Savers nationwide will get more chances to fatten their retirement savings accounts after the Internal Revenue Service announced today that 2026 contribution limits will be higher for some types of retirement plans.

The biggest increase is in the elective deferral limit for 401(k) and similar workplace plans, which rises to $24,500 from $19,500 in 2025. The changes, spurred by cost-of-living adjustments, are meant to assist Americans in more efficiently saving for retirement against continued inflationary headwinds.

The official guidelines reflecting these changes are generally released in late October or early November of the prior year, and estimates from financial experts mostly have come in line with these projections. The IRS has announced the 2026 retirement contribution limits, raising the 401(k) cap to $23,500. Learn how this impacts your retirement savings strategy.

Key Changes for 2026

Here’s a breakdown of the new limits for the 2026 tax year:

401(k), 403(b) and 457 Plans: The employee elective deferral limit for these plans will go up by $1,000 to $24,500. That goes for both pretax and Roth 401(k) contributions.

IRA Contributions: The maximum amount that millennials can contribute to an IRA in 2020 will likely be the same as in 2019 – $7,000 for both Traditional and Roth IRAs.

Catch-Up Contributions (50 or Over):

The contribution limit for catch-up contributions to 401(k), 403(b), and most 457 plans for those age 50 and over will be $8,000, up from $7,500. In other words, those who qualify can contribute up to $32,500 ($24,500 + $8,000).

For people 60, 61, 62 and 63, the “super catch-up” limit in an existing law raised by the SECURE 2.0 Act of 2022 is even higher, at $11,250 for 2026.

The IRA catch-up contribution for people 50 and older will also remain the same at $1,000.

Total Defined Contribution Limit: The most that can be contributed to a defined contribution plan (including employee and employer contributions, but not catch-up contributions) is expected to rise to $72,000 for 2026, up from $70,000 in 2025.

SECURE 2.0 Act’s Impact on Catch-Up Contributions (Effective 2026)

One major change for 2026, a result of the SECURE 2.0 Act, alters the way certain high earners contribute their catch-up amounts:

Mandatory Roth for High Earners: For tax years beginning after 2025, individuals with prior year Social Security (FICA) wages that exceed $150,000 (as indexed for inflation from the $145,000 in 2024), the catch-up contribution shall be made as an after-tax Roth contribution. This means that contributions to the account aren’t tax-deductible in the year they are made, but qualified withdrawals in retirement are tax-free.

Implication for Plans without Roth: When a 401(k) plan doesn’t allow Roth contributions, participants in this high earner group would not be eligible to make any catch-up contributions. This provision, which originally was scheduled to take effect in 2024, was postponed by the IRS to allow employers and payroll service providers additional time to update their systems.

Planning Ahead for Retirement Savers

These higher limits can be an excellent way for people to turbocharge their retirement planning. Financial advisors recommend reassessing existing contribution strategies to make the most of the higher thresholds, especially for those nearing retirement and able to take advantage of catch-up contributions.

Since the law’s effective date approaches, employers should also make sure that their retirement plans are updated to be compliant with SECURE 2.0 requirements, including the new mandatory Roth catch-up contributions for highly compensated employees.

The changes support a continued focus on increasing retirement savings security for America’s workers by promoting broad access and enhancing savings opportunities in an evolving economy.

In a major diplomatic and business move, Jensen Huang, CEO of leading AI chipmaker NVIDIA, praised Chinese-developed AI models as “world class” today, July 16, 2025.

His comments at the opening ceremony of the third China International Supply Chain Expo (CISCE) in Beijing were reported one day after NVIDIA said it had received U.S. government permission to sell its H20 AI chips to China.

Explore how Nvidia’s Huang hails Chinese AI models as “world class”, emphasising their significant contributions to artificial intelligence innovation worldwide.

Praising Chinese Innovation

Huang singled out AI models created by Chinese companies such as DeepSeek, Alibaba and Tencent as “world class”. AI has become “essential infrastructure, like electricity”, he said, and is “transforming every industry, from scientific research and health care to energy and transportation and logistics.”

Meanwhile, the open-source AI landscape in China serves as a “catalyst for worldwide development”, according to the CEO of NVIDIA, who has welcomed the country’s rapid progress in AI development.

This endorsement by one of the world’s most influential technology leaders further solidifies the rapid maturation of China’s AI ecosystem, which has achieved big gains in generative AI, notably in non-reasoning models. Chinese producers also innovate, and models such as DeepSeek V3 0324 have become popular worldwide.

Navigating the US-China Tech Landscape

Huang’s visit to China, his third of this year, comes at a sensitive time for Nvidia, which is trying to steer its way through the knotty and often combative entanglement between the world’s two biggest economies, which are jostling for pre-eminence in AI and other state-of-the-art technologies.

The praise for Chinese AI models, along with the now-resumed sales of the H2O chips, indicates an attempt to salvage relationships and still serve the very important Chinese market investment strategies. The H20 chip, an adaptation of NVIDIA’s high-end AI accelerators, had been built to adhere to previous US export regulations.

In the wake of enhanced legislation, its sales were suspended in April 2025. But on July 15, NVIDIA said it received confirmation from the U.S. government that licences would be provided for the export of H20s into China, with shipments set to resume “shortly”. NVIDIA is building a new, fully compatible model RTX Pro GPU for the Chinese market for purposes of nickel AI applications.

Balancing Interests and Future Outlook

Huang has long maintained that curtailing exports would undermine U.S. leadership in AI by limiting American companies’ ability to sell to developers around the world, including the large number of AI researchers in China.

His recent contacts with US President Donald Trump and other top policymakers purportedly involved talking about not allowing American technology to become the worldwide standard. The freshly restored permission to sell H2O chips – plus Huang’s public praise of Chinese AI – is an example of the relatively carefully negotiated relationship that Nvidia must maintain.

It is designed to take advantage of the huge and fast-moving Chinese market while remaining compliant with US export controls. The political tactic also underscores the interconnected reality of the global AI industry and tech giants’ overtures to political enemies in the name of tech progress. In the months ahead, we will see how this delicate balance influences the state of the market and the overall landscape of AI globally.

Retirement is creeping up on you, and perhaps you feel the ticking of the clock. But the good news is this: your later career years can actually be some of the most impactful when it comes to turbocharging your retirement savings!

