India remains the world’s fastest-growing large economy, as strong GDP growth accompanies a marked reduction in the rate of inflation. That is a good combination which is giving greater policy flexibility to the Reserve Bank of India (RBI) to sacrifice higher interest rates for some growth-inducing steps with an optimistic India’s Resilient Economic Growth and Easing Inflation: Aiding RBI Policy Flexibility in July 2025

Consistent GDP Growth

The Indian economy remains robust as its real GDP is envisaged to have risen by 6.5 per cent in FY 2024-25, the fastest among the leading global economies. This growth momentum is expected to carry on till FY 2025-26, the Reserve Bank of India (RBI) said.

Other global and domestic institutions, such as the United Nations (6.3% in 2025) and the Confederation of Indian Industry (CII) (6.4% to 6.7% for FY26), reflect this optimistic note. This ongoing performance underscores India’s structural economic strength, which is needed for overall economic stability in an environment of global vagaries.

Inflation Hits Lowest Levels in Years

One important part of this supportive setting is that there has been a great fall in inflation. The year-on-year CPI for May 2025 declined to an impressive 2.82% – the lowest since February 2019. What is more, the Consumer Food Price Index (CFPI) has trended upwards by 0.99% in May 2025; the food inflation has been the lowest since October 2021.

This sharp food price cooling flow, which translates as bumper farm harvests to efficient supply chains, brings dramatic relief to consumers and small businesses and signals a healthy economy. You can find detailed reports on India’s CPI data in The Economic Times.

The RBI’s Increased Flexibility in Policy

India’s continued declining inflation view India’s continuing falling inflation outlook gives the RBI more room to tweak its policy. Now, inflation is expected to stay comfortably within its medium-term target of 4%, possibly even falling below that in months to come.

This will enable RBI to concentrate on the next rounds of growth enablers, such as rate cuts and liquidity measures. The present scenario of low inflation makes it a point to reaffirm the view that the RBI enjoys ample policy flexibility to effectively respond to the changing macroeconomic dynamics.

Strong External Sector and Reserves

India’s foreign sector still enjoys good health, further enhancing the country’s general economic stability. Foreign exchange reserves rose to a robust USD 702.78 billion in the week to June 27, 2025, moving closer to their all-time high.

This comfortable reserve support provides a strong line of defence against shocks and would cover more than 11 months of goods imports. The trade dynamics with the US and its impact on the trade balance are being watched, but the intrinsic export strength (total exports posted an all-time high of USD 824.9 billion in FY2024-25) and steady remittances are continuing to be the foundation for India’s external account.

Cumulatively, these are factors which illustrate India’s sturdy economic standing in July 2025.

The Indian Market Caution on July 7, 2025: US Tariff Countdown and SEBI Probe Weigh on Investor Sentiment. Accordingly, when the Nifty and Sensex opened on a flat note, it appeared that investors were nervous over two things in particular – a looming US deadline on tariffs on Indian goods and SEBI’s impact on a market review over suspected market manipulation. This cautious climate requires that wealth accumulation strategies are applied with a strategic approach.

Nifty and Sensex Remain Muted

The 50 shares of Nifty were flat in early trade on July 7, 2025 (09:40AM) near the 25,485 level in the opening trade on Monday. The BSE Sensex also was trading nearly flat around 83,400. This flatness, according to financial planners, reflects a market that is cautious, in a hurry-up-and-wait posture for clearer signals on outside and inside pressures. The Nifty trend for July 7, 2025, remains neutral as key uncertainties remain in play, affecting the stock market in India today.

US-India Trade Tensions Cast a Shadow

Investment sentiment appears to be reacting to a number of factors, not least of which are the rising trade tensions between the US and India. US President Donald Trump said on Sunday, July 6, that the new trade deals are “coming along very well,” announcing further possible USD products that may face tariffs if the US issues its USD 300 bn worth of Chinese goods levies on July 9.

Such tariffs, between 10% and 50%, and expected to be implemented from August 1, are a big threat to Indian exports. India has not so far been exempted explicitly in any final agreement, which would have made such specific trade measures redundant. This constant ambiguity is one of the reasons that the broader market is being so cautious right now, several market watchers have pointed out.

SEBI Probe Adds to Domestic Concerns

At the domestic level, the financial market is also reeling under the aftereffects of SEBI’s report accusing US trading firm Jane Street of manipulative trading in Indian equity markets. Although SEBI has simply blocked Jane Street from trading in Indian markets and ordered the disgorgement of illegal gains, the broader implications of the investigation on both regulatory enforcement and market reputability have grabbed attention.

This may temporarily affect the trading volume of derivatives and the stock prices of a few exchanges and brokerages. But, according to experts such as VK Vijayakumar of Geojit Financial Services, such short-term regulatory challenges are unlikely to disrupt the long-term positive trend for the broader market.

Early Market Performers and Losers

While thin on the whole, a handful of specific issues saw significant action early. FMCG major Hindustan Unilever, too, was trading with gains of around 1.86% at ₹2,382.80. Asian Paints, too, rose 1.27 per cent to ₹2,455.00. On the other hand, the loss leaders led by Bharat Electronics lost 2.07 per cent at ₹418.70, probably due to profit booking and/or sectoral negative information flows.

The divergent moves indicate that stock-specific action will continue to pan out even as the market grapples with a volatile environment driven by domestic macro and global cues. For real-time stock updates, you can check Angel One’s live blog for specific companies like Bharat Electronics.

Financial independence is a journey, not a race. But for those in the early years of How to Supercharge Your Savings in Your 40s and 50s, the decades are a pivotal period – a combination of a final sprint and a graceful victory lap where time remains to build substantial retirement savings and achieve some ambitious goals.

Odds are that you are in your peak earning years, that you have a wealth of experience and perhaps fewer short-term financial obligations than you did when you were younger.

