not higher; digital assets, however, are riskier due to volatility and lack of long-term data, though they also have more potential for growth.

4. Do digital assets have a place in the world of traditional investments?

The new age of digital assets should be something that integrates along with traditional investment. A moderate portfolio takes a mixture of both for steady resilience and growing results.

5. What are the biggest risks about the use of cryptocurrency?

Key risks include price volatility, regulatory uncertainty, hacking and lack of historical performance data.

Choose the right advisor for your financial goals. Choosing an advisor is a decision that will directly and significantly affect all of the components of wealth that you have built. As investments, taxes, estate planning and retirement strategies become more complicated, many people are increasingly turning to a professional known as a wealth manager.

If you’ve been asking yourself how to choose the right wealth management advisor, this complete guide covers everything—from what advisors do and their scope of expertise all the way through to making an informed decision for your goals.

What is Wealth Management?

Concerning Canary Wealth Management, it is a full service for individuals seeking to grow, protect and effectively transfer wealth. Wealth management, unlike simple financial planning—which can often get into budgeting or saving—is more of a much broader mentality.

It brings together investments, tax savings, retirement planning, estate strategies, insurance and sometimes even philanthropic goals under one big umbrella.

A wealth management advisor acts as your personal guide, focusing on devising not only asset-related strategies but also solutions that encompass your long-term objectives.

But Why It Matters Who You Turn to for Advice

Advisers are not all created equal. Some are investments, while for others it means very fee-based, tax-oriented wealth structuring. Choosing an ill-fitting option can cause your portfolio to underperform, you might miss valuable tax minimization opportunities, or financial planning and life goals may find themselves misaligned.

When trying to determine How to Select the Right Wealth Management Advisor, take into consideration these important characteristics:

1. Professional Qualifications

Seek those who are certified, such as a CFP (Certified Financial Planner), CFA (Chartered Financial Analyst), or CPA in the field of wealth management. Certifications show that a candidate is technically proficient and complies with industry standards.

2. Experience in Wealth Management

Wealth Management It has a weight of reality to it when accomplished investment advisors are in the house. Years of serving a variety of client portfolios give you greater knowledge around market cycles, not to mention tax planning and asset preservation techniques.

3. Fiduciary Responsibility

In your ideal adviser, you want someone who puts your best interest ahead of their own. This responsibility means your decisions are impartial and focused on only what is best for you in managing your wealth.

4. Customized Solutions

People have different tax situations, family structures, inheritance issues and business interests. A professional who specializes in creating personalized solutions will closely match his strategy to your objectives.

5. Transparency and Communication

Trust is built on transparency and regular communication, and fee disclosure is key to that. Make sure your adviser is communicating to you risks, costs and potential outcomes without industry jargon.

Types of Wealth Management Advisors

Different advisors bring different expertise. In order to choose well, you need to know what exists.

Knowing that specialization enables you to select the appropriate professional to meet your needs.

How to hire the best Wealth Management Advisor

When trying to determine how to choose the best wealth management advisor, keep in mind these steps:

Step 1: Assess Your Needs

Know your money goals before reaching out to any professional. And do you want investment advice to plan for retirement, seek tax efficiency, or transfer wealth from one generation to the next? While filtering advisors who don’t fit, the exercise aids in clarifying objectives.

Step 2: Research and Shortlist

Ask for recommendations from coworkers, friends or industry organizations. Vet professionals online via regulatory bodies and wealth management firm client reviews. Make a shortlist of 3–5 advisors after doing your research.

Step 3: Check for Credentials and Experience

Ask for licenses, certificates and professional history evidence. Make sure they have a background in wealth management that resembles your situation.

Step 4: Understand Their Approach

Inquire about how they build portfolios, handle tax efficiency or tweak financial plans in times of market stress. A philosophy of advising should dovetail with your financial comfort zone.

Step 5: Fee and Commission Models Comparison

Some charge a fixed fee, others charge a percentage of AUM, and some earn commission on products. A transparent fee schedule means that none of the hidden costs will eat away at your returns.

Step 6: Conduct Face-to-Face Meetings

An in-person meeting will give you a sense of someone’s mannerisms, how comfortable they seem to be with you, and whether or not they instill your confidence. A good relationship means better and easier future cooperation.

Step 7: Test the Waters with a Trial Period

Perhaps start with a service scope or more limited asset amount to gauge effectivity. Over time, grow it to a full relationship if they work out as you hope.

Common Mistakes to Avoid

Most end up choosing one because of impulse or not enough research. Avoid these pitfalls:

Picking solely based on brand and not research of the specific advisor.

Not paying attention to fee specifics that can decrease effective return.

Failing to check fiduciary responsibility.

Outside of this communication-style thing, big words get in the way.

Hiring advisers who are specialists in one area rather than the whole of wealth management.

How Advisors Add Value

What a Wealth Management advisor does for you A good wealth management advisor doesn’t just manage money; they also:

Integrate all of your financial life under one plan.

Provide strategies tailored to each individual circumstance based on level of risk.

Discipline retail investors when the market is hot and cold.

Stay up on regulatory changes that affect taxes and estates.

Develop a plan to transfer wealth in an efficient way.

Final Words

The ability to choose the right wealth management advisor is a matter of recognizing needs, evaluating expertise, and making certain values and goals are aligned.

These relationships, based on trust, openness and a plan that addresses future needs for generations—not just the next year or decade—can help secure and extend your financial success.

So with a little bit of reasoned consideration, you can choose the right wealth management partner and feel comfortable that your future is secure.

Frequently Asked Questions

1. What is the minimum amount for Wealth Management?

There is no hard and fast minimum, although many firms have a client base that includes individuals with at least $250,000 in investable assets. Yet even smaller investors taking a look at complex strategies can gain.

2. How can I determine if an advisor is trustworthy?

Look for fiduciary responsibility, professional credentials and memberships in regulatory bodies. Reviews, recommendations and references can also provide reassurance.

3. Which fee structure do I want to be on?

I prefer the flat fee or AUM (percentage-based), as they are more clear. Avoid models that are commission-based relative to product sales.

4. How is wealth management different from traditional financial planning?

Yes. Whereas financial planning often involves short-term budgeting and saving, wealth management focuses on longer-term investment, retirement, and tax and estate planning strategies.

5. How frequently should I revisit my plan with a professional?

Annually, if possible; or after moments of significant life or economic change. Periodic reviews ensure strategies are adapted to the realities on the ground.