This guide is intended for people in their 50s and early 60s who are nearing retirement. This stage is so important because you have a lot working for you, including peak income potential, the ability to maximize your contributions to savings and retirement, and having an idea of what retirement feels like.

Navigate the complexities of late career retirement planning. Learn how to maximize your savings and ensure a comfortable retirement lifestyle.

The Landscape of Late-Career Retirement Planning Tap Qualified or not?

Advantages You Have

Greater Income Potential: Typically this is when you make the most money.

“Catch-Up” Contributions: Designed as a way for older savers to make up for lost time, you can contribute more to retirement accounts.

Less Debt (Maybe): Some people may have paid off — or paid down — their mortgage.

Sharper Vision: You probably have a clearer vision of your retirement dream.

Specific Challenges

Time Horizon: Time for Compounding to Wonder on Miracles.

Risk of Market Volatility: Less time to recover after a large market decline.

Health-Related Expenses: A significant worry that rises as we age.

Caregiving Duties: You might have to help ageing parents or grown children.

Insecure employment: The possibility of unexpected job loss is more threatening as retirement nears.

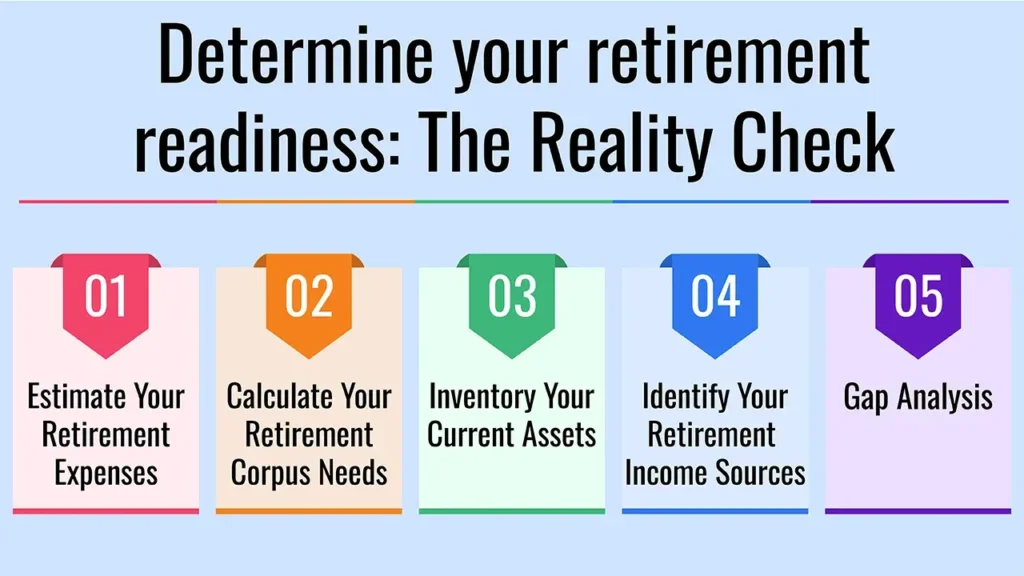

Step 1: Determine your retirement readiness: The Reality Check

Determine Your Retirement Date: When do you want to retire versus when can you afford to retire?

Estimate Your Retirement Expenses: Establish a comprehensive post-retirement budget to cover housing, food, health, travel, hobbies and entertainment. Keep in mind to adjust for inflation and the possibility that other spending niches could increase.

Calculate Your Retirement Corpus Needs: What target do you need to hit to sustain the lifestyle you want? It’s best to use rules of thumb, such as 25-30 times annual expenses, or a comprehensive retirement calculator.

Inventory Your Current Assets: Mention all retirement accounts (EPF, NPS, PPF, mutual funds, stocks, and real estate), savings and other investments.

Identify Your Retirement Income Sources: Include pensions (if any), NPS annuities, rent and systematic withdrawal plans (SWPs) from mutual funds.

Gap Analysis: Compare your estimated future needs with your existing savings and income sources to determine the “gap” you have to make up.

Step 2: Save and Contribute as Much as Possible

Supercharge Retirement Accounts

Catch-Up Contributions: Avail of such enhanced limits for above 50 category (following are the specific provisions concerning NPS, EPF or such other government/employer schemes in India)

Leverage EPF/VPF: To the extent applicable, enhance voluntary provident fund (VPF) for assured return and tax advantage.

NPS (National Pension System): Avail of tax benefits under Section 80CCD(1B) for investments over and above 80C.

PPF (Public Provident Fund): Invest the maximum every year and get tax-free returns.

ELSS (Equity Linked Saving Schemes): For 80C tax benefits along with exposure to equities, you may consider this.

Aggressive Savings

Trim your discretionary spending and figure out how to raise your savings, perhaps by paying yourself first via automatic transfers.

Convert Non-Earning Assets

Some things you should consider: Selling off your “extras” (like a second home or expensive cars) in order to ramp up your retirement savings.

Step 3: Refine Your Investment Plan

Risk Reassessment

Start the transition of your portfolio from high growth to balanced or conservative. And the aim should be to preserve capital and to grow income, not to see aggressive how-much-can-I-do growth.

Asset Allocation

Talk about the need to “rebalance” as you get older and reduce your exposure to stocks and increase exposure to debt/fixed income as retirement edges closer (i.e., you’ve got a 60/40 equity-to-debt ratio when you’re 40, but that should maybe be more like 40/60, eventually 30/70).

Income-Generating Investments

Debt Funds: For stability and moderate returns.

Fixed Deposits (FDs): Safe and sure income, but no tax benefits.

Senior Citizen’s Savings Scheme (SCSS): The SCSS is a government-guaranteed scheme for regular post-retirement income (if you were eligible).

Annuity Plans: Explain about them being the source of providing guaranteed income for life but also their drawbacks (no liquidity, low returns)

Tax-Efficient Withdrawals

Develop a withdrawal strategy for your various accounts (taxable and tax-exempt) to reduce your tax liability in retirement.

Step 4: Strategic Debt Management

Goal: Debt-Free Retirement

Pay off all high-interest debt (credit cards, personal loans) before retirement.

