As of its most recent readings, which were published, the Global Economic Outlook Dampened by Trade Protectionism on July 8 stresses the overall impact caused by the increased introduction of trade protectionist measures, so things are not going to get much better anytime soon.

In this difficult environment, central banks around the world face the dilemma of having to be vigilant while trying to strike the right balance between supporting growth and controlling inflation in a time of greater uncertainty. The tug of war between these forces is charting a treacherous and uncertain course for the world economy.

The Potential for Global Growth Is Threatened by Protectionism

Trade protectionism in the form of tariffs, non-tariff barriers, and retaliation is resulting in a bleak global economic outlook. Almost all of the economic leading indicators have released updated projections recently, and they all agree there will be a negative effect on global trade volumes and GDP.

If we take the World Bank, for example, they forecast global GDP growth to drop to 2.3% for 2025, a substantial revision downwards largely due to rising trade barriers and policy uncertainty. This has resulted in weakened corporate confidence, broken international supply chains and depressed investment.

Enterprises are suffering from high costs and uncertain market availability, and that combination has quite naturally discouraged cross-border investments. The BIS emphasized that trade-related headwinds are strengthening established trends toward economic balkanization, intensifying a weakening of economic and productivity growth that has now lasted the better part of a decade.

Central Banks Stay on Alert Despite Conflicting Pressures

In such an environment, central banks are crucial and are “vigilant” or “closely watching” data and willing to act forcefully. They now face a twin challenge of a slowdown in growth, exacerbated by trade protectionism, that could also push them to ease monetary policy.

On the other hand, persistent inflationary pressures, possibly exacerbated by trade barriers driving up import costs, prevent them from loosening policy too rapidly. The general theme is one of caution, however, and central banks are taking slightly different stances depending on their own domestic economies.

Take, for example, the European Central Bank (ECB), which has acknowledged that while disinflation is in progress, the continued intensification of trade pressures complicates the inflation horizons, causing them to adopt a data-dependent approach to politics.

The vigilance is important as to how trade-offs are balanced to support economic activity and ensure price stability; it can be a difficult one to make. For more on the ECB’s monetary policy and outlook, see the European Central Bank’s official statements and publications.

Navigating the Delicate Balance: Growth, Inflation, and Policy Uncertainty

Keeping vigil for central banks, or so it is frequently the case, entails walking a tightrope. Should global growth continue to decelerate because of trade protectionism being sustained, the chorus calling for rate cuts will grow louder.

Yet if inflation proves more persistent or speeds back up again via supply shocks caused by trade disruptions or higher import prices, rate hikes could still be in play. The uncertainties created by trade protectionism are very challenging when taking such decisions, with little firm ground upon which to base economic projections and policy decisions.

This uncertainty also applies to financial markets and consumer spending, making the calculus even more complicated. Businesses are reluctant to make job-creating investments, while consumers may put off big purchases, dragging on economic momentum.

Even more than in the Vietnam era, central banks need to understand the changing landscape and ways in which trade policy affects import prices and overall demand to better achieve their mandates.

Outlook remains cautious, policy cooperation crucial

So long as trade protectionism is still on the table, the short-term global economic picture is going to look dim. Meanwhile, international financial companies are also cautious, as risks on the downside are high.

International cooperation is the key means to solve trade rows. Returning to more market-orientated policies, including encouragement of private investment, could have a substantial positive effect on the economic environment by repairing confidence, supply chains and capital appreciation.

Central banks are here to stay, adjusting their monetary policy as new data comes in, striving for price stability as well a sustainable growth. It will take their alert and data-oriented approach to navigate economies through such uncertain times, but also global policy cooperation for more resilient market insights and economic outlooks in the future.

In their most recent reports, which were released today, the Global Growth Slowdown Confirmed by World Bank and OECD; Trade Barriers Impact Investment Flows on July 8, 2025, concur that there has been a significant drop in global growth.

This slowing is directly tied to the deleterious spread of rising trade barriers and their knock-on impact on world investment. The news draws attention to an economic uncertainty on the horizon for companies and countries struggling to navigate a more splintered world order.