The decision to select a wealth management firm is among the most important choices anyone and their family members will ever make with regard to ensuring their financial future. A wealth management company offers a collection of services that go beyond just investment management and include retirement planning, estate planning, tax efficiency and risk management.

There are so many vendors today that it can be very confusing if you don’t know what you’re looking for in terms of your financial needs, lifetime aspirations and the characteristics to target in a professional partner.

This article explains how to choose the right wealth management firm and considerations to look for, as well as steps you can take to ensure you make a wise decision.

Understanding Wealth Management

What is wealth management? It goes beyond investment advice to offer personalized financial planning, estate planning, philanthropy, retirement coverage, tax strategies and risk management. Unlike old-fashioned financial services, wealth management is holistic: rather than concentrate on specific products like an individual financial product or service, it considers all areas of the client’s financial life.

The right wealth management firm is critical for long-term success because, if you lead a complex financial life (or are planning to), including owning your own business, having a high net worth, or, most importantly, having family multi-generational wealth transference, at some point you will benefit from having access to a professional viewpoint that can bring clarity and vision.

The Importance of Selecting the Correct Wealth Management Firm

When you have a working relationship with a wealth management company, you are entrusting them with your future and that of your family, as well as the most personal areas of your life—finances. The right firm ensures that your wealth creation is in line with investment strategies and also provides customized tax and estate planning.

Selecting the wrong firm, however, could mean bad decisions or too-high costs or strategies not in harmony with your risk-taking and/or principles.

Here are a few reasons why it’s such an important choice:

Safeguarding your long-term wealth growth.

Stabilizing the volatile financial markets.

Optimizing tax-efficient strategies for better return on your investment.

Constructing a bucketed financial plan appropriate for personal and family goals.

Preventing conflicts of interest by contracting with transparent firms.

Key Factors to Consider

There are several key issues you need to consider when assessing a wealth management firm:

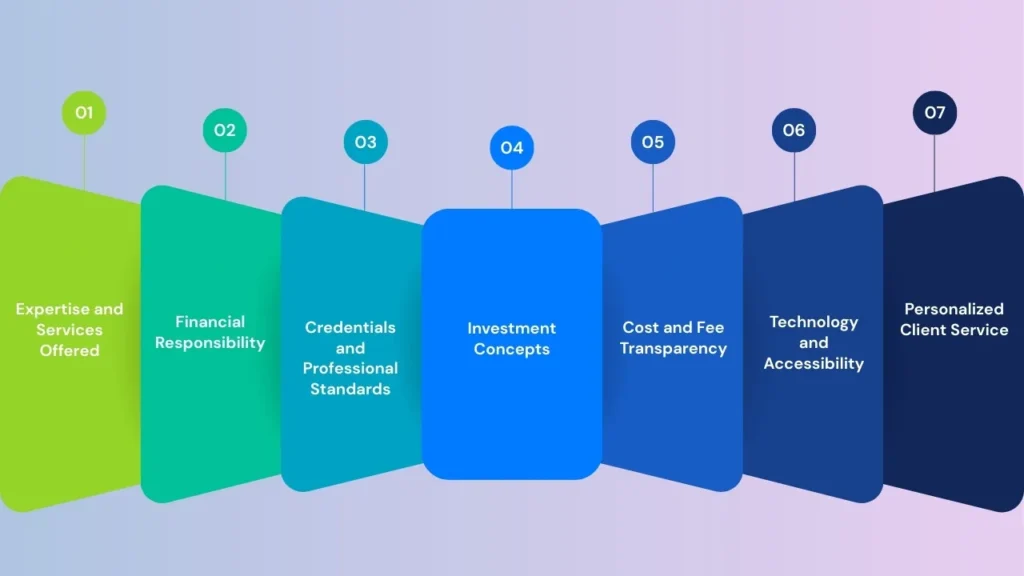

1. Expertise and Services Offered

Each wealth management firm does things differently. Some may concentrate more on investments, while others might have a more robust offering, including tax planning, estate planning, insurance analysis or business succession strategies. Inquire if the firm focuses on serving clients with needs similar to yours.

2. Financial Responsibility

The top factor to look for in a money management firm is if it works as a fiduciary. A fiduciary has a legal duty to act in your best interest, not theirs or their firm’s. This is so product recommendations aren’t motivated by commissions but instead are in your best interest.

3. Credentials and Professional Standards

Find companies with advisors that hold reputable designations like CFP, CFA, or CIMA. These titles reflect expertise, education, and ethical responsibility.

4. Investment Concepts

Every financial advisor has its own investment philosophy. Some can be aggressive in nature, geared toward growth-oriented strategies; others may promote risk mitigation and stable growth for the longer term. Realizing if the strategy they purport to follow is in line with your risk level is very important.

5. Cost and Fee Transparency

Wealth management fees vary. Some do it as a percentage of assets under management (AUM), others as flat fees, and still others via commissions. Compare costs and make sure you understand all existing charges before signing anything.

6. Technology and Accessibility

A modern approach to wealth management also means the use of digital dashboards and data analytics in financial planning with information available online. A company with sound technology brings you the ability to monitor your portfolio and financial planning in a more effective manner.

7. Personalized Client Service

Wealth management is not “one-size-fits-all.” A great firm spends time getting to know your unique goals, values and lifestyle. Evaluate if the firm is providing personalized strategies and enabling regular communication with an advisor.

Wealth Management Fee Models Compared

Fee Model

Description

Pros

Cons

Assets under Management (AUM)

A percent on what’s in their portfolio charged annually

Same success as the firm with your portfolio growth

May get expensive as you grow

Flat Fee

Fixed amount paid annually/quarterly

Predictable and easy to understand

Bodyguard against size of wealth changing

Hourly Fee

Pays only for time and advice

Open and fair, no hidden commissions

Can be unpredictable based on issues

Commission-Based

Advisors earn from selling products.

Might seem cheaper upfront

Risk of pushing product, conflict of interest

Here, you can get a good feel for why we consider it so important to know how much fees are going to cost.

Choosing the Best Wealth Management Firm—A Step-By-Step Approach

Instead of jumping, consider taking these steps for some clarity:

1. Identify Your Needs

Start with some clarity: estate planning, retirement planning, tax efficiency or plain old investment management? Your need determines the firm you select.

2. Research Potential Firms

Check out online reviews, industry rankings and peer recommendations to narrow down your list of firms. Be sure to watch for specialization, types of service & focus on clients.