Mortgage Strategy

Strive to have your home loan repaid or a substantial debt reduction by the time you retire. This will leave you with a sizeable amount of cash flow in retirement.

Avoid New Debt

Be very cautious about taking on extra loans or expanding your debt as you near retirement.

Step 5: Critical Insurance and Healthcare Planning

Health Insurance

Make sure you have good health insurance that carries over into retirement. Think about a super top-up or critical illness policy to meet larger medical expenses.

Long-Term Care (LTC) Insurance

Although relatively infrequent in India compared with parts of the West, talk about whether it makes sense to provide for the possible cost of assisted living or nursing care.

Life Insurance Review

Reevaluate whether you still need term life insurance. If your dependants are no longer depending on your income, you may have the option of scaling back or completely dropping coverage in order to cut costs.

Step 6: Retirement’s Non-Financial Impacts on Households

Define Your Retirement Lifestyle

What are you going to do when you retire? Think about hobbies, travel, volunteer work, family or a passion project.

Social Connections

Be sure to make time for socializing in order to improve your quality of life.

Housing Decisions

Consider downsizing, moving to a less expensive part of the country or taking out a reverse mortgage (on which you should be very sceptical and very careful and should consult experts).

Part-Time Work/Encore Career

Could you work part-time in retirement for a little extra income?

Estate Planning

Review any will or power of attorney documents you have, and think about designating beneficiaries for your assets.

Step 7: Importance of Seeking Professional Help

When You Need a Financial Adviser

If you feel frazzled or have complicated financial circumstances, consider hiring a financial adviser to help with a personalized game plan.

What a Financial Planner Can Offer

A financial planner can help with goal identification, cash flow analysis, investment rebalancing, tax planning, estate planning and withdrawal strategies.

Choosing the Right Advisor

Identify SEBI-registered Investment Advisors (RIAs) or Certified Financial Planners (CFPs) who would provide independent advice and work on a fee-only model.

Conclusion

Focused action in these late working years really can make a difference in your retirement security and comfort level. And with the right moves today, you can be on the road to a full and financially secure retirement.

Call to Action

Begin your retirement checkup today! For help putting the finishing touches on your late-career strategy, seek advice from a financial planner — and download our retirement checklist!

Frequently Asked Questions

1. At age 50-something, is it even worth saving for retirement?

It’s never too late! Although you can’t save as long, there are ways to make the most of your retirement savings.

2. What are the best low-risk investments for someone about to retire?

For stability and predictable returns, you can look at vehicles such as fixed deposits, debt funds, government-backed schemes, etc.

3. What are the best health insurance options for retirees

Ideally, you should look at a comprehensive health insurance plan which includes hospitalisation and outpatient cover and also consider Super Top-up plans for additional cover.

That shiny new “real” job just land in your lap? Excited, yes, but also a little overwhelmed by adulting and running your own finances? You’re not alone! Young professionals have a difficult road to hoe when it comes to money.

Early financial education ensures long-term prosperity and helps to avoid common pitfalls. This manual covers important topics including budgeting, investing and debt reduction and will equip you with the knowledge that you need to secure the financial future that you deserve.

Empower your personal financial planning for young professionals. Learn to budget, save, and invest wisely for a prosperous future.

The Financial Reality of the Young Professional

Common Challenges

Student Loan Debt: A heavy onus for the young workforce.

Lower Starting Salaries: Aspirations vs. current salary is always a conflict.

High Cost of Living: Being so even more in the cities.

Lack of Financial Education: Money management is typically not part of an official curriculum.

Peer Pressure/Lifestyle Creep: Keeping up with the spending of pals can put your finances in a bind.

Shaky Economy: Swings in the job market and at the pump can add to frayed nerves.

The Advantage: Time!

The biggest advantage you have as a young professional is time. Beginning your financial planning process early helps you realize the magic of compounding that adds to your wealth to a great extent in the long term.

Step 1: Take Control of Your Cash Flow with A Great Budget

Why Budgeting is Essential

Budgeting is the cornerstone of any financial planning. It gives clear insight into where your money is going, and ensures that you’re able to reach all your personal spending and savings goals.

Understanding Income & Expenses

Net Income vs. Gross Income: Understand the gap between what you make and what you keep.

Fixed vs. Variable Expenses: Determine what you COULD spend, compared to what you NEED to spend:

Famous Budgeting Methods For The Young Professional

50/30/20 Rule: Give 50% of your income to needs, 30% to wants and 20% towards savings or debt.

Every Rupee Has a Job – Zero-Based Budgeting: Income – Expenses = Zero.

Envelope System: This one is great for tactile learners and involves using cash to budget.

Tools for Budgeting

You could use an app like Mint or YNAB, spreadsheets or banking apps to track your spending.

Tips for Sticking to a Budget

Automate your savings, keep an eye on your spending, revisit your budget often and adapt when necessary.

Step 2: Lay the Foundations of Your Financial House: The Emergency Fund

What is an emergency fund?

An emergency fund is a sum of money set aside for unanticipated expenses, such as losing your job, a medical crisis or auto repairs.

Why You Need One: Having an emergency fund is crucial for peace of mind and financial security amid challenging moments.

How Much to Save: Really try to save 3-6 months’ worth of basic living expenses this time, adjusting based on your job security.

Where to Keep It: Look into high-yield savings accounts (HYSAs) for liquidity and growth.

Step 3: Tackle Debt Strategically

Identify Your Debts

What are common types of debts?

Prioritize High-Interest Debt

You’ll want to pay off credit cards first because they typically have the highest interest rates.

Debt Repayment Strategies

Debt Avalanche: Repay debt with the highest interest rate first to save the most money.

Debt Snowball: Pay your smallest balance to gain a mental win.

Student Loan Specifics

Know your options when it comes to repayment, to include refinancing and deferment/forbearance (but only if you must).

Avoid New Bad Debt

14 of 19 Practice credit card discipline and know your APRs Whether using a credit card to bridge the gap, always practise credit card discipline to avoid adding to your debt.

Step 4: Begin Investing Young: Your Wealth Turbo Charger

The Power of Compounding (Revisited)

Demonstrate the concept of compounding over time and how an early investment can result in exponential growth later.

Defining Your Investment Goals

Think about your objectives — whether it be retirement, a down payment on a home, or early financial independence.