The World Bank’s grim forecast indicates a clear slowdown through 2025.

The World Bank published its latest report on the global economy, the Global Economic Prospects, and the general narrative remains a pessimistic one: The institution has just cut its outlook for global GDP growth to 2.3% in 2025, a significant reduction compared to previous expectations.

That would be the weakest rate of non-recessionary growth in about two decades. The key factors highlighted by the World Bank primarily reflect the high contribution of increased trade tensions and policy uncertainty to the slowing of global growth.

“The 0.9 per cent drop is the weakest performance since 2001, excluding global recessions,” Indermit Gill, chief economist of the World Bank Group, said at a press briefing.

The World Bank also said that world growth projections have been downgraded in nearly 70% of economies, a comment that serves to emphasize the widespread slowdown and the vulnerability of the world recovery to trade barriers.

The OECD Highlights the Growth-Stifling Effect of Trade Protectionism

Reinforcing the World Bank’s view, the OECD’s recent Economic Outlook further attests to the global deceleration in growth. Especially striking in the OECD’s examination is the pernicious effect of widening trade barriers and protectionist measures in contributing to the slowdown. The organization now projects that global expansion will decelerate from 3.3 per cent in 2024 to 2.9 per cent in both 2025 and 2026.

These actions are directly affecting business confidence, disturbing global supply chains and, importantly, redirecting or pausing committed investment. “Policy uncertainty today is holding back trade and investment, undermining consumer and business confidence and slowing the pace of global growth, according to the latest OECD Economic Outlook.

There is a need for governments to discuss any concerns with the global trading system in a positive and constructive manner – keeping markets open and retaining the economic benefits of rules-based global trade for competition, innovation, productivity, investment and wealth growth,” it adds.

Global Investment Flows Choke With Trade Tensions

Both reports underscore how the kind of uncertainty introduced by trade frictions is having a chilling effect on investment, especially foreign direct investment (FDI). It was reported that companies are delaying their expansion and startup plans and thinking again about cross-border projects because of uncertain trade policies, increasing costs and possible market access losses.

UNCTAD’s World Investment Report 2025 also revealed that global FDI has fallen by 11% in 2024, the second year of consecutive decline (UNCTAD, 2023b), confirming the deepening of the slowdown in the flow of productive capital. For the full World Bank “Global Economic Prospects” report, visit the World Bank’s official publications page.

Lower investment also means slower job creation, less technological innovation and a weaker growth potential for the future ‐ all magnifying a global slump. The decline in global trade and the disintegration of the global value chains that began in the 2010s have led capital to become risk-averse – it is seeking domestic predictability over international contortions in the context of higher protectionism and geoeconomic provocations, from industrial plants to R&D centres.

Outlook and Policy Imperatives

Conditions are still difficult, with the institutions calling for quick and coordinated action. The message from the WB and the OECD is unequivocal; if the current trend of escalating trade restrictions and policy uncertainty continues, the world economy will enter a period of prolonged, anaemic expansion.

The policy implications are clear, centring on the pressing need for unwinding trade frictions and building a more stable global economic environment which will revive investment flows and address the broader global growth deceleration. Multilateral initiatives are the key to returning to a stable and rules-based world trade system. The stability of the world economy depends on international cooperation to steer these choppy economic seas. Sources

Is owning a home, sending your kids to college, or travelling around the world on your bucket list? These “big financial goals” may feel intimidating, but with the right strategies, they’re totally within reach.

This in-depth guide will help you to “How to Save Money for Your Big Financial Goals” successfully. We’ll unpack and refactor practical tactics, looking at the best tools and the most effective action steps in order to minimise the hurdles you encounter in your path to financial freedom.

Section 1: The Basics: Knowing Your Objectives and How to Save Money for Your Big Financial Goals

Step 1: Know Your “Why” – Having Clear Financial Goals

Vague ends produce vague means. You need to get specific to reach those money dreams. Employ SMART goals: Specific, Measurable, Achievable, Relevant, and Time-bound.