3. Interview Shortlisted Firms

Treat this process like hiring. Inquire about experience, the financial planning process, and wealth management philosophy. Focus on transparency and responsiveness.

4. Assess the Advisor-Client Relationship

Since wealth management is so much about clarity of communication, meet the advisor and find out if they understand and sympathize with all your requirements.

5. Check Regulatory Compliance

Ensure that the company is registered with all regulatory authorities and it complies with regulated standards. This protects your financial interests.

6. Evaluate Technology and Innovation

Leading-edge wealth management firms tend to offer sophisticated performance dashboards, timely reporting and proactive analytics.

7. Understand Succession and Continuity Plans

Wealth management is a long-term commitment. Make sure the practice has a succession plan in place so your strategy stays intact even when your lead advisor retires.

Common Mistakes to Avoid

Selecting on reputation, rather than fit.

Failing to account for hidden charges or commission rates.

Neglecting to consider how much the firm lines up with your personal financial philosophies.

Failing to require the firm to be held to fiduciary standards.

Not comparing at least three financial firms to select the one that best meets your wealth management needs.

Final Words

When you partner with a wealth management firm, you don’t just give them your portfolio—you trust that they are helping to secure your financial future for generations to come.

Having clarity on your FPU/financial goals along with doing proper research would have prevented you from choosing a partner who does not share the same values as you do. Thinking about fiduciary responsibility, fee transparency, investment philosophy and personalized service prepares you for long-term financial success.

Frequently Asked Questions

1. What does a wealth management firm do?

A financial advisory firm that offers comprehensive financial services such as investment advice, retirement planning, tax and estate planning, or specific goal-based solutions for individuals or families.

2. How can I tell if a wealth management firm is reputable?

Seek fiduciary status, professional designations, regulatory scrutiny and favorable reviews. Another aspect of trustworthiness is communication and fee transparency.

3. How much money do you need to have for wealth management services?

Enter different companies at various points. Some serve high-net-worth individuals; others provide services for professionals just starting to accumulate wealth. In general, most companies have minimum investment amounts that can be as low as a few hundred thousand dollars.

4. What is the distinction between a financial advisor and a wealth management firm?

An investment counselor usually provides investment advice. A good wealth management firm offers a wide range of services with the full spectrum of financial categories—investments, taxes, estate planning, philanthropy, and legacy planning.

5. How can a wealth management firm assist with tax planning?

Yes. More than a few provide tax-planning-oriented wealth management solutions aimed at helping you save income, capital gains, and estate taxes in the most effective way possible.

Establish automatic transfers from your chequing account to a savings account and a broking account on payday. A rule of generality is that you should be saving at least 15% of your income, but you can start at a lower percentage and increase it over time.

As for automatically doing this, it ensures the better part of your pay cheque is disciplined each month, removing the temptation of that money you didn’t even have the time to miss yet. This small act of automation is a departure from saving what’s left to creating wealth first.

Here are the 5 Smart Moves to Grow Your Wealth Beyond Your Salary

1. Invest in Yourself (Your Person)

Your best asset isn’t your stock portfolio or your pile of real estate — it’s your earning power. The only way to make wealth grow is to keep investing in your skills, knowledge, and network. This can be even more powerful than any investment you could make in the stock market, because it adds directly to your baseline earning potential.

Think about getting a certification in a new skill, going back to school for an advanced degree or going to industry conferences to develop your network. The investment for skills that result in earning a higher salary or are a gateway to a new career path can be exponential. Consider which skills are in demand in your industry and come up with a plan for developing them. Your own future salary is the most potent wealth factor you control.

2. Use a Side Hustle or Passive Income Source

One salary, one highway to wealth. If you have a side hustle or a passive income stream, you have the opportunity to speed up the process and make your journey a nonlinear one. It is an essential step for anyone who wants to expedite their path to financial planning.

A side hustle is intended to be an active income source that’s beyond your 9-to-5. This could be freelance writing, starting a web design business, or selling things online. A side hustle both provides you with more cash to save and invest and is a great place to learn the ropes of business.

3. Leverage a Side Hustle or Passive Income

Passive income is income that requires little to no effort to earn. This could be a royalty from a creative project, rental income from a piece of real estate or dividends from a stock portfolio.

So, many passive income streams can be lucrative with investments of time and money upfront; others would be better served with more modest investments and are established more on the “get rich quick” rather than the “slow and steady” idea of income generation.

4. Embrace Strategic Investing

Now that you have your automatic savings in place, it’s time to do something with that money. Allowing your money to sit in a traditional savings account is a losing bet against inflation. Strategic investment produces a growing amount of money, and when you do that, the money itself accumulates more money over time due to the power of compounding.

Begin by investing in a broadly diversified portfolio of low-cost index funds or ETFs (exchange-traded funds). These funds are broad market-focused and offer an easy way to begin. As you grow more comfortable, you might look to other asset classes, including real estate (via REITs or direct ownership), bonds or even private equity. The trick is to begin early and be consistent so that investments can grow and work harder than your salary alone.

5. Minimize Debt and Unnecessary Expenses

You can’t build a powerful financial house on a weak foundation. High-interest debt, including on credit cards, is one of the biggest wealth destroyers. Before you can start constructing, you’ve got to put an end to bleeding money in interest.

Establish a high-interest debt repayment plan where you attack to pay aggressively. Focus on the cards with the highest interest rates to pay off debt fastest. At the same time, scrutinise your expenses. Trim superfluous subscriptions, dine home more often and seek savings on your monthly bills.

Blood and Tears Once you come to terms with this reality, however, you become better at finding ways to keep that money in the bank for as long as possible. Every dollar you can keep from being sucked into the quicksand of spending, basically, is a dollar that you can use to service your financial goals, whether that’s chiselling away at debt or investing in your future.

Conclusion: How to achieve financial freedom

Generating wealth over and above your salary is no pipe dream; it’s not only possible but a doable goal and can be approached in a strategic way.

All it takes for a financial engine to work for you is to automate good financial behaviours, invest in yourself, establish new income streams, practise strategic investing, and minimise debt in order to have the strongest financial engine possible.

The following five moves are not quick fixes but indispensable pillars of a financial life built on independence, resilience and growth.

Frequently Asked Questions

1. What’s the right amount to save from my pay cheque?

The generally recommended figure is 15% of your pretax earnings. If you have other goals, like buying a house, you may need to save more.