Understanding Risk Tolerance

Determine how much volatility in your investments you can handle.

Beginner-Friendly Investment Options

Employer: Sponsored Retirement Plans: Like 401(k), EPF, and NPS, if your employer provides a match.

IRAs (PPF/Roth IRAs): Explain tax benefits and flexibility.

Index Funds & ETFs: Perfect low-cost diversification.

Mutual Funds: Diversified portfolios managed by professionals.

Direct Stocks: If you’re willing to do the homework and accept more risk.

Automate Your Investments

Create scheduled contributions to streamline investing.

Step 5: Watching Your Back: Insurance Basics

Why Insurance Matters

But insurance does protect you from unexpected risks that could derail a plan you’ve worked hard on creating.

Young Professionals, 5 types of insurances you should have

Medical Insurance: Most important for accidents and illnesses.

Term Life Insurance: This is a term. Insurance is substantial if you have dependents and/or co-signed loans.

Disability Insurance: Provides income if you become unable to work.

Renter’s/Homeowner’s Insurance: Covers your stuff and liability.

Car Insurance: Compulsory for all owners of cars.

Understanding Coverage and Premiums

You can’t just shop for the lowest price; you need to know you have the coverage you need.

Step 6: Factor in Big Life Events (not Just Retirement)

Buying a Home: Begin saving for a down payment and familiarise yourself with mortgages and property taxes.

Marriage & Family Planning: Think about your shared finances and expenses for the child – for example, schooling and health care.

Career Growth & Upskilling: Put money in yourself to make more.

Wealth Building Mindset: Take a long-term view and resist the urge to splurge.

Step 7: Get Professional Help (When to Find a Financial Planner)

When It’s Beneficial

If your finances are complex, such as when you are high-net-worth or have something unusual like an early retirement, it may be a good idea to seek the help of a financial advisor.

Types of Advisors

Get the distinction between fee-only and commission-based advisors.

What to Look For

Look for certifications (like CFP), experience and a clear fee schedule.

Conclusion

It’s a lifelong process, not a one-time event. When you take control of your personal financial situation now, it becomes a platform on which you can build a better future.

Call to Action

Get started on the journey of financial planning! Download our budget template here for free, and subscribe to get more financial advice.

Frequently Asked Questions

1. How much savings should I be doing as a young professional on a monthly basis?

A good general rule is to save at least 20% of your income, but it varies depending on your personal situation.

2. What are the top financial mistakes young professionals make?

People often fail to budget, rack up high-interest debt and don’t save for an emergency.

3. Which is better, to pay off students loans or think about investing first?

It all comes down to your interest rates and financial goals. For the most part, if you have a low student loan interest rate, getting invested early can pay off.

Swiss Re Institute predicts that a potential impact of rising US tariff policy is slower global economic growth. The reinsurance colossus’ most recent “World Insurance sigma” report, published July 9, 2025 says these protectionist steps will not only hinder global GDP expansion but will also inhibit insurance premium growth internationally.

Explore how US tariffs are set to impact the global economy and insurance premium growth, as analyzed by Swiss Re. Stay informed on key economic trends.

Tariffs to Trigger “Stagflationary Shock”

The global average rate (real GDP growth) is expected to slow to 2.3% in 2025 and 2.4% in 2026, having stood at 2.8% in 2024. This slowdown has been primarily caused by the widening US tariff policy which is causing a ‘stagflationary shock’ to the US, and by extension the broader global economy, and is designed to obliterate policy uncertainty worldwide, the report states.

Jérôme Haegeli, Swiss Re’s Group Chief Economist, pointed to the short-term effect. “US consumers will be the most affected by US’ tariff policy and cut their consumption because of increased prices. This will in turn bear down on US growth which is largely driven by household consumption.” Swiss Re expects a slowdown in US GDP growth to just 1.5% in 2025 after 2.8% in 2024.

“Additional tariffs would lead to structurally higher inflation in the United States” as supply chains become less efficient and domestic industries face reduced competition from other countries, the report said. This mix of weaker growth and accelerating prices creates a thorny new world for businesses and consumers.

Insurance Premium Growth to Halve

There’s to be a ripple effect from a lightened global growth and increased uncertainty, and the insurance sector like no other will suffer. Global insurance premium development will slow down considerably to 2% in 2025, about half of the 5.2% seen in 2024, according to projections by the Swiss Re Institute. In 2026, a low partial recovery to 2.3% is expected.

Premium growth down in both life and non-life segments:

Nonlife growth of premiums is forecast to fall to 2.6% in 2025 from 4.7% in 2024 as competition in personal lines and softening market in some commercial lines.

The pace of growth in life insurance, in particular, will cool even more sharply, with premiums rising 1% in 2025, down from a 6.1% increase in 2024 — higher interest rates are set to moderate.

US tariff policy is another step toward increasing market fragmentation longer-term, which would decrease insurance affordability and availability, and thereby global risk resilience, Haegeli cautioned.

Trade barriers potentially leading to higher claims costs for insurers and supply chain disruptions, and cross-border flow of capital restrictions on reinsurers that may lead to capital allocation inefficiencies and higher capital costs and, ultimately, higher insurance pricing, are cited in the report.

Uneven Impacts and Emerging Opportunities

While the tone is in general cautious, the report states that the impact of tariffs on the insurance sector is likely to depend on geographic regions and lines of business.

US Motor Physical Damage This insurance sector is anticipated to bear the brunt of the tariff rise with auto parts and new/used cars prices surging and hence higher claims severity. Swiss Re predicts US motor damage repair and replacement costs will rise by 3.8% in 2025.

Our commercial property and homeowner and engineering lines in the US could also experience an increase in claims severity coming from higher costs for the intermediate goods, machinery, and commodities.

Tariffs outside the US are usually thought to be more disinflationary and could reduce claims pressure.

But the added uncertainty and economic disruption could also present opportunities, and credit and surety insurance that guard against economic disruption might be in higher demand. Alives could affect marine insurance as well, given changes to trade routes and supply chain realignments.

Notwithstanding the decline in premium growth, Swiss Re says that the overall profitability position of the global insurance industry remains robust, benefiting principally from ongoing investment income gains.