If you’re not sure how to navigate this key saving period, you’ve landed on the right page. This guide will give you practical strategies to increase your savings and enable you to build a strong fortune as you confidently approach your golden years. For an overall perspective on financial planning in your 40s and 50s, see Investopedia’s guide to saving in your 60s.

Why Your 40s and 50s Are Prime Time for Saving

Though sooner is always smarter, there are some special advantages of midlife for improving your financial planning:

1. Peak Earning Potential

For many, their peak earning years are in their 40s and 50s. This leaves you with more money that you can put towards savings.

2. Closer to Retirement

The retirement end-of-the-rainbow is just around the corner, so, there’s no better motivation than that sense of urgency to get your financial plan fixed up.

3. Reduced Early-Life Expenses

For many, some of their largest expenses — like child care or first-home down payments — may be in the rear view mirror, freeing up cash flow.

4. Financial Wisdom

What do you learn after suing and being sued by everyone from your most trusted adviser to your landlord? You pick up a few things that you would have liked to have known 10 to 20 years ago.

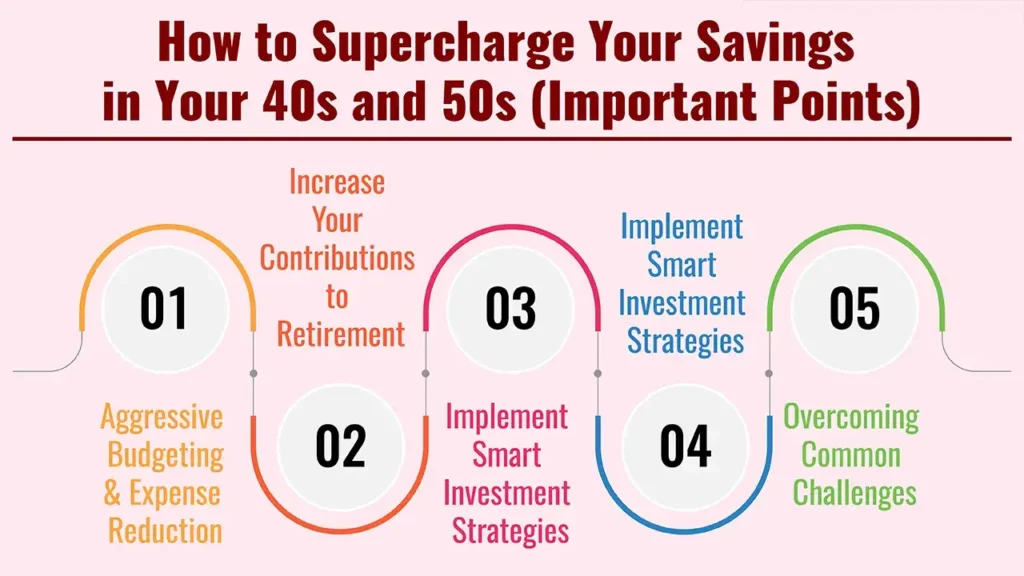

How to Supercharge Your Savings in Your 40s and 50s (Important Points)

It’s time to get strategic. What follows are the best strategies for crushing your savings goals in your 40s and 50s:

1. Aggressive Budgeting & Expense Reduction

Even if you’ve budgeted in the past, a deep dive is in order.

Conduct a Spending Audit: Carefully track all your spending for a month or two. You may be surprised how your money is spent.

Identify and Eliminate Non-Essentials: Consider any recurring subscriptions or unused memberships or any discretionary expenses that you can reduce or cut completely. Small, consistent savings snowball into something significant over time.

Optimize Recurring Bills: Research for lower rates of insurance (home, auto, life), internet, phone plans and utilities.

Reduce High-Interest Debt: Focus on paying back credit card debt, personal loans, or other high-interest debts first. The amount of money saved on interest can then be diverted into savings.

2. Increase Your Contributions to Retirement

It’s debatable, but one of the most important things you can do here.

Max Out Employer-Sponsored Plans: If your employer has a 401(k), 403(b) or other such plan, contribute up to the maximum at which an employer match is available. This is essentially free money.

Utilize Catch-Up Contributions: Someone who is aged 50 or older can usually take advantage of tax laws that also permit higher extra contributions to retirement accounts (such as 401(k) and IRA). Use them to speed up your savings.

Use of a Traditional/Roth IRA or Roth/Traditional Account(s) (ROTH AND/OR IRA): If you’re maxing out your employer plan or don’t have an employer plan, you should be contributing to an I.R.A. or Roth I.R.A., depending on where you’ll be eligible for tax incentives.

Understand and Optimize Pension Plans: If you have a defined benefit pension, know what its payout options are and how it fits with your other savings.

3. Implement Smart Investment Strategies

Your investments should be earning their keep.

Review and Adjust Asset Allocation: As you get near retirement, your ability to prioritize one goal over another changes. And make sure the assets in your portfolio (the mix of stocks, bonds, and so on) are appropriate for your timeline and tolerance. And while you can mitigate risk, just keep in mind that you still have to have growth to fight inflation.

Increase Investment Contributions: Money from raises, bonuses or spending cuts should go directly to your investment accounts.

Diversify Your Portfolio: Diversify money across asset classes, sectors and geographies to reduce risk.

Consider Professional Financial Advice: A certified financial planner can help you develop a personalized investment strategy, maximize your portfolio and handle difficult financial decisions.

Boost Your Income: More money means more to save.

Explore Side Hustles: Put your experience and skills to use on freelancing, consulting or a part-time project.

Negotiate Salary and Promotions: Advocate for yourself at work. Being in your 40s and 50s is valuable.

Monetize Hobbies or Skills: Turn a passion into a source of income.

Consider Rental Income: If you have some extra space, you might be able to rent out a room or property.

4. Optimize Major Expenses

Some of the largest expenses you face may have the potential for great savings.

Mortgage Strategy: Think about putting more money down on your mortgage to own your home that much faster and free up substantial cash flow in retirement. Refinancing at a lower interest rate may also save you money.