The best strategy is to start with what you can and then continue to raise your savings rate each time you get a raise.

2. What’s the difference between a side hustle and a passive income stream?

It’s more like an active income — these websites explain a side hustle as “side work” that’s done apart from your day job but earns you money, per hour or entire project.

A passive income source, by the way, is one that takes this active involvement, adds it for a while, and afterwards doesn’t have the same level of maintenance or work thereafter (such as an investment that continues to pay off).

3. Is the stock market an okay bet?

The stock market is risky, but over time, it has outperformed any return you would get from a traditional savings account.

You also can mitigate risk by diversifying your portfolio and investing for the long term, thereby allowing you to ride out short-term market swings.

When people hear what is wealth management? beyond just investing, many people picture a stockbroker on Wall Street with their only focus covering buying and selling stocks for the ultra-wealthy. Investment management is one important part of the equation, but it’s not the whole enchilada.

Real wealth management is a far more comprehensive and holistic offering that encompasses all elements of a clients financial life. It’s also about developing a comprehensive long-term strategy that transcends simply growing assets and that includes protecting them, minimizing taxes and planning for the future.

It’s a dedicated partnership, here specifically to help you meet your most important life goals, rather than generate market returns. So what if the current The financial situation is complex and the old days of pensions and Medicare are long gone; you may have multiple retirement accounts, not to mention real estate holdings and different kinds of debt — do-it-yourself is a great way to rack up monumental mistakes.

What Is Wealth Management? A Comprehensive Strategy

In essence, wealth management is a professional service which encompasses financial planning, investment management and a wide range of other forms of financial advice. It’s made for clients who need extra attention to their financial world because of their substantial assets or more complicated financial world.

Unlike a transaction-stock broker or a transaction-only financial planner, or a one-time financial planner, a wealth manager serves as the primary point of contact for all of a client’s financial needs. They act as trusted advisors who help preserve, protect and enhance a client’s wealth for generations to come.

It is a long-term and dynamic relationship that changes with job conditions and life events and with new patterns of economic thinking.

More Than Just Investing: Key Elements of Wealth Management

Ironically, (g) one of the most critical functions of the wealth manager is to be able to coordinate multiple disciplines into a comprehensive and synergistic strategy. Here are the main ingredients, which go far beyond purchasing and selling investments:

1. Financial Planning

This is the basis of a wealth management relationship. It is a forward-thinking exercise that helps you chart your financial future. But it is about far more than just the numbers; it’s also about translating your life goals into a numbers-based financial roadmap.

A wealth manager will help you define your financial goals, which can range from saving for a down payment on a house to funding a child’s education to retiring at age, say 55, 62, or 70. They will look at your current financial position – what you have in cash flow, assets and liabilities – to create a realistic, actionable plan that is the roadmap for your financial story.

2. Investment Management

Though not the sole ingredient in the mix, investment management is an essential service. This approach helps you construct a balanced portfolio that is appropriate for your goals, risk tolerance and time-frame. A wealth manager will take the monkey work of portfolio construction, asset allocation and security selection off your hands.

They track the performance of the portfolio and, if necessary, automatically rebalance it to remain on target. In times like these, you need an advisor who can offer invaluable emotional support, helping you take a ‘chill pill’ and resist panicking, selling low and abandoning your long-term game plan.

3. Retirement Planning

A wealth manager assists you in addressing the one most important question: “Will I have enough to retire?” They do a comprehensive plan for your retirement that includes both the accumulation phase (saving for retirement) and the decumulation phase (withdrawal of your assets).

They will assist you with the intricacies of various retirement accounts, including 401(k)s, individual retirement accounts (I.R.A.s) and Roth accounts, and create a plan for taking distributions in the most tax-efficient way. The objective is to make sure your savings last a lifetime and can sustain the lifestyle you want.

4. Tax Planning

This is an area where a good wealth manager will add huge value. A proactive tax approach can mean a lot more money in your pocket in the long run and this will also contribute to increasing your total returns.

A wealth manager collaborates with your tax accountant to execute strategies like tax-loss harvesting, in which losing investments are sold to write off gains. They also provide advice on asset location, which involves putting tax-efficient investments in taxable accounts and higher-tax-rate investments in tax-advantaged accounts to optimize after-tax returns.

5. Estate Planning

This is about your legacy. The benefit of estate planning It is estate planning that will help to make sure that your assets are transferred to the next generation rapidly and exactly as per your desire.

A wealth manager can help you through this messy job, and may collaborate with an estate attorney to establish important legal instruments like wills, trusts, and powers of attorney. They can advise you on a range of trusts to protect your assets, minimize estate taxes and provide for future generations.

6. Risk Management and Insurance

Life is full of uncertainties that can throw even the best financial plan off course. A wealth manager does this for you by helping you assess your risks, and mitigate them, through an analysis of your insurance needs.

They will review your life, disability and long-term care coverage to make sure that you and your family are protected from what life can throw your way. And they can even provide businesses owners with business-specific risk management advice.

7. Philanthropic Planning

For many wealthy individuals, giving back is a top priority. A wealth manager can also assist you with structuring your charitable contributions in the most tax-advantageous manner. They can help you establish a donor-advised fund or a private foundation, enabling you to plan strategically how to give as well as how to plant your legacy.

Who Is Wealth Management For?

And while “wealth management” may sound like something that only the very rich need, the peace of mind and financial clarity you’ll get from at least a consultation on your options can help anyone who’s reached a level of financial complexity that they can no longer easily manage on their own. This could include:

Young professionals: who have stock options or a large bonus and appreciate assistance integrating this new wealth into their overall financial plan.

Entrepreneurs: who are looking to balance their personal money with the intricacies of small-business business (including exit strategies).

Families saving for several big life goals: It says, college tuition for numerous children — and want a coordinated savings strategy across various accounts.

Individuals nearing or in retirement: Those who are approaching or already retired and need a plan for turning their nest egg into sustainable income.

People who have inherited a large sum of money or received a sizable legal settlement, and are seeking advice on how to protect and grow it wisely.

At the end of the day, a wealth manager is for anyone who has ever tried to organize all of the moving parts of their financial life or house them in one cohesive, strategic plan.