Yet the report is a stark reminder of how international trade policies and protectionism can have such widespread economic implications for wider global growth and important sectors, such as insurance.

There’s a shake-up occurring in the U.S. mortgage market, and it’s regarding something you might not think about very often — credit scores. A large portion of home loans are being paid with money from investors.

Described by the Federal Housing Finance Agency (FHFA) on July 8, 2025, and supported by the European Parliament on July 10, 2025, the landmark decision looks to spur competition, lower costs for consumers and push homeownership opportunities to millions of Americans.

The implications of a new credit score alternative gaining approval for mortgages. Learn how this challenger to FICO could benefit borrowers.

Breaking FICO’s Monopoly

FICO (FICO) scores have long been the gold standard for home mortgages bought and sold by government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, which back most home loans in the US. With the acceptance of VantageScore 4.0, the monopoly to be the only credit score in town has been shattered, welcoming the beginning of a new era of competition in the credit scoring environment.

FHFA director William J. Pulte (Bill Pulte) made this announcement on social media, writing in a post on his official page that “Effective immediately,” lenders working with Fannie Mae and Freddie Mac can opt to use VantageScore 4.0. He stressed that this action is in line with President Donald Trump’s “landslide mandate to decrease costs” and raise competition.

What VantageScore 4.0 Offers

VantageScore 4.0, created by the three major credit bureaus (Equifax, Experian, and TransUnion), includes some important changes that should amplify the number of people benefiting from them:

Inclusion for “Thin Files”: One of the biggest benefits of VantageScore 4.0 is that it can score more consumers, especially people with little credit history, or “thin files”. It does so by including additional data points like rental payments, utilities, and telecom payments in the mix. What that means is that timely payments for these vital services can now be used to create or enhance a borrower’s credit profile for a mortgage. It’s a game-changer for people who don’t have traditional plastic credit cards or long loan histories.

Trended Data Analysis: Instead of providing a “snapshot” of credit at a moment in time, like old FICO models, VantageScore 4.0 uses “trended data”. This lets lenders view trends in a consumer’s financial planning over time, including whether credit card balances are being reduced consistently or minimum payments are made most of the time. This “video” of credit history has the potential to paint a much richer risk assessment.

Potential Cost Reductions: Introducing competition for the purchase of credit scores likely will reduce licensing fees for credit scores, lowering costs for lenders and potentially benefiting consumers with lower origination fees or interest rates.

Impact on Homebuyers and Lenders

The immediate impact is significant. VantageScore also says that its use would help an additional 4.7 million potential homebuyers, including first-time buyers, people of colour and those with an income on the low end of the scale, who cannot get a mortgage using scores supplied by the three national credit bureaus.

For lenders, it means added flexibility and possibly less expensive access to credit reports, as the tri-merge (three-bureau) infrastructure is staying in place, making for a simpler move over. The move is being widely cheered by housing advocates and industry participants like the National Association of Realtors (NAR) for putting more credit options in the hands of consumers and burning off some sluggish competition.

But some experts warn that lenders could still take a more cautionary approach with borrowers who don’t have a traditional credit history, perhaps leading to slightly wider interest rates in today’s market. But certainly, this is a big step toward modernizing the U.S. mortgage market, making homeownership more accessible for a wider swathe of the population.

The FHFA’s move implements the 2018 Credit Score Competition Act — signed into law by then-President Trump — delivering on a long-time goal of modernizing the credit scoring system.

JGB yields have climbed to multi-decade geographical peaks, with the 10-year benchmark yielding more than 1.595% on Tuesday, July 15th, 2025, a level not seen since just before Halloween, October 2008.

Japan’s bond yields reach multi-decade highs amid rising fiscal concerns ahead of the upcoming election. Discover the implications for investors and the economy.

The spike in yields, especially on the far end of the curve, is a reflection of growing investor concern over Japan’s fiscal state and the prospects for additional government spending as preparation for the pivotal Upper House election on Sunday, July 20, heightens.

Record Highs and Market Instability

The 30-year JGB yield, a bellwether for long-term fiscal health, surged to an all-time 3.195% on Tuesday, and the 20-year yield rose to 2.65%, its highest since November 1999.

The rapid movement reflects rising strains in a Japanese government bond market that has been unusually stable in the past, anchored by the BoJ’s ultra-accommodative monetary policy. The rapid rise in yields is a troubling one for a country with the largest public debt-to-GDP ratio in the developed world, which comes in at around 250%.

Although the majority of Japan’s debt is held at home, any slackening in appetite from institutional buyers, who fund themselves at a spread over the JGB market, along with the BoJ’s ongoing gradual reduction of bond purchases, is increasing the vulnerability of the market.

Fears About the Economy Before the Election

The approaching race for the Upper House is a big factor behind the bond market sell-off. Japanese Prime Minister Shigeru Ishiba’s ruling Liberal Democratic Party (LDP) and its junior coalition partner Komeito are facing a difficult challenge, with local polls indicating they will struggle to win a majority in the chamber.

The possibility of a weakened ruling coalition or political continuity is stoking fears about continued budget generosity. Opposition parties, riding the wave of platforms that promise to tackle surging living costs, are pushing for steps like consumption tax advisory reductions. Such policies, although popular with voters, would also widen the fiscal deficit, making Japan’s already stretched finances even worse.

“As the volume is building around noise going into more fiscal spending, we took an underweight on Japan in general,” said Ales Koutny, head of international rates at Vanguard, speaking to the UK bond market’s headaches in recent years.

BoJ’s Delicate Balancing Act

The Bank of Japan is in a ticklish situation. Following its unconventional yield curve control (YCC) policy exit and, now, slow interest rate hikes (the cash rate sits at 0.5%), the central bank targets a sustained 2% inflation.

But ramped-up fiscal spending could unravel all of this and leave the BoJ with little choice but to engineer monetary tightening faster than the pace most households and firms would be happy with. Even though the Ministry of Finance tried to cool things down by stating that it intended to cut 20-, 30- and 40-year debt sales to help mend supply-demand imbalances, the real issue is fiscal.

“If a demand-less market continues and if investors see no rate hikes within this fiscal year, JGB volatility will go up, especially in the long end,” said Kentaro Hatono, a fund manager at Asset Management One.