Children’s Education Planning: “If you can, try out for selective universities and win scholarships and grants, or look around for a less expensive school, such as a community college. Balance their interests against your own retirement security.

Downsize Your Home: If you find your current residence is larger than you need and there are substantial maintenance costs involved, think about selling and downsizing. And the equity freed up can make quite a difference in your retirement savings.

Healthcare Planning: Outside of insurance, look at Health Savings Accounts (if you can get one), which offer a triple tax whammy (deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses).

5. Overcoming Common Challenges

Hurdles are bound to happen, but you can work through them.

The “Too Late” Mindset: You can never be too deep into improving your financial future. A string of aggressive saving, even just a few years’ worth, can have a significant effect thanks to compounding.

Competing Financial Priorities: Manageing retirement savings alongside other goals (like your kids’ education or caring for ageing parents) takes thoughtful planning and prioritizing. Ensure a balanced message by consulting with the selling agent.

Market Volatility: Avoid letting short-term swings in the market knock you off your long-term course. Stay the course with your diversified investment approach and do not make any emotional decisions.

Conclusion

Your 40s and 50s provide a significant window to reset your financial future. Two other solid vote-getters were small potatoes – paying yourself a portion of everything you earn and squeezing every bit of cost out of a recurring expense.

Get a handle on things, be consistent and get peace of mind from ensuring your retirement is established on a strong foundation – one that will lead to financial freedom and fulfilment.

Frequently Asked Questions

1. What are retirement “catch-up contributions” accounts?

Catch-up contributions refer to extra amounts that people 50 and older can contribute to retirement accounts (such as 401(k)s, 403(b)s and IRAs) beyond the regular annual limits. This is intended to enable older workers to save more for retirement.

2. How much should I be saving each month in my 40s and 50s?

It depends on your income, expenses and retirement goals. Yet a lot of money gurus would advise you to save 15% to 20% or more.

Even if you began saving late or are aiming to retire early during these years. Run a retirement calculator to get a personalized target.

3. Debt repayment versus savings in your 40s and 50s

It really does depend on the nature of the debt. You should probably tackle high-interest debt (such as credit card debt) first, as it is the most corrosive to your financial situation.

Low-interest debt (say, a mortgage) generally comes with advice to take a balanced approach, for instance, paying it down while continuing to save for retirement.

Retirement is one common dream – to put away the daily grind and welcome in a new, free chapter of life. But for most people, the real question is, “How Much Do I Need to Save to Retire?” There is no specific number you should enter; only you can provide the right answer to that deeply personal calculation, based on the kind of lifestyle you hope to lead in the future, your current age, anticipated lifespan and the ever-looming factor of inflation.

This article will help you piece together the retirement so that you can not only gauge how much money you’ll need to build for your golden years but also construct a powerful financial planning for a secure future – no matter where you live.

Knowing How Much Do I Need to Save to Retire?: It’s More Than Just a Number

Only once you’ve seen yourself in your post-retirement life can you determine how much you need.

1. Define Your Retirement Lifestyle

Current Expenses vs. Future Spendings: To compare your current monthly and annual expenditures to how you will retire, begin by recording both sources of data in a list. Now consider how these could change in retirement. Will you travel more? Pursue new hobbies? Or perhaps downsize your home?

Necessity Spending vs. Want Spending: The overall idea is to prioritize your spending between the necessities (housing, food, healthcare, utilities)and the wants (travel, entertaining, luxury products). While some costs may go down (such as commuting), they would also likely rise in some cases—such as healthcare.

Medical Costs: A key, underappreciated issue. Medical expenses the world over are soaring; in such an environment, a sound health corpus or a good cover becomes indispensable. Experts are advising people to set aside a hefty chunk of your retirement treasure chest to be used in medical expenses specifically. For insights into the importance of health insurance in retirement, Acko offers valuable information.

2. Consider Inflation: The Silent Wealth Erosion

Rising prices are a major problem when it comes to planning for the long-term financial stress. What might feel like a comfortable amount today isn’t likely to feel as comfortable 20-30 years from now. Inflation is different in different countries and economic conditions, but it’s something to factor in.

The Impact: Your current spending floor may not be sustainable in 25 years, when your expenses could more than double to over $120,000 a year at a 3% annual inflation rate.

Mitigation: You’ll need to ensure that retirees’ investments grow enough to outpace inflation and protect your buying power.

3. Figure Out When You’ll Retire and How Long You’ll Live

When Do You Plan to Retire? The younger you retire, the more years you will have to cover your expenses during retirement, and hence, would need a higher corpus. Some are targeting early retirement in their 40s or 50s, while others hope to work until their late 60s or even longer.

How Long Will You Live? Life expectancy is increasing all around the world as health care and living conditions get better. It is wise to assume a retirement of at least 25-30 years, if not longer, to avoid outliving your assets.

How to compute your retirement corpus? Practical methods.

And as good as online retirement calculators are, knowing how to calculate retirement yourself is important.

Exponentials, the “25x Rule” (and its Variations)

A common rule of thumb is to aim to have saved 25 times your projected first year’s retirement expenses. For instance, if you want to spend $60,000 a year in retirement (in current dollars), then you would need $1.5 million.

This rule presupposes a somewhat stable withdrawal rate (generally estimated to be around 4%, although it can fluctuate depending on market conditions and personal risk tolerance).

A More Comprehensive Approach:

Here is a step-by-step approach which also addresses the financial realties:

1. Calculate Your Retirement’s First-Year Spending Needs (Inflation Adjusted):

Take your current annual expenses. Then forecast that number forward to your retirement year, with an inflation rate plugged in (3%, say). Example: Annual expense at present = 50,000 * (1 + 0.03) ^ 25 ≈ $104,680.

2. Determine Your Total Retirement Corpus:

And here is where a retirement calculator can be an enormously useful tool. It will consider your annual expenses in the future, how long you expect to live in retirement and what rate of return you expect on your investments during retirement.