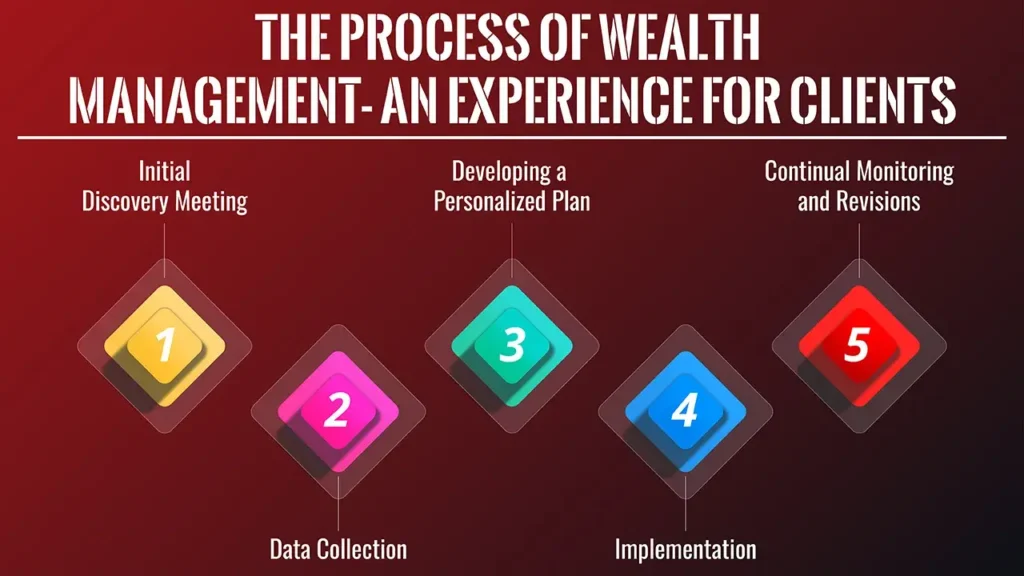

The Process of Wealth Management: An Experience for Clients

A relationship with a wealth manager is a continuous process of communication and trust. The process, in most of the cases, is as follows:

Initial Discovery Meeting: This is just a get-to-know-each-other meetings. The advisor will inquire about your financial past and your future, your values and your worries. This is an essential part of trust and rapport.

Data Collection: You provide us with all your financial, insurance, and legal documentation. Your wealth manager’s team will analyse this information to develop a full picture of your current financial position, and will highlight potential risks and opportunities.

Developing a Personalized Plan: In analyzing all of your information, you will create a personalized, comprehensive financial plan. This model isn’t a template one-size-fits-all plan, but rather a customized plan with unique investment management, tax, and other financial strategies for you.

Implementation: The plan is executed. That could include, for example, the opening of new investment accounts, the adjustment of your existing portfolio mix and working with other professionals such as a tax accountant or estate attorney to get the legal and tax aspects of the plan in place.

Continual Monitoring and Revisions: Plans are living documents. The wealth manager keeps a close eye on your portfolio and financial affairs regularly to keep it on course with your goalposts and adjust for any changes in your life or the market. Frequent check-ins, sometimes on a quarterly, or even an annual level, mean you are never left out of step with your plans.

Conclusion: A New Wealth-Full Age

Wealth management is a discipline that is intended to provide clarity and control over your financial affairs. It’s a strategy that all your assets, from your investments and your retirement accounts, to your family’s future, are working together toward a common goal.

Knowing this more integrated view, you can be more enlightened in how you take care of your finance and construct a financial future that is genuinely robust.

Frequently Asked Questions

1. What’s the key distinction between a financial adviser and a wealth manager?

People tend to use the terms interchangeably, but a wealth manager is generally a more encompassing service.

A financial adviser might specialize in one or two areas in particular (retirement planning or investing, say), while a wealth manager encompasses every aspect of a client’s financial life, including estate planning, tax strategies and insurance.

2. What do wealth managers charge?

Generally speaking, wealth managers will have an annual fee as a percentage of assets under management (AUM).

That can be 0.5-2% or more, depending on what services you get and how big your profile is. Some may also assess a fixed fee or an hourly one.

3. When should you consider engaging a wealth manager?

There’s no one answer, but here’s a good rule of thumb: Consider hiring one when your financial life becomes too complicated for you to handle on your own.

Perhaps when you have more than one investment account, when you experience a big life event or when you have an explicit need for high-order tax and estate planning.

4. Can I just manage my wealth on my own?

Absolutely, lots of people can take care of their finances well. But as your wealth accumulates and your financial life becomes more nuanced, an expert can bring knowledge and a tactical perspective that can be difficult to replicate.

And, they can help you maintain a valuable objective perspective and keep you from making emotional decisions when markets swing.

Wealth management, formerly the responsibility of the ultra-rich and delivered through in-person meetings, is undergoing a seismic shift. The emergence of advanced technology not only facilitated broader access to financial services but has also fundamentally transformed their delivery, management and use.

Technology is shifting the industry from legacy, manual systems toward a data-driven, effective and personalised future. This article will examine how technology is transforming today’s wealth management industry, from the automation of basic tasks to providing a more transparent and secure client experience.

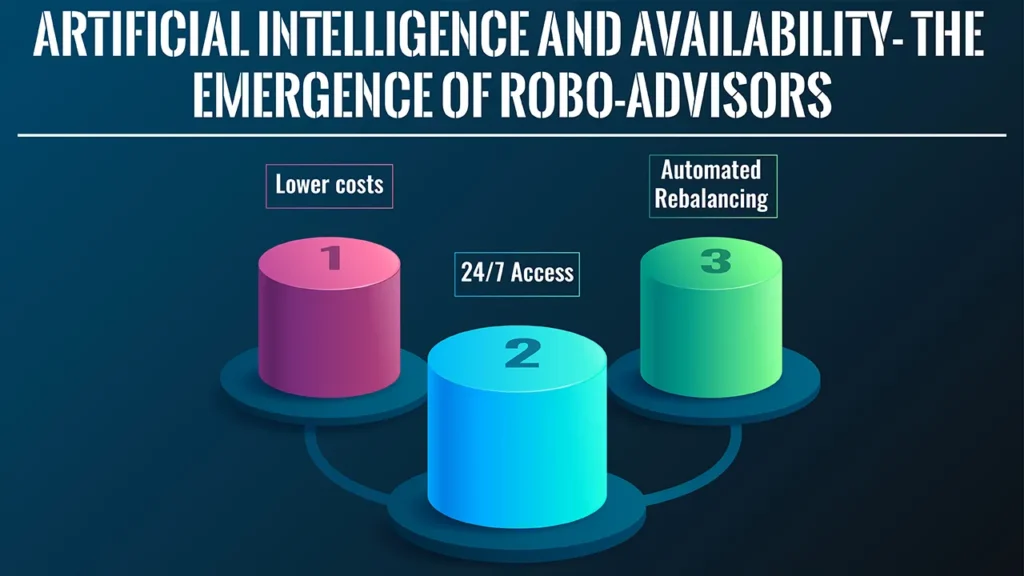

1. Artificial Intelligence and Availability: The Emergence of Robo-Advisors

Perhaps the most readily apparent sign of tech changes is the rise of robo-advisors. These are digital platforms that employ algorithms to offer computerised, low-cost financial advice and portfolio management.