Everything now depends on the result of Sunday’s election. A major defeat for the ruling coalition may lead to another sell-off in super-long JGBs as investors bet on a massively swollen government deficit.

The surge in yields, which have been rising steadily since the summer, has the potential to raise the cost of corporate loans and mortgages, in turn dampening domestic economic growth. Japan’s bond market readies for a volatile phase, with the election set to determine its fiscal course for years.

It’s today, July 15, 2025. Stock futures, by the way, are up early in the morning on economic growth out of China, which is coming in better than expected, and renewed optimism about strategic manoeuvres for NVIDIA in China.

Persisting concerns over the next round of US inflation figures and the ongoing, expanding repercussions of US tariff policies on global trade are taking the edge off the positive push.

NVIDIA’s China Plan Offers a Glimmer in Technology’s Gathering Gloom

Technology stocks, particularly in semiconductors, are being actively bid in pre-market as a major change to NVIDIA’s China plans is released. The AI chip giant said on Tuesday that it will resume sales to China after the US government committed to grant licences. In accordance with U.S. export law (ALUMINIUM RAM HERE WE COME), the H20 chip is a downgraded (crippled) edition specifically for the Chinese market.

On top of that, NVIDIA announced a new RTX Pro GPU model optimised for AI use in logistics and smart factories and is optimised for Chinese regulatory requirements. As does Nvidia CEO Jensen Huang visiting with US and Chinese officials to promote AI cooperation, the ANT says. “This action will serve as crucial support in ensuring Nvidia’s leading position in the Chinese market,” the ANT says. The news also helps clear up some concern among investors over how export restrictions might affect NVIDIA’s earnings, with this development setting up a bright outlook not just for the company but for the broader tech industry.

China’s Q2 GDP Beats Forecasts

Bullish sentiment also was lifted by a stronger-than-expected report on China’s economy in the second quarter. Official figures for China showed the country’s gross domestic product was up 5.2 per cent from the 2024 period during the second quarter, April through June. While it surpassed analysts’ predictions of a 5.1 per cent increase, it suggested resilience despite lingering domestic challenges and international trade pressures.

Robust exports were partly to blame for the better-than-forecast showing, with Chinese firms reputedly front-loading shipments to get ahead of looming US tariff cut-off dates. The Q2 data is a welcome pick-up in global risk sentiment, particularly in emerging markets which are vulnerable to the fortunes of the Chinese economy, although analysts warn the second half of the year could see a slowdown as domestic demand weakens and the real estate sector has problems.

Shadows Linger: Tariff & US Inflation A lack thereof of Uncertainty

“The global markets are still vacillating, waiting with bated breath for the release of the US CPI report for June 2025 tomorrow, bad news from China and the good from NVIDIA notwithstanding,” Wadhwa said. As inflation figures are likely to play a crucial role in future decision-making on interest rates at the Federal Reserve, that data is causing an outsized response from investors. The dollar, bonds and stocks could all become volatile if there is a large deviation from expectations.

Adding to the uncertainty are U.S. policies of tariffs on the rise. President Donald Trump’s administration stepped up trade tensions by sending warning letters on the tariffs to more than 20 countries and free trade zones, including some of foes and closest allies.

Saxony’s Economy Minister Martin Dulig warned of “serious negative effects for the auto industry” if bilateral trade pacts could not be reached by August 1, when 20%-50% tariffs would be introduced. Analysts forecast that this will hit the US economy with a “stagflationary shock”, pushing up inflation at home and triggering havoc across global supply chains. The future of global investment and trade is also complicated by the potential for retaliatory measures.

Though tech optimism and China’s surprising economic resilience are providing some tailwinds to the trading day, investors are finding comfort from broader concerns about U.S. inflation and the fickle nature of global trade policy.

Have you ever wondered how a bank determines whether you qualify for a loan or how an insurance company decides what to charge you for coverage? You can thank something called underwriting.

This critical measure essentially assesses the risk involved with a venture, a loan, an insurance policy, or an investment for a fee. In this report, we’ll explain the different types of underwriting, how they operate, and why they’re essential to banks and the stability of markets.

What is Underwriting? The Foundation of Financial Decisions

Underwriting is when an individual or institution takes on financial risk for a fee after working to evaluate the risk associated with a particular venture, loan, or investment.

Role of an Underwriter

This critical judgement call is made by underwriters, the experts who are doing the evaluating. Their core purpose includes:

Eligibility for loans, insurance and investments.

Risk quantification and pricing, including interest rates, premiums and prices of securities.

Protecting the underwriter or bank from potential losses.

Historical Context

Derivative Origin The term “underwriting” comes from a shipping insurance practice whereby two or more parties would sign under the risk, denoting that they had underwritten their names underneath the description of the risk, and were accepting it.

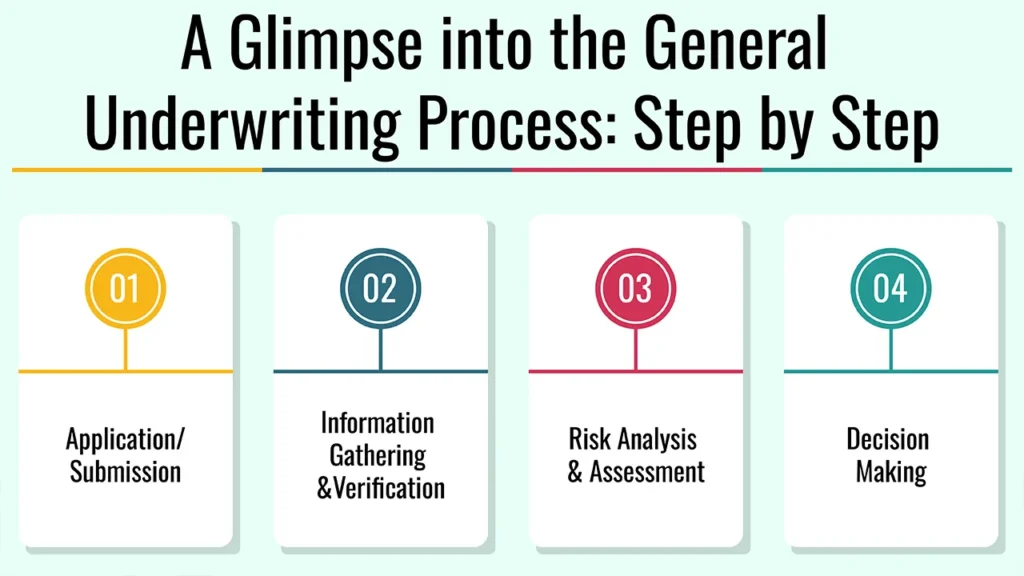

A Glimpse into the General Underwriting Process: Step by Step

1. Application/Submission

The whole process of underwriting commences with the application for a loan, insurance, or other security.