Formula (simplified):

Corpus Required = (Future Annual Expenses / (Expected Return Rate in Retirement – Inflation Rate)) * [Factor of life span]

Many of the financial institutions from around the world that we have compared have an online calculator that will assist you with this hard-to-calculate figure, which will consider elements such as:

Current age

Retirement age

Life expectancy

Current monthly expenses

Expected inflation rate

Expected pre-retirement investment return

Expected post-retirement investment return

Current retirement savings

Any anticipated pension income (social security, company pensions, etc.)

Ballpark Figures (Highly Variable):

Although it’s very much a personal choice, rule-of-thumb figures for a comfortable retirement tend to range from $1 million to $5 million (or more). A $40,000–$60,000 lifestyle could suffice for a simple, comfortable existence. This comes from a corpus of $1 million – $1.5 million over 25-30 years. For a large city or a more extravagant lifestyle, this amount could be doubled or tripled.

How to build your Retirement Corpus

With the target corpus in mind, it is on to setting up a strong savings and investment plan next.

1. Start Early, Save Consistently

It’s compounding that is your best friend. The sooner you start, the less you have to save each month to hit your target. And even relatively modest routine investments can grow to a significant sum over decades.

2. Automate Your Savings

Automate contributions to your retirement-themed investment accounts. What people don’t see, they don’t think about, and that can be a great motivator to save more.

3. Diversify Your Investments

Avoid putting all of your eggs in one basket. A balanced portfolio typically includes:

Equities: For long-term growth and returns that beat inflation (for example, diversified stock funds, index funds, ETFs).

Fixed Income: Stick to these easier for stability and less for risk, especially the closer you get to expecting retirement (bonds, government securities, certificates of deposit).

Real Estate: Has the potential for rental income or capital appreciation.

Other investment options: (e.g., commodities such as gold) can be a way to hedge against inflation and economic instability.

4. Leverage Tax-Advantaged Accounts

Research tax-advantaged retirement plans in your country (the United States), such as employer-sponsored plans (401(k), 403(b), 457, and pensions) or individual retirement accounts (IRAs, Roth IRAs, and RRSPs in Canada).

5. Prioritize and Review

Retirement planning is not a one-shot deal. Revisit your plan on a regular basis (at least once a year) and make necessary updates due to changes in income, expenses, inflation or the performance of the market.

6. Consider Professional Advice

With local CFPs, you get that personal touch to set up your tailor-made retirement plan and wade through the murky world of investments while getting clarity on tax rules in your area.

Conclusion

Retirement planning can sound intimidating, but with a few easy steps and a head start – don’t delay – you could have a bright and secure future. Because remember, it’s not just about having as much as you can in your account.

It’s about being able to finally live the dream retirement you’ve always imagined. Take action today, decide what you want out of life, and allow the magic of regular saving and smart investing to move you closer to your goals.

Frequently Asked Questions

1. What is a reasonable corpus to have at retirement?

It’s complicated and depends in large part on your lifestyle and where you live, but in simple terms, a realistic average “corpus” you’ll need for a comfortable retirement might be anywhere from $1M to $5M+ in terms of income associated with inflation and a long retirement.

2. Is the 4% rule a good rule of thumb for retirement withdrawals?

There’s that ol’ 4% rule (taking half your portfolio in the year you retire and then adjusting for inflation) that may apply somewhat differently.

Its efficiency may be affected by factors such as how the market is performing, the level of inflation, and individual risk appetites.

Some financial planners recommend a more conservative or aggressive withdrawal approach.

How much should I save on a monthly basis for retirement?

The monthly savings amount would be a function of your current age, when you would like to retire, expected income need post-retirement and the target corpus. Online retirement calculators can provide an exact number for how much you need to invest each month.

As a rule, the sooner you begin saving, the smaller the percentage of your income you’ll need to save (say 10-15%); the longer you wait, the more you’ll need to save (20-30%, or more).

4. Do I need to pay off all my debt before I can begin investing?

Ideally, yes. It can also keep your post-retirement expenses lower and make you feel even more financially secure going into retirement if you are debt-free, especially with high levels of debt such as a mortgage. That’s one way to keep your retirement money going longer.

5. Just how important is retiree health insurance?

Extremely important. Retirees are also facing significant health costs globally. That’s why its important to have good all-around health insurance and a separate medical fund (outside of your FRS) to protect your retirement savings from health-related expenses not covered by insurance.

As it prepares for a US tariff deadline looming for India on July 9, it is at a crossroads as crucial trade talks with the United States take a crucial turn. The result of these discussions will have significant importance for the stability of the rupee and the overall external finances of the country and are therefore an important focus for risk mitigation in India in the days ahead.

Crucial US Tariff Deadline Approaching

As of July 4, 2025, India and the US are in the throes of an extremely intense dialogue to seal a trade deal before US President Donald Trump’s July 9 tariff deadline.

The inability to reach a sensible deal, or visible progress to that effect, could prove to be a huge strain on the INR and the external balance of the country. This is also one of the single greatest geopolitical risks being watched by the markets.

Most expect a positive result, given the mutual economic and geopolitical interests at stake, but it’s hard to have confidence in that. And that’s a major market risk.

One of the contentious points of negotiations is India’s access to the market for genetically modified (GM) crops. A new option being considered is a “self-certification” mechanism for US exporters who will have to meet India’s GM-free mandate but with a sense of comfort on food safety.

The writings also pertain to India’s food safety protocols under the ‘certification’ and ‘registration’ of certain ‘high-risk’ imports such as dairy, meat, poultry, fish and infant foods.

Improving National Security by Buying Locally

Also, as a boost to the national financial security and to ensure greater self-reliance in the country, the Defence Acquisition Council (DAC), chaired by Raksha Mantri Rajnath Singh, here today accorded approval for capital acquisition proposals valued at over 1.05 lakh crore on 03 Jul 2025.

All these acquisitions are under the ‘Buy (Indian-IDDM)’ category, which prioritises indigenisation of design, development and manufacturing. This policy move is in line with the government’s thrust on defence sector self-reliance.