Clients can fill out a questionnaire, rather than relying on a human advisor, to give details about financial goals, risk tolerance and time frame. It then builds and maintains a diversified portfolio for them.

Lower costs:Robo-advisors usually take a percentage of your assets under management, rather than charging fees based on trades; this makes professional wealth management services available to more people, including younger investors who have smaller portfolios.

24/7 Access: Instead of having to look for an adviser to make a change or get information, clients can now log in to their accounts to see how they’re doing, make changes, etc. in the middle of the night on a Saturday if that is when it’s convenient for them, instead of according to a traditional model where that would be taken away from them.

Automated Rebalancing: They assist in automated rebalancing of portfolios according to the target asset allocation so that the investor’s risk profile does not get skewed manually over time.

2. Data-Driven Decision-Making and AI

Technology has provided financial advisors and clients with a degree of data and analytical power that would have been unthinkable even a decade or two ago. Algorithms and AI can handle large volumes of data in real time and provide deep insights that help us make better decisions.

Predictive Analytics: AI has the ability to analyse market trends, economic indicators and past data to make predictions of potential market movements and recognise opportunities or risks.

Risk assessment: You can model the risk of a portfolio better than established methods, enabling better asset allocation to reach a preferred risk-adjusted return.

Behavioural Finance: Even a client’s behaviour and spending habits can be analysed by technology to provide more relevant and personal advice. For example, a platform may notify a customer of a potentially over-budget situation or recommend an optimal savings plan for the customer based on his or her behaviour.

3. Personalization and Enhanced Client Experience

Contemporary clients want a smooth, customised and potentially on-demand experience akin to what they already receive from other digital services, such as streaming platforms or e-commerce sites. Wealth managers can use technology to fulfil each of these needs and offer a tailored experience accordingly.

Personalised Portfolios: Algorithms can build highly individualised portfolios to correspond to an individual client’s specific goals, values (ESG investing, for instance), and tax considerations.

Interactive Dashboards: With interactive dashboards, clients can access a complete picture of their finances at any time, anywhere, with mobile apps and a web portal – including real-time cash flow and investment performance, opening windows of trust.

Digital Communication: Technology provides a means for clients to interact with their advisors securely and in real-time—consider secure messaging, video conferencing or collaborative planning tools.

4. Security and Transparency

Now more than ever, security is the top concern in a world which is more fraught with cyber threats. Technology has a paradoxical role here: it creates new vulnerabilities while also offering the most potent tools for fighting them.

Strong Encryption: Secure encryption protocols are now implemented by the platforms of today, meaning your clients’ sensitive information, such as personal and financial data, is safe.

Biometric Authentication: As we are already doing on mobile devices with fingerprint and facial recognition, this could provide that extra security layer, making it more difficult for unauthorised users to get into our accounts.

Real-time Transparency: Clients can see their accounts in real time, which means they can view what’s happening with their transactions and how their portfolios are performing. The transparency fostered by this enables your clients to have more confidence and control over their finances.

5. The Rise of the Hybrid Model

Technology has given life to the robo-advisors but not killed the human advisor. In its place has emerged the hybrid wealth management model.

In this structure, technology is automating the mundane administrative tasks (like data entry and rebalancing) and managing straightforward investment questions. This means the human advisor is liberated to concentrate on higher-value tasks like:

Sophisticated Financial Planning: Complicated finances such as estate planning, retirement planning and tax efficiency.

Emotional Support: Offering clients support and reassurance during times of market volatility, the kind of human touch an algorithm cannot provide.

Relationship Development: This includes developing deep, personal relationships with clients in order to have truly intimate knowledge of their long-term life goals.

The hybrid nature combines the best of both worlds, as it not only leverages the effectiveness and convenience of technology, but it also taps into the empathy and expertise of a human professional.

Conclusion: A New Financial Empowerment Age

The importance of technology to today’s wealth management is not on the verge of a decline; it’s a profound change that has already occurred. Wealth management is shifting from being an exclusive and expensive service to becoming increasingly inclusive, transparent and efficient, driven by technological developments.

Using automation, data analytics and better security, advisors can make better decisions, and clients can feel more secure and in control of a sound financial future. The digitisation of finance is indeed a golden age for finance professionals as well as their investors.

Frequently Asked Questions

1. What is the biggest distinction between a robo-advisor and a traditional financial advisor?

A robo-adviser is a series of algorithmic-based choices to create a custom portfolio at a reduced cost, with minimal human contact.

A traditional adviser is a human adviser who is capable of providing holistic, bespoke advice across multiple aspects of your finances.

2. Will technology make financial advisers obsolete?

Not entirely. Technology can automate many aspects of the process, but it can’t mirror the human touch of empathy, nuanced problem-solving and emotional support, particularly in many high-stress financial situations.

It seems to me that the future is probably some sort of hybrid model in which tech enables the advisory role rather than eliminating it.”

3. Will a digital wealth management platform keep my money safe?

Legitimate digital wealth management platforms invest heavily in bank-grade security features such as sophisticated encryption and multi-factor authentication to secure your data.

Typically, your investments are also insured by organisations like the SIPC (Securities Investor Protection Corporation).

4. In what ways does technology help make wealth management more accessible?

Technology significantly diminishes the operational costs of a company by automating the manual work. Then it passes the savings on to customers in the form of reduced fees and account minimums, allowing all to have access to financial advice.

Do you want something more than just growing your wealth but managing it for many years to come? By “effective wealth management”, I don’t mean to refer just to the idea of saving money and investing it.

In this article, we will discuss “8 Must-Know Strategies for Effective Wealth Management” to equip you with the practical know-how you need to accumulate, preserve and intelligently accumulate your wealth for a future that is financially secure and prosperous.