2. Information Gathering & Verification

Interest and Other Collection: That’s for those financial statements, credit bureau reports, medical data, property valuation and business plans.

Confirmation of Accuracy: Underwriters confirm the accuracy and completeness of the submitted data.

3. Risk Analysis & Assessment

Analysis: Processing data using models, algorithms and human analysis.

Risk Identification: Assessing the probability and effects of risks.

Creditworthiness: Measuring a candidate’s creditworthiness/risk.

4. Decision Making

Approved: With rates, terms, or premiums Other specific terms, rates or premiums.

Conditional Approval: Additional information or conditions requested; Not all criteria have been met.

Refusal: If the risk is considered to be too great.

Pricing/Terms Setting

Setting interest rates, premiums, or prices of securities according to perceived risk.

Type 1: Origins, Loan Underwriting – Definition of Creditworthiness.

Definition

Loan underwriting is the procedure for determining the borrower’s ability to pay and their creditworthiness.

Key Factors Assessed (The “5 Cs” of Credit)

Character: Reputation, how you have paid other people in the past.

Capacity: Debt-to-income ratio, steady income and ability to repay.

Capital: Money or savings, assets, down payment.

Collateral: The value of assets offered for security (secured loans such as mortgages).

Common Sub-Types

Mortgage Underwriting: Focus on the borrower’s financials and property appraisal.

Personal Loan Underwriting: Emphasis on credit history and debt-to-income.

Auto Loan Underwriting: Looks at borrower credit and value of car.

Business Loan Underwriting: Requires a deep dive into business financials, industry and management.

Automated vs. Manual Underwriting

Technology is a factor in loan underwriting, but human underwriters remain essential for complex cases.

Type 2: Insurance Underwriting – Assessing Insurability and Risk

Definition

Insurance underwriting is the process of evaluating the risk of insuring a particular person or asset in a particular portfolio and then determining the terms of insurance (called pricing/products).

Goal

The main objective is to position the company to pay for claims with a profit while providing coverage on a fair basis.

Key Factors Assessed

Life Insurance: Age, health (medical background, lifestyle patterns), where you work and your family medical history.

Medical cover: the medical history, pre-existing conditions, the age, and the lifestyle.

Property & Casualty Insurance: Driving record, claims experience, location of the property, type of property, condition of the property, safety features.

Business Insurance: Your industry, claims history and safety measures.

Outcomes

Approval (standard premium)

Approval (loaded premium/special conditions)

Denial

Type 3: Underwriting Securities (Bringing Assets to Market)

Definition

The issuance and sale of new securities–stocks or bonds–is often called underwriting because the process is usually led by investment banks. The underwriter takes on the risk of not being able to sell the securities.

Primary Market Role

This process is especially important for IPOs and follow-on offerings.

Types of Securities Underwriting Agreements

Firm Commitment: The underwriter purchases the entire issue from the issuer and then resells it to investors, taking on full risk.

Best Efforts: The underwriter stands as agent for the issuer, committing itself only to use ‘best efforts’ to sell the issue and does not guarantee the sale of all of the securities. Risk of Unsold Shares The issuer takes on the risk of any unsold shares.

All-or-None: A type of “best efforts” offering in which the entire issue is cancelled if the underwriter is unable to sell all of the securities.

Syndicate: A syndicate is frequently organised, consisting of several investment banks in order to share the risk of large issues.

Process

This involves monitoring issuers, valuing and pricing securities, and marketing and distributing securities issues.

The Significance and Development of Underwriting

1. Risk Management

Underwriting stops banks from taking too much risk, and maintains stability in the market.

2. Market Stability

(b)/(c) It promotes the proper flow of capital and aids investors, by establishing rates and premiums commensurate with the risk of other investors.

3. Technological Advancements

Automated Underwriting Systems (AUS): Improves the ease of preparation of routine cases.

Big Data and AI: Towards better risk predictions and personalized interventions.

Alternative Data: Using sources of non-traditional data to judge creditworthiness (e.g., utility payments, rental history).

Human Element

As much as technology helps us, complex cases do need seasoned human underwriters to take an informed call.

Conclusion

To sum it up, underwriting is pervasive in finance and forms the basis of educated finance decisions. It promotes market trust and stability, allowing institutions and individuals to fight financial risk management well.

Call to Action

Continue researching how to manage your risk and meet with a financial advisor to understand your underwriting criteria, and learn more about a career in underwriting.

Frequently Asked Questions

1. Who is an underwriter?

An underwriter is a professional who determines the risks of loans, insurance or investments.

2. What is the purpose of underwriting?

The purpose of underwriting is simply to mitigate the risk of a financial decision and to guarantee that the institution is able to cover potential losses.

3. Can I appeal the underwriting decision?

In some cases, underwriting decisions can be appealed – particularly if new information is provided that could impact your ranking on risk.

Have you ever registered for the trip of a lifetime, only to fret that unforeseen circumstances may force you to cancel? If so, you’re not alone. A number of travellers are also dealing with unknowns that have the potential to interrupt their travel plans and cause financial damage.

That’s where Cancel for Any Reason (CFAR) insurance comes in. In this article, we’re going to define what CFAR is, discuss how it works and its potential limitations, and help you figure out if it’s worth it for you or not.

Defining CFAR

Cancel for Any Reason (CFAR) insurance is a travel insurance plan add-on that provides the option to cancel for any reason, even if it’s not listed in the base policy.

While most travel insurance plans are triggered by specific named perils, a CFAR policy lets you cancel your trip for almost anything, offering you all but psychic protection when making travel decisions.