Actionable Advice:

Short-term (1-3 years): Save for an emergency fund, add to that rainy day fund, or take a holiday.

Mid-term (3 to 10 years): Save for a down payment on a home, buy a car, or pay for education.

Long-term (over 10 years): prepare for retirement, your child’s wedding, or leave a legacy.

Example: Rather than declaring, “I want to save for a house,” say, “I want to save $20,000 for a down payment by June 2028.” Learn how to set SMART financial goals effectively from Fidelity.

Step 2: Take a Look Around Your Financial Landscape

It’s important to know where you are in the beginning. You can’t make a good plan if you don’t know what you’re dealing with.

Actionable Advice:

Get a Handle on Income & Expenses: For a month, keep track of where your money really goes, using apps, spreadsheets or notebooks.

Figure Out Your Net Worth: Deduct what you owe from what you own to assess your overall financial condition.

Review Your Current Savings/Investments: See what’s working for you and what’s working against you.

Section 2: Smart Saving Strategies: Get the Ball Rolling

1. Create an Effective Budget (and Stick to It)

A budget is not a straightjacket; it is a tool to empower you and guide your money toward that which is most important to you.

Actionable Advice:

Zero-Based Budgeting: Give every dollar a job.

50/30/20 Rule: 50% should go toward needs, 30% for wants and 20% for savings or debt repayment.

Find ‘Money Leaks’: Think of little things you pay for every day — coffee, subscriptions you don’t use, impulse buys. The bottom line: You do have a choice: Scale back on the discretionary spending that doesn’t advance your goals.

2. Automate Even Saving – “How to Pay Yourself First”!

Remove willpower from the equation. Make saving automatic.

Actionable Advice:

Establish a recurring transfer from your cheque account to your savings or investment or retirement accounts on payday.

Invest in mutual funds or counterparts whereinyou invest through SIP (Systematic Investment Plan) as per the availability in your country.

You may also want to consider RDs with your bank for certain objectives.

3. Grow Your Income (Side Hustles & Upskilling)

You can only cut so much. Earn more to save more.

Actionable Advice:

Negotiate a Raise: Figure out what people in comparable positions are earning and show your manager why you deserve it.

Diversify Your Skills: Fortunately, upskilling is a common theme in the tech industry.

Get a Side Job: Think about freelancing, tutoring or online selling. A few dollars more per month can really add up in your savings.

4. Manage Your Debt Well

High-interest debt — credit card debt and personal loans — is contradictory to your savings goals.

Actionable Advice:

Focus on High-Interest Debt: Attack it head-on using something like the debt snowball or avalanche.

Refinance Loans: Research how interest rates can be reduced on current loans.

5. Motivate Saving through Gamification and Rewards

Staying motivated is key. Approach saving as if you’re trying to beat a challenge or a game.

Actionable Advice:

Savings Challenges: Attempt the 52-week challenge or establish no-spend days.

Picture Goals: Place pictures or reminders of your goals somewhere you can see them.

Incentive Milestones: Reward yourself for meeting smaller goals without risking setbacks.

Section 3: Smart Tools and Where to Put Your Money

Aligning Your Money With Your Goal’s Timeline

For Short-Term Goals (1-3 years):

Instruments: A high-yielding bank savings account, bank FDs for assured returns, and short-term debt funds.

Why: Safety and liquidity are key; do not subject yourself to market fluctuations.

Why: To achieve growth with a comparative degree of risk.

For Long-Term Goals (10+ years):

Tools that can be used: diversified equity mutual funds (large-cap, flexi-cap), index funds, National Pension System (NPS), Public Provident Fund (PPF) and direct equity (for experienced investors).

Why: To make the most of compounding; can tolerate market swings.

Tax Considerations: Growing savings early with tax-advantaged investments (such as ELSS, NPS and PPF) can help in saving tax that way.

Section 4: Conquering Typical Savings Obstacles

Staying on Track When Things Get Tough

Challenge 1: Lack of Motivation/Discipline:

Solution: Revisit your “why”. Employ visualisation and measure your results. Keep Morale Up By Celebrating Small Wins.