These cleared purchases would contain vital things like Armoured Recovery Vehicles, Electronic Warfare Systems, and Integrated Common Inventory Management Systems for the tri-services besides surface-to-air missiles.

For the Navy, the acquisitions include moored mines, mine countermeasure vessels, super rapid gun mounts and submersible autonomous vehicles.

These indigenised defence procurement plans, once executed, will improve the mobility, air defence and logistical capabilities of the Armed Forces on the one hand and, on the other, give a significant fillip to the country’s indigenous defence manufacturing environment. You can find the official press release from the Press Information Bureau (PIB) regarding these approvals.

Rupee Performance and External Resilience

The Indian rupee Strong rupee The Indian rupee opened flat against the US dollar on June 30, 2025, at ₹85.48, having registered its best weekly gain since January 2023.

This stability was largely supported by tumbling global crude prices and détente in West Asian geopolitics. India stands to gain, with lower oil prices helping to cut its import bill and support the current account, key to external finances in India.

Active management of currency volatility by the RBI, including buying dollars at key levels, also helps maintain order in the markets and ensures that there are enough reserves for the pots of the financial protection that India has erected for itself against external shocks.

A combination of international trade chop and change, strong domestic defence and central bank initiatives exemplifies the multi-dimensional nature of India’s risk management in times of global and home-brewed challenges.

July 2025: It is an important month for personal finance in India, as it announces an extension date for ITR Filing Deadline Confirmed 2025 and various changes that can affect daily financial transactions.

While taxpayers are paying attention to being compliant, they should also get prepared for increasing ATM charges and new guidelines for Tatkal train bookings by taking proactive steps towards money management.

ITR Filing Extended Date for Salaried Employees

In a sigh of relief for the salaried class, the Income Tax Department has officially announced that the last date for filing ITR 2025 for the financial year 2024-25 (assessment year 2025-26) will be extended from July 31 to September 15, 2025.

This extension, news of which was informed on July 3, would help taxpayers in getting more time for accurate compliance as certain ITR forms (like ITR-2 and ITR-3) are being made more user-friendly, which required more time, for which the last date was being extended.

Taxpayers can now utilise this additional time for filing returns to compile details like borrowings, capital gains and other investment income during the extended period. For an official press release regarding the ITR filing extension, refer to the Press Information Bureau (PIB).

How Increasing ATM & Bank Fees are Affecting Everyone

ATM finders: can be used for other banks as well. Some banks, such as Axis Bank and ICICI Bank, have revised their ATM transaction charges from July 1, 2025. At Axis Bank, the charge on such transactions above the free limit has been hiked from ₹21 to ₹23 a transaction for a gamut of accounts – savings, NRI and so on.

ICICI Bank is also revising service fees on ATM transactions, cash deposits and withdrawals and IMPS money transfers. The rate revision due to higher operating expenses will apply to customers in metro and non-metro markets.

That’s why it’s important for them to review these changes so they don’t get saddled with surprises and so they can tweak their budgeting strategies and transaction habits accordingly to better manage their personal finances.

Tatkal Train Rules Changed: Other things to know

In what is another layer of complication to regular financial and travel planning, new guidelines for Tatkal train ticket booking will be effective from July 15, 2025. Wait no more! For from this very date, all online Tatkal ticket transactions will need to be Aadhaar-based OTP authenticated!

The same is intended to prevent false bookings and improve the security of the booking system. The masses have to link and validate in the coming days for a seamless experience while keeping security in place and adding yet another layer of protection to their daily digital transactions.

Proactive Financial Planning is Key

Apart from these immediate switches, financial planning-related challenges in India are constantly changing. But with the EPFO increasing the auto-settlement limit for advance claims from ₹1 lakh to ₹5 lakh (certain categories of withdrawals in three days for different types of needs) and little better to do with savings at this juncture, the need for caution, in the larger interest of the economy, stands reinforced.

Experts also continue to caution against holding large amounts of cash in low-interest savings accounts that don’t even keep pace with inflation and recommend other high-yield investment options. This personal finance news in India for July 2025 tells us that the need of the hour is that we should all stay informed, agile and proactive in managing our personal finances if we don’t want to be hurt financially when it all unfolds in the years to come!

The magazine highlighted India’s economic resilience, quoting a healthy 6.4-6.7% GDP growth forecast for the Indian economy by the CII Projects Strong GDP Growth Amidst RBI Rate Cut; India’s Economic Resilience in July 2025

This positive India economic outlook for 2025 is supported by robust domestic demand and recent proactive steps taken by the Reserve Bank of India (RBI).

Driving Factors for Economic Growth

Speaking at a press conference on July 3, 2025, CII President Rajiv Memani said despite rising global economic and political turmoil, India continues to shine as one of the “bright spots”. Key reasons for this optimistic sentiment are positive monsoon forecasts (key for farm output) and an increase in liquidity in the financial system. For more details on CII’s economic outlook, you can refer to the Economic Times’ report.

Big Role of RBI monetary policy The RBI has significantly played the role after it reduced the repo rate by 50 basis points to 5.50% at the June 2025 meeting and a 100 basis point reduction in the Cash Reserve Ratio, opening liquidity of over ₹2 lakh crore for the banking system.

These acts are designed to increase the country’s credit growth and encourage economic activity, which is important Indian economy news.

Inflation and Policy Stance

RBI’s decision to lower rates was spurred by a sharp easing of inflation, with the CPI inflation dropping to 3.16 per cent in April 2025, its lowest since July 2019. The policy bias has transitioned from an ‘accommodative’ bias to a ‘neutral’ stance, implying a neutral outlook and a data-dependent approach to future rate moves.

Inflation expectation for FY26 has been slashed to 3.7%, giving confidence in stable and limited inflation. Although headline inflation has moderated, observers will keep a close eye on whether core inflation (which excludes food and fuel) does the same, as the two have historically tended to converge.