More Than Just Standard Trip Cancellation: CFAR Explained

Standard Trip Cancellation

Traditional trip cancellation insurance generally covers specific, named perils, like illness, injury, natural disasters or job loss. For instance, if you get sick before your trip, or a hurricane is threatening your destination, regular trip-cancellation insurance can reimburse you for your nonrefundable costs.

The CFAR Advantage

The advantage of CFAR is the ability it gives you to cancel for virtually any reason, even one that is not on the list in a standard policy. Here are some scenarios wherein you might be able to cancel with CFAR to the tune of something that isn’t protected by regular insurance:

Change of plans; you’re not in the mood to go.

Job or scheduling issues that arise unexpectedly.

Unsafeness or uneasiness related to a destination (e.g., political turbulence, health reasons, such as new outbreaks).

A friend or non-“covered family member” gets sick.

Your travel partner can’t make it, and you don’t want to travel alone.

Passport delays or visa issues.

Simply changing your mind.

How Does Cancel for Any Reason (CFAR) Insurance Work?

1. Add-on, Not Standalone

CFAR is usually an “upgrade” to a standard travel insurance policy, not a stand-alone policy. That’s because you’d be required to purchase a standard travel insurance policy first, and then buy supplemental CFAR coverage.

2. Purchase Timeline

It’s also worth mentioning that there’s a limited amount of time when you can buy CFAR; typically, it’s 10-21 days after you make your first trip deposit. That is, you must take action soon after booking your trip.

3. Insuring 100% of Trip Costs

The majority of CFAR plans stipulate that you need to insure 100% of your prepaid, nonrefundable trip costs in order to qualify for coverage. Therefore, you are fully protected if you need to cancel.

4. Cancellation Window

Most CFAR policies have a deadline for cancellation and it’s almost always a cancellation at least 48 hours before your planned departure.

5. Reimbursement Percentage

Unlike traditional cancellation policies, which would pay 100% of the cost of your trip if you have a covered reason to cancel, CFAR plans generally provide on 50%-75% of your insured trip costs.

6. Claim Process (Simplified)

In general, filing a CFAR claim is simple. You will need to submit a report of cancellation notice and other proof you consider necessary to justify your claim.

Advantages of Having CFAR Insurance

1. Unmatched Flexibility

The single greatest feature of CFAR is the incredible flexibility it provides. You can cancel for ANY reason up to the day before you travel and still get 100% of your money back (even if you have “I do not want to book a trip” coverage).

2. Financial Protection

CFAR protects a large portion of your non-refundable investment, so that in case you have to cancel, you don‘t lose the money you worked hard for.

3. Peace of Mind

CFAR insurance takes the stress and worry out of planning costly trips so far in advance. Plan your travel with confidence, knowing that you have a safety net.

4. Ideal for Uncertain Times

In a world of potential global uncertainty, CFAR is extremely timely today. It’s a cushion for travellers finding themselves in a precarious situation.

5. Protects High-Value Trips

CFAR can be most useful for costly international trips, cruises or tours – when the financial risk management is greater.

Downsides and Caveats to CFAR Insurance

1. Higher Cost

One of the downsides of CFAR is that it can significantly hike up the price, usually making the policy 40-60% more expensive than regular travel insurance.

2. Partial Reimbursement

It’s worth noting that CFAR doesn’t pay a 100% refund. In most cases, you will get only a portion of your trip costs back.

3. Strict Eligibility Requirements

CFAR policies have stringent eligibility requirements, including timing on when you bought the insurance and a requirement to cover the entire cost of the trip.

4. Not Available in All States/Regions

Both availability and terms may vary by insurer and location, and some states may not offer CFAR insurance at all.

5. Exclusions

“Any reason” is a big field, but there might be some or two rare exceptions. Don’t forget to read the fine print to know what’s not covered by a policy.

Who Should Consider CFAR Insurance?

1. Travelers with High Non-Refundable Costs

If you’re an individual or family whose flights, tours or accommodations are costly, then you may want to invest in CFAR to cover your investment.

2. Those with Unpredictable Schedules

Business travellers, people with high-pressure jobs, or those with family obligations that may be subjected to change could also appreciate CFAR’s flexibility.

3. People with Health Concerns

Traditional policies are good for illness that is not known of ahead of time, CFAR is a safety net for non health specific conditions, or pre-existing conditions (if no waiver is signed).

4. Anyone Seeking Maximum Flexibility

Those who appreciate the flexibility to change their mind without an egregious financial penalty stand to benefit most from CFAR.

5. Those Planning Far in Advance

The further in advance the planning, the more ability there is to absorb unanticipated events, so that was prudent (IMO) for the early planners to do.

How to Choose a CFAR Policy

1. Compare Providers

Compare CFAR policies from different insurance companies to ensure you have the greatest coverage for your unique requirements.

2. Understand Reimbursement Percentages

Seek the most variable percentage, such as 75%, rather than 50%.

3. Check Eligibility Requirements

Double-check that you meet the purchase timeline and full trip cost insurance requirements before purchasing a policy.

4. Read the Fine Print

Do remember to read the policy document for exact terms and conditions and any small print exclusions to avoid surprises at a later stage.

5. Consider Your Trip Details

Match that policy to your individual travel needs and your potential for risk, so you aren’t left without coverage.

Conclusion

In conclusion, travel insurance with CFAR allows for a special form of protection that affords flexibility and peace of mind to travellers. Though it may be an added cost, you’ll have peace of mind along with the ability to cancel for any reason. If you have a trip and want to protect your investment, look into CFAR.

Call to Action

Review CFAR benefits for your next journey, get a free quote now and learn more about TravelSafe’s comprehensive travel insurance coverage to support your trip. CFAR travel insurance, peace of mind travel, protect your vacation

Frequently Asked Questions

1. Can I purchase CFAR insurance after I’ve paid for my trip?

Normally you have to have purchased CFAR insurance in 10-21 days of you first payment.

2. Is CFAR available for pre-existing conditions?

Indirectly, CFAR allows you to cancel for issues which may be related even when you do not have a waiver in place, but it is not medical coverage itself.

3. Is CFAR insurance actually worth the extra cost?

It’s really down to your personal risk tolerance, the cost of the trip and how much flexibility you need. For lots of folks who spend time on the road, the peace of mind is worth the cost.