Challenge 2: Unexpected Expenses:

Solution: That’s what your emergency fund could be used for! Turn it on when you need to, and then recharge it. Avoid touching goal-specific savings.

Challenge 3: Lifestyle Creep:

Solution: Don’t spend significantly more as your income increases.” Instead, automatically increase your savings.

Challenge 4: Overwhelm:

Solution: Divide and conquer, by setting smaller, more manageable goals. Concentrate on one or two important goals at a time.

Conclusion: Your Journey, Your Success

So how do you actually go about saving money for your biggest financial goals? In sum: You do so by defining your goals, budgeting efficiently, automating your savings, raising your income, dealing smartly with debt, and selecting the right tools for the time horizon for your plan.

“Saving money for your big financial goals” isn’t at all about deprivation; it’s just about making conscious choices today that empower your future self. And by employing these “smart saving strategies”, you’re doing more than just saving money; you’re creating that life you had always hoped for. Just do small things often and see your dream come to life.

Call to Action

Choose one strategy in the guide and get started on it today. For tailored planning purposes so you can reach your goals, you should speak with a financial adviser.

Frequently Asked Questions

1. What percentage of my income should I strive to save for my financial goals?

The rule of thumb is to save at least 20% of your income for goals including retirement. But the right percentage is going to vary based on your income, expenses and the size and urgency of your specific goals. Try to save what you can afford to.

2. Should I save in the bank rather than invest for my goals?

For investment goals between 6 months and 3 years, when the investor priority is not to lose money and to have liquidity, a bank savings account (or a fixed deposit or FD) may be considered.

For mid- and long-term goals (beyond 3 years), investments in instruments such as mutual funds, NPS and PPF tend to be more beneficial, as they provide the potential to earn higher returns that can surpass inflation.

3. What is the number one barrier people face when it comes to saving money?

It’s typically a mix of no discipline, vague goals and lifestyle creep (spending more as earnings rise). Getting past these will take effort, a well-defined budget, and saving automatically.

4. Can I save for multiple big goals at once, like a house and retirement?.

Yes, absolutely! It is a common recommendation to save for multiple goals at the same time. The trick is to spend the money in smart ways.

For example, allocate a part of your savings to retirement (including through NPS/PPF) and another to your house down payment (a separate SIP, FD, etc.), ensuring that each of the goals has a separate stream of funds.

5. How can I stay motivated to save when things feel so far off?

It is to break down your large goals into bite-sized manageable steps. Monitor your progress regularly and work towards accomplishing small victories. Envision what you want (a photo of your dream house).

Savings should be automatic; you should not have to depend on your daily motivation and remind yourself about your “why”.

Are you neglecting your future without even knowing it? So many of us make money mistakes, and it’s not for lack of good intentions or ideas; it’s for lack of knowing any better. By understanding the “top 10 most common financial mistakes”, you can recognize and work to correct them, thereby creating a more solid financial foundation.

In order to put you on a path to long-term financial health, this article will help highlight those typical pitfalls, explain why they’re so terrible, and—above all—tell you “how to avoid common financial mistakes” and steer clear of them completely.

Part 1: The root of financial mistakes: Recognizing the pain is the first step to blame

Why We Make Financial Mistakes

Financial blunders are caused by a combination of psychological biases, a lack of financial literacy, and unforeseen life events. For example, the need for immediate gratification can also induce wasteful spending. The herd instinct causes people to jump on the bandwagon without doing due diligence. Also, people don’t understand it very well in financial terms.

“Everybody makes mistakes; we need to remember that.” The point is to learn from them and plan not to do them again.

Section 2: Top 10 Most Common Financial Mistakes

1. Not Budgeting (or Underbudgeting)

The Mistake: Most people don’t know where their money is going, and so overspending occurs, and potential savings are lost.

The Solution: Develop a reasonable budget that aligns with approaches like the 50/30/20 rule or zero-based budgeting. Monitor your costs closely and adjust your budget as needed. Learn about the 50/30/20 budgeting rule from NerdWallet

2. Not Establishing an Emergency Fund

The Mistake: People with no financial cushion might resort to high-interest debt in an emergency or sell investments before they should during a downturn.