Focus on Reforms and Competitiveness

CII has also announced its theme for the year 2025-26, “Accelerating Competitiveness: Globalisation, Inclusivity, Sustainability, Trust”, with suggestions for strategic economic reforms. These are ways to increase manufacturing, exploit technology and AI (including the proposal for a National AI Authority), accelerate sustainable processes and improve livelihoods.

Emphasis is laid on enhancing India’s competitiveness through global engagement and inclusive growth, which is necessary to achieve sustainable economic stability. Loans for MSMEs needed to be scaled up and R&D supported across industries as well, according to CII.

Fiscal Discipline and External Stability

We view the government’s decision to stick to the 4.4% of GDP fiscal deficit target for FY26 (Apr-Mar) and the shift to medium-term debt targeting from FY27 and beyond as positive for fiscal discipline.

Externally, though FDI and FPI could continue to be sluggish on account of global vagaries, the strong quantum of India’s foreign reserves, at around $691.5 billion in June, is comforting and provides sufficient cover against external volatility (it covers over 11 months of imports), thereby ensuring a stable BOP.

Together, these factors further confirm the optimistic market views July 2025 for India’s economic odyssey.

As of July 4, 2025, the Indian stock market, specifically the Nifty, is beginning to indicate a broadening rally and not just predicated on a few outperforming stocks.

Is Market Breadth Improves: Is a Broader Bull Run on the Horizon for Indian Investors in July 2025? India is favouring more stocks that participate in the upside move, indicating that more wealth creation opportunities for stock investors are open in the months ahead.

Nifty’s Present Status and Technical Levels

Nifty outlook July 2025: The index is seen consolidating after it made a nine-month high of 25669. As of July 4, 2025, the Nifty was trading mostly unchanged around 25,407.45, up from an intraday low of 25,370.

Support is at 25,400-25,450 levels, but the bounce back does not have any strong conviction, as The Hindu BusinessLine points out. Immediate resistance is at 25,500-25,600. A strong breach of 25,500 might extend the rally to 25,600 or 25,650, whereas a fall below 25,370 may take the index lower to 25,200. For further technical insights and daily levels, Trade Brains offers a detailed breakdown.

This phase of sideways trading indicates that investors are also waiting for fresh triggers before placing big directional bets.

Where does Nifty stand now, and what are its technical levels?

Nifty July 2025 outlook: The index is likely to remain consolidative, taking resistance around the nine-month high of 25669. As of July 4, 2025, the Nifty has been trading almost flat at 25,407.45 from an intraday low of 25,370.

There is support at the 25,400-25,450 levels. However, the bounce back does not have much conviction, as The Hindu BusinessLine is pointing out. Immediate resistance is at 25,500-25,600. An overwhelming breach of 25,500 can trigger rally towards 25,600 or 25,650, while a drop below 25,370 can take the index lower to 25,200.

This period of sideways trading is a sign that investors are waiting for more new triggers before taking large directional bets on the market.

Where is Nifty now, and what to do with technical levels?

Nifty July 2025 outlook: The index is expected to consolidate, being resisted at a nine-month high of 25669. On July 4, 2025, the Nifty has been hovering in deep red territory at 25,407.45, up barely 3 points from its intraday low of 25,370. There is support between the 25,400 and 25,450 levels.

But the rebound doesn’t seem to have much conviction, as The Hindu BusinessLine is noting. Immediate resistance is at 25,500-25,600. A break below 25,370 can pull the index down to 25,200.

This sign of commitment by left-for-dead stocks has helped most major indexes post gains over the last few sessions as they break out of at least one week of sideways trading, with investors waiting for more fresh catalysts before placing huge directional bets on the market.

FII and DII Dynamics

The market is still strengthened by aggressive buying from Domestic Institutional Investors (DIIs), who have been a bulwark against intermittent selling by Foreign Institutional Investors (FIIs).

On July 3, FIIs became a net seller of ₹1,481 crore in the equity segment, against DII buying of ₹1,333 crore. However, the general sentiment is cautiously optimistic, with analysts saying that any market fall should be used as a buying opportunity for long-term wealth building in the country.

Besides this, the low India VIX (implying least volatility, now standing at 12.38) reaffirms that investors are seemingly comfortable and there is no element of panic.

“The idea of ‘Smart Investment Strategies to Build Long-Term Wealth’ intimidates us in an age of instant gratification and short attention spans. Yet it is the foundation of financial security and of freedom itself. Growing rich doesn’t happen overnight; it requires time and strategic planning.

This piece will reveal “smart investment strategies” that will help you “build long-term wealth”. We’ll talk basics, investment building blocks, and basic habits to develop for a lifetime of financial prosperity. By implementing these techniques, you’ll be able to lay the foundation for a brighter financial future and start building wealth.

1. The Basis for Smart Investment Strategies to Build Long-Term Wealth

Mindset, Goals, and Discipline

1. Start Early (The Power of Compounding):

Detail: The younger you start investing, the longer your money will enjoy time to compound and grow at an exponential rate, in which the money you earned will make you even more money.

Why it’s beneficial: Even modest, regular investments early in life can outperform larger investments later in life.

2. Define Clear Financial Goals:

Detail: What is it you are saving for? Retirement, a child’s education, a home, financial independence? Concrete goals bring focus and inspiration.

Why it’s beneficial: Goals drive how much to invest as well as where to and for how long. Learn how to set financial goals from Ally Bank.

3. Plan and Save: Create a No-Spend Budget and Save Regularly

Detail: Know your ins and outs. Budgeting helps you know where to save and have room in your cash flow to contribute on a regular basis.

Why it’s beneficial: Regular saving is the gasoline in your investment engine. Automate savings to build discipline.

4. Save for Emergencies: Build and Maintain an Emergency Fund:

Detail: Before going all in, establish a liquid fund (3–6 month’s worth of living expenses) in a savings account.

Why it’s beneficial: It can keep you from having to sell long-term investments at a loss in the event of a surprise financial crisis.