If you will employ these strategies, then you can have the power to direct your financial planning, and soon, you can maximize the chances of reaching your long-term financial objectives. Read below to get in-depth knowledge about those crucial tactics for successful wealth management.

Section 1: The Foundation of Effective Wealth Management

Why Strategy Trumps Chance in Wealth Building

We don’t merely accumulate wealth; we manage it, optimize it and protect it. Taking control of your financial future with wealth management Retirees and long-term investors who focus on portfolio income can generally be classified as either savers or reactive savers.

With proactively planned wealth management, the goal is for your money to work on your behalf – not against you.

Section 2: 8 Must-Know Strategies for Effective Wealth Management

Detail: If your goal is wishy-washy, your results will be wishy-washy. Disaggregate desires into measurable goals.

Actionable Advice:

Differentiate between short-term (e.g., down payment), mid-term (e.g., child’s education) and long-term goals (e.g., retirement, legacy).

Attach a figure and schedule to each goal.

For example: “Save X by year Y for retirement” and “Fund the child’s education with Z by age A”.

Strategy 2: Develop a Comprehensive Financial Plan

Detail: This is more than just a budget; this is your custom roadmap to financial success!

Actionable Advice:

Combine budgeting, saving, investing, debt, retirement, insurance and estate planning.

Be sure their parts are all working together toward the purposes you’ve set.

And add a little that a professional wealth manager can assist in establishing this plan.

Strategy 3: Prioritize Smart Debt Management

Detail: I’m not going to get down on debt, because not all debt is bad, and in fact, how one uses debt strategically is essential for wealth-building.

Actionable Advice:

Pay off credit cards, personal loans and other high-interest consumer debt first.

Use good debt (mortgage, education loans) strategically to create an asset or a future cash flow.

Know your debt-to-income ratio to stay in a healthy financial groove.

Strategy 4: Optimize Your Investment Portfolio Through Diversification

Detail: Diversification is important to reduce the risk and to seek out opportunities for growth in different markets. Understand the principles of investment diversification with Investopedia’s guide to diversification.

Actionable Advice:

Diversify investments across a mix of asset classes (stocks, bonds, real estate, alternatives).

Diversify within classes of assets (different industries, different geographies, different scales of business).

Rebalance your portfolio on a routine basis to be sure that it is properly weighted according to your preferences.

Strategy 5: Master Tax-Efficient Investing and Planning

Details: Taxes can eat into your returns big time. Tax planning is key.

Actionable Advice:

Employ tax-advantaged accounts (e.g., 401(k)s, IRAs, ISAs, and pension funds) in accordance with local legislation.

Know capital gains tax consequences and tactics to manage them.

Take advantage of tax-loss harvesting where it makes sense.

Try to guide users to seek jurisdiction-specific advice from a tax professional.

Detail: Protect your wealth from sudden events and ensure a hassle-free transfer.

Actionable Advice:

Purchase proper insurance coverage, such as life, health, disability, property, and liability plans, to guard against significant financial downturns.

Create an estate plan (wills, trusts, powers of attorney) to dictate asset distribution and minimize inheritance taxes.

Strategy 7: Practice Consistent Observation and Flexibility

Detail: Financial plans are not static. Life happens, market conditions change, and strategy must be adapted.

Actionable Advice:

Meet with your wealth manager or on your own at regular intervals (e.g., annually) throughout the year.

Adapt your plan to major life changes (marriage, children, change in work, inheritance).

Keep abreast of economic factors and new laws that could affect your approach.

Strategy 8: Seek Professional Wealth Management Guidance

Detail: While these approaches are foundational, a dedicated professional may be able to offer you some helpful, individualised attention.

Actionable Advice:

Think about hiring a fiduciary wealth manager or financial adviser.

They can be useful for doing complicated financial modelling, advanced tax strategies or even working through some complex market conditions.

Select an advisor by qualification, fee and client ratings.

Section 3: Common Pitfalls in Wealth Management

Mistakes to Avoid on Your Wealth Journey

Emotion-driven investing (rushed buying, following fads).

You have all your eggs in one basket.

Pretending inflation or taxes do not exist in your planning.

Putting off planning (including retirement and estate).

Not reevaluating and updating plans frequently enough.

Lacking an emergency fund for when unexpected expenses arise.

Conclusion

The eight must-know strategies for effective wealth management are, in summary, setting clear objectives, creating a strategic plan, managing debt wisely, diversifying your investments, maximising tax efficiency, managing risk, adapting easily, and, lastly, seeking professional advice.

The way these strategies are structured provides solid support for both building wealth and managing it wisely in order to achieve your greatest financial goals.

Call to Action

Start implementing these practices now and think of ways a financial planner could help you to reach your wealth goals.

Frequently Asked Questions

1. What’s the difference between saving and effective wealth management?

Saving is just putting some money aside. The successful management of wealth is a long-term strategy that encompasses saving, investing, reducing taxes, managing risk, estate planning, and more and should be designed to accomplish certain real-life goals over time. It’s proactive and strategic, not merely accumulation.

2. Is wealth management just for the super-rich?

Historically, wealth management was designed for people with high net worth. With the advent of fintech and as financial advisory services become more accessible, winning wealth management approaches are now relevant and beneficial to a wider audience of more commitment-orientated individuals who want to grow and protect their financial future.

3. What is the return on investment for money management that works?

There is a “risk-return tradeoff”, meaning there is no sure reward and that the return on your investment depends on several factors: your investment strategy, risk tolerance, market conditions and investment time horizon.

Yet, the goal of proper wealth management is to maximize returns while minimizing risk — and that approach could outperform unmanaged assets over the long haul.

4. How frequently should I re-evaluate my wealth management plan?

You should give a thorough, formal review of your comprehensive wealth management plan at least annually.

Further, a major life event (marriage, new job, inheritance, or health change) should be a time for an immediate review and possible shift in strategy.

5. What’s The Most Important Long-term Wealth-growth Strategy?

They are all essential, but setting fiscally tangible financial goals (Strategy 1) paired with diversifying your investment portfolio (Strategy 4) and routinely monitoring and being adaptable (Strategy 7) could be said to be the most consequential for achieving and maintaining long-term wealth growth over time.

Are you interested in increasing, preserving, and transferring your wealth but confused by all the distractions in the financial industry? Getting to know “how does wealth management work” will be your first step to complete financial wellness.

This guide will explain exactly what wealth management is, its fundamental principles, what it comprises, and how hiring a qualified wealth manager can help you plan your financial future.