2. Principles of Smart Investing

Strategic Approaches for Sustainable Growth

1. Diversification (Don’t Bet the Farm on One Horse):

Detail: Diversify your investments across asset classes (equities, debt, real estate, and gold), sectors and geography.

Why it’s beneficial: Mitigates risk; if one investment does badly, others may do well, so the good and the bad help to balance out your portfolio.

2. Invest for the Long Term (Don’t Try to Time the Market)

Detail: Emphasis on holding quality investments for years, even decades. Avoid the temptation to trade on the basis of short-term market movements or “news.”

Why it’s beneficial: It is notoriously difficult to time the market. Investing for the long run can help you harness the gains of the overall market and is the best way to ride out the market’s inevitable ups and downs.

3. Dollar-Cost Averaging (SIP – Systematic Investment Plans in India)

Detail: Invest a set dollar amount at set intervals (say monthly) irrespective of prices in the market. You buy more units when prices are low and fewer when prices are high.”

Why it’s beneficial: Smooths the average purchase price over time – reducing risk and taking emotion out of the equation. Works wonders for mutual funds in India.

4. Rebalance Your Portfolio Periodically:

Detail: As the performance on each of the investments changes over time, your asset allocation may change as well. That process of selling some of the outperforming assets and buying more of the underperforming assets to return to your target allocation is known as rebalancing.

Why it’s beneficial: It helps you keep your desired risk level and can make you “buy low and sell high”.

5. Focus on Low-Cost Investments

Detail: If high fees (management fees, expense ratios) are plucking too many of your feathers, then your long-term returns can be significantly compromised. Choose from low-cost index funds, ETFs, or direct plans of mutual funds.

Why it’s smart: Even small differences in fees can result in huge disparities in wealth accumulated over decades.

3. Long-Term Growth Investment Workhorses

Where to Stash Your Money, Besides Under Your Bed, for the Next Emergency

Stocks (both individual stocks and equity mutual funds):

Detail: Provide the greatest long-term growth attitude solution. These can be largely individual stocks (blue chip, growth, dividend-paying ones) or even diversified equity mutual funds/ETFs.

Consideration: Greater volatility, but necessary for wealth generation.

Debt Instruments (Bonds & Debt Mutual Funds)

Detail: Offer security and some stable income. Bonds of the government, of corporations and of mutual funds full of debt.

Consideration: Lower returns compared with stocks, but important for portfolio stability and capital preservation.

Real Estate

Detail: Can be cashflow and growth. You could own the property outright, own shares (such as in real estate investment trusts, or REITs), or own fractions.

Consideration: Illiquid, high entry cost to direct ownership, but potentially an inflation hedge.

Gold

Detail: Can act as a hedge against inflation and economic insecurity. Can be invested in physical gold, gold ETFs or sovereign gold bonds.

Consideration: Doesn’t make money, but diversifies and adds safety.

Policies focused on retirement (NPS, PPF, EPF, etc. in India)

Detail: Tax-friendly, long-term, compounding schemes run by the government or under government supervision in your country.

Consideration: Long lock-ins, great for retirement planning.

4. Habits and Pitfalls to Avoid

Developing A Mindset And Steering Clear From Mistakes

Good Habits: Always learning personal finance, revisiting/marking your portfolio consistently, disciplined purchasing, and adding more to your investments with an increase in income.

Avoid these common pitfalls:

Emotional Investing: Allowing decisions to be driven by fear or greed.

Pursuing Hot Tips/Fads: Making speculative investments in unproven assets without doing any of the due diligence.

Not heeding due diligence: not knowing what you are investing into.

Too Much Debt: Interest on debt can cancel out gains from investments.

Over-Leveraging: Over-borrowing to invest, and so increasing losses.

Hyper-Focused on Returns: Not considering risk, fees, or liquidity.

Conclusion

In short, “smart investment strategies to build long-term wealth” are premised on having goals, systematically saving and investing, and disciplined asset allocation in multiple classes. His mantra is to build “long-term wealth”, which he says is a journey that demands patience, persistence, and a desire to learn.

With these fundamental approaches and pitfalls in mind, you will be prepared to successfully navigate the investment world and provide a financially sound future for you and your loved ones!

Call to Action

You should begin today, even if you invest small amounts, and also look at taking the advice of a SEBI-registered financial advisor for customized advice.

Frequently Asked Questions

1. How much do I need to invest to become wealthy over the long run?

There’s no one-size-fits-all answer. Begin with what you can afford to do on an ongoing basis, no matter how modest that amount may be. The trick is to act consistently and as early as possible.

A good rule of thumb is to set aside at the very least 10-20% of income, bumping it up a bit as your income increases.

2. Is the stock market too dangerous when it comes to building long-term wealth?

Markets have been known to make people rich overnight or poor in just minutes; in the short term, it is very volatile, but over a long period of time, historically, equities have given the best returns – they have beaten inflation and other asset classes.

This risk is greatly diminished by diversification, focusing on quality companies/funds and taking a long-term view.

3. How much does inflation matter in long-term wealth building?

It’s inflation and stripping your money of its purchasing power. Intelligent investment strategies seek to produce returns that are higher than inflation so that your money grows in real terms.

Assets such as stocks and real estate tend to be good hedges against inflation.

For many years, “stocks, bonds, and cash” constituted the fundamental trinity of investment portfolios. For wise investors seeking to diversify and possibly increase returns, a new realm of “alternative investments” offers bright futures.

By the end of this article, you’re going to know exactly “what are alternative investments” and a variety of typical “examples of alternative investments”, and you’ll learn why they’re taking the system over by storm and, with that, the key benefits as well as risks that come with them.

With a little education in alternative investments, you can broaden your investment horizon and build a stronger investment portfolio.

1. What Are Alternative Investments? Definition and Examples

How Are Digital Assets Different From Traditional Assets?

“Alternative investments” are financial assets that do not fit into traditional investment categories, such as publicly traded stocks, investment-grade bonds and cash. They are generally less liquid, may be less transparent and may currently be subject to less oversight than other asset types.

Objective: They are regularly requested to:

Diversify Portfolios: Because of their low correlation with traditional asset classes.

Possibly Produce Higher Returns: Typically with Higher Risk.

Hedge Against Inflation: Some kinds, such as real assets.

Access Exclusive Opportunities: Restricted markets or industries.

Key Characteristics:

Illiquid: Not readily purchasable or saleable on public exchanges.

Larger Minimum Investments: Usually limited to ‘accredited investors’ clients or High Net Worth Individuals (HNIs), but access is being opened up.

Less Regulation: A catalyst for less transparency.

Complexity: May require specialized knowledge.

2. A Broad Array of ‘Alternative’ Investments

A Glimpse into the World of Non-Conventional Assets

1. Real Estate (Beyond Public REITs): Owning the real estate directly (apartment building, commercial building, land) for rent or appreciation. This could be through fractional ownership in a commercial property or via a project.

Example: Include investing in a commercial complex, leasing out an apartment, and using a real estate crowdfunding platform for a particular project.

Note: Although REITs are similar, direct or private real estate funds are considered alternatives as a result of their illiquidity and direct management.

2. Private Equity (PE) & Venture Capital (VC): Investing in companies that are not listed on the stock exchange.

Private Equity: Usually invests in seasoned private companies, mostly for buyouts or growth capital.

Venture Capital: Focuses on young, high-growth companies that have a high potential.

Examples: Putting money into a fund that buys private businesses or funding a hot new tech startup in Bengaluru.

3. Hedge Funds: Investment funds that are open to a limited number of accredited investors and that engage in a wider range of investment and trading activities than most funds, which include long/short equity, global macro strategies, and arbitrage, among others. Hedge funds also typically use leverage and may use derivatives.

Examples: An investment in a fund that employs sophisticated trading strategies throughout multiple classes of assets. For more on hedge funds, see Corporate Finance Institute’s explanation.

4. Commodities: Base goods or raw products, as they are found in their natural state, such as gold or cattle.

Examples: gold, silver, crude oil, natural gas, agricultural products (wheat, corn). Physical/Futures/ETF Physical or futures/ETF way to invest.

5. Private Debt/Private Credit: Providing capital directly to private companies, typically those which are unable to borrow from banks or public credit markets. This lending can be structured as direct lending, mezzanine debt, or well as distressed debt.

Examples: Investing in a fund that lends to expanding businesses.

6. Collectibles & Physical Assets: Tangible and finite products that derive value from their rarity, age or beauty.

Examples: fine art, rare wines and classic cars, in addition to rare coins, stamps, antiques and luxury watches.

7. Infrastructure: Spending on big public works or critical services.

Examples: Roads, bridges, airports, power plants, and communications networks, frequently through specialized infrastructure investment funds.

8. Farms: Direct investments in 100%-owned agricultural operations or leased land to farmers or pure speculation.

Examples: Buying up agricultural land for lease or investing in a farmland investment fund.

3. Why Consider Alternative Investments? (The Benefits)

The Advantages of Going Beyond the Norm

Diversification: reduced overall portfolio risk and volatility is possible with low correlation with the traditional stock and bond markets, particularly during market downturns.

The potential for higher returns: A lot of alternatives, especially in the world of private markets, promise the potential for higher risk-adjusted returns relative to traditional assets.

Hedge Against Inflation: Physical assets, such as real estate and commodities, tend to retain or increase their value in an inflationary environment.

Unique Access to Opportunities: invest in new companies or niche markets not offered on public markets.

Lower Market Volatility (Sometimes): Because of the illiquidity, their values do not swing daily like public stocks would, providing a less bumpy ride (though the underlying value can still change).

Professional Management: A good number of alternative funds are run by professionals in those respective markets.

4. The Risks Associated with Alternative Investments

Understanding the Downsides Before Investing

Illiquid: Not easily or quickly sold at a price close to fair value. Funds often have lock-up periods.

Complexity & Opacity: Difficult to understand and less regulated, so less information is publicly available.

High Minimum Investments & Fees: It is usually only available to wealthy investors, and fees can be higher with fund managers charging extra in management and performance fees.

Valuation issues: Not easy to value with precision because they do not trade on any public exchange.

High Risk: Can lose a substantial amount of your investment strategies, particularly with venture capital or speculative investments.

Less Regulation: Provides less oversight than with other publicly traded traditional securities.

Manager dependence: Performance may be highly dependent on the manager’s skill and judgement.

Conclusion

In short, “alternative investments” comprise a variety of asset classes that are not traditional stocks, bonds, or cash, which provide unique “benefits” such as diversification and potential for higher returns, which are offset by real “risks” such as illiquidity and complexity.

Despite the potential to add value to a portfolio, not every investor is right for alt investments. And like anything else, what’s most important is that you understand what they are, who they’re for, the pros of “examples, ” cons, and determine whether or not they fit into your portfolio. Seeking advice from an experienced adviser is a must before delving into such complex channels.

Call to Action

No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor.

Frequently Asked Questions

1. Who are alternative investments generally appropriate for?

Throughout history, alternatives have only been really available to institutions (pension funds, endowments) and high-net-worth individuals (HNIs) since being out of reach for the average retail investor due to high minimums, lack of liquidity, and complexity.

But as crowdfunding or fractional ownership platforms gain popularity, access to even accredited retail investors and, by extension, non-accredited entities in a lot more geographies, India included, is increasing.

2. How can alternative investments assist with portfolio diversification?

Many alternative investments have a low correlation with conventional investments such as stocks and bonds. What this means is that they are driven by different market drivers.

Alternatives may not behave as traditional markets do when they decline, which can lead to decreased overall portfolio volatility and risk.

3. Do alternative investments perform better than traditional investments?

In alternative investments, investors usually have options for higher returns compared to traditional investments, especially in private equity or venture capital.

But this opportunity does not come without its corresponding risk, such as illiquidity and increased volatility in certain forms. Returns are not guaranteed.