Understanding the basics of wealth management can enable you to take charge of your financial future and help ensure the choices you make are in line with where you want to go. Let’s take a look at how wealth management can set the stage for your financial success.

Section 1: What Is Wealth Management and Why Is It Important?

All aspects of your financial life

Definition: Wealth management is a professional service which combines financial and investment advice, accounting and tax services, retirement planning and legal or estate planning for one set fee. The programme is for high-net-worth individuals, high-net-worth families, and corporates.

Differing from Financial Planning/Investment Management: Yes, financial planning and investment management are both parts of wealth management, but the latter is more comprehensive in nature, spanning the entirety of a person’s financial life.

Fundamental Objective: The key objective of wealth management is to help you maximise, protect, and pass on your wealth to your loved ones.

For a foundational understanding of wealth management, its components, and how it differs from other financial services, Investopedia offers a comprehensive definition. Check out Investopedia’s explanation of wealth management.

Section 2: Key Steps to How Does Wealth Management Work?

Stage 1: Discovery and Goal Setting

The Client Profile: Knowing more about your financial life and financial situation, the resources and spending.

Life Goals: Defining your short-term, medium-term, and long-term goals, like retirement savings, saving for your child’s education, legacy planning, property purchase, or sale of your business.

Risk Tolerance: Determine your risk comfort level as an investor.

Timeline: Determining realistic time-frames for different goals.

Stage 2: Full-Scale Financial Planning

Budgeting and Cash Flow Analysis: Make the most of income, monitor and control expenses and guard your financial operations.

Investment Planning: Personalising plans for goals and risk tolerance.

Retirement Planning: Figuring out how much you’ll need and the best way to save and spend!

Tax Planning: Developing plans to help reduce taxes on income, investments, and estate.

Estate Planning: Arranging your assets in such a way that they can be passed on to family members as quickly and easily as possible and that as little as possible will need to be paid for inheritance tax.

Risk Management and Insurance: Analysing risks (health, property, life) and advising consumers on obtaining insurance.

Debt Management: Planning on getting yourself into debt or out of it.

Stage 3: Investment Process and Portfolio Management

Asset Allocation: Spreading investments among different types of asset classes (stocks, bonds, real estate, alternatives) in accordance with your financial plan.

Portfolio Building: Choosing from among hospitality properties, mutual funds, ETFs, equities, debt or other investment vehicles.

Active vs. Passive Management: A brief overview of the different philosophies of investing.

Rebalancing: In conjunction with diversification, rebalancing involves the periodic change of your portfolio to reach the appropriate asset allocation.

Performance Monitoring: Measuring portfolio growth against benchmarks and objectives.

Stage 4: Ongoing Monitoring and Relationship Management

Ongoing Reviews: Regular meetings to review progress, to discuss changes in the market and to adjust the financial plan as necessary.

Adjusting to Changing Life Needs: Adjusting financial plans to levels of flexibility with life events such as marriage, divorce, new children, changes in career and health, or inheritance.

Tax Efficiency: Actively working to reduce taxes.

Communication: Keeping the client and wealth manager in regular contact to keep everyone on the same page.

Section 3: Who Provides Wealth Management Services?

Types of Wealth Management Professionals and Firms

Offshore/Private Banks: These are usually designed for the ultra-high-net-worth and provide personalised services to fit their needs.

Independent Wealth Management Companies: Fiduciary advisors (they are usually fee-only) serving customised and comprehensive financial planning.

Brokers/Dealers: Provide wealth management services to clients on a commission-based platform within a broader range of services.

Robo-Advisors (Hybrid Models): Investment management algorithmically – then algorithmically with human oversight lead, frequently targeting the emerging affluent.

What to Focus On: It’s all about how they get paid, Fiduciary duty, fee structure (fee-only, fee-based, commission-based), credentials (CFP, CFA), specialisation, and client focus.

Section 4: What Are the Benefits of Professional Wealth Management?

Why Engage a Wealth Manager?

Professional Advice: Expert advice in sophisticated markets.

Save Time: Save time on managing complex financial details.

Objective Advice: Aids in avoiding financial decisions made on emotions, often with poor results.

Tax Efficiency: Minimising Taxes and Maximising Returns.

Trust or Estate Planning: Securing your legacy for posterity.

Risk Protection: In-depth risk assessment and management protects your investment.

Ease of Mind: The knowledge that you have a well-designed plan for your financial future.

Conclusion

In conclusion of the concepts relating to so-called “how wealth management works”, the process encompasses many parts, ranging from the setting of objectives or goals to the strategic planning of the comprehensive aspects of managing the funds to managing the investments actively and ongoing review of the wealth management plan.

How Wealth Management Works Wealth management is an ongoing, dynamic partnership designed to provide direction and consistency while pursuing your financial aspirations.

Call to Action

Evaluate your financial needs today and find out how professional wealth management can help shape your financial growth and secure your financial future.

Frequently Asked Questions

1. What is the minimum of the asset which you need to utilise the wealth management service?

While most private banks require high assets (like $1 million+ or ₹5-10 crore+), there are a growing number of independent investment firms and hybrid robo-advisors that will serve the emerging affluent (lower minimums, often $100,000 or ₹10-25 lakh in investable assets).

2. What is a wealth manager, and how is it different from an advisor?

A financial planner is more general and focuses on things like retirement planning or investments. A wealth manager, by contrast, provides a far more holistic, all-encompassing service that takes into consideration every element of a client’s financial life beyond investing alone – things like tax planning, estate planning, risk management, and all sorts of ancillary services for those with more complex needs and higher asset bases.

3. How do wealth managers typically get paid?

The most typical fees include a percentage of AUM, an hourly rate, a flat retainer fee, and commissions.

A lot of wealth managers are also fiduciaries and not transactional, i.e., they use a fee-only or fee-based charging model, which is in the client’s best interest.

4. Do wealth managers do my taxes?

Although wealth managers offer in-depth tax planning advice that can help lower the amount of taxes you owe on investments and income, they usually don’t prepare or file your tax returns for you.

They usually will work with your personal accountant or refer you to tax preparers to actually file.

5. How frequently should I have contact with my wealth manager?

Regularity of meetings will vary based on your needs and the firm’s method; however, usually clients meet with their wealth manager at least once each quarter or six months for reviews.

Greater contact can take place with material market shifts, life events, or when particular financial concerns arise.