The Solution: Aim to have 3-6 months’ worth of living costs squirrelled away in a separate, easy-to-access high-interest savings account or short-term fixed deposit.

3. Accumulating High-Interest Debt

The Mistake: If you have carried balances on credit cards, personal loans or quick loans, you may find your wealth evaporating fast, as you fork out high interest payments.

The Solution: Focus on paying down high-interest debt aggressively (with the snowball method or the avalanche approach), instead. Avoid making only minimum payments.

4. Not Starting to Invest Early Enough

The Mistake: putting off tasks or succumbing to fear can result in missing one of the most powerful forces in investing: the power of compounding.

The Solution: Begin investing as soon as you can, even with small amounts. Opt for instruments to invest: Opt for vehicles such as Systematic Investment Plans (SIPs) in mutual funds. For time in the market trumps timing the market, remember?

5. Missing Out the Diversification Factor While Investing

The Mistake: You are taking on a concentrated risk when you invest everything you have in a single type of asset, sector or stock.

The Solution: Diversify your investments across various asset classes (equities, debt, real estate, gold), industries and geographies. You might consider investing in diversified mutual funds or exchange-traded funds.

6. Investing Emotionally

The Mistake: “You start buying when things get high (greed), and you start selling when things get low (fear), and obviously that’s a losing strategy most of the time.”

The Solution: Stay the course with a clearly defined plan. Automate your investments (through SIPs) to cut down on emotions driving decisions. Remember, market volatility is par for the course.

7. Ignoring Retirement Planning

The Mistake: Overlooking the importance of saving adequately for the long term or thinking future income will take care of it all or that it’s “too early” to start saving for retirement, which can result in a future of potential financial insecurity.

The Solution: Save for retirement tenaciously. Make the fullest use of your tax-advantaged accounts, such as NPS (National Pension System) or PPF (Public Provident Fund) in India, or employer-sponsored plans.

8. Neglecting Insurance

The Mistake: Not Accounting for Unforeseen Events: Failing to plan for life’s what-ifs – such as illness, disability or death – can leave dependents financially vulnerable.

The Solution: Secure proper health, life, and disability insurance. Regularly review your policies to make sure there is enough coverage.

9. Failure to Review Financial Plans Periodically

The Mistake: Creating a budget or investing plan and leaving it unchanged for life can result in a stale strategy that does not accommodate changes to life.

The Solution: Set regular financial planning once a year or twice a year. Change budget, investment mix and goals as life requires (i.e., marriage, new job, baby, buying a house).

10. Falling for “Get Rich Quick” Pitfalls

The Mistake: Falling for get-rich-quick-and-easy pitches usually results in big money losses or the discovery of scams.

The Solution: Be sceptical. Recall that true wealth creation is a process, and it does not happen overnight. If something sounds too good to be true, it probably is. Invest only in regulated and well-understood instruments.

Conclusion: Empowering Your Financial Future

In short, the “top 10 most common mistakes” have the potential to do in your financial health. But these trips are inside everyone’s control. Your finances are unique, but the fundamentals of good money management are the same for everyone.

When you can avoid those mistakes and put some smart strategies in place now, you put yourself in a position to grow wealth that lasts and gives you real peace of mind.

Call to Action

Figure out what mistakes you could be making and start adjusting quickly. Perhaps discussing with a CFP could help keep you on track with your financial mindset.

Frequently Asked Questions

1. If I hate budgeting, how can I track my spending effectively?

You don’t have to be super strict in budgeting at first. Begin with the simple act of tracking every rupee you spend for a month or two. For a gradual but consistent strategy, use budgeting apps, a spreadsheet, or pen and paper.

After seeing where your money goes, you can decide what to cut back on and what to reallocate.

2. Should I pay down my home loan or invest more if I have extra money?

That depends on how interest rates on your home loan stack up. If loan interest rates are much higher than what you believe you can actually earn from investments, after taxes, wiping out the loan may be more advantageous.

But if you’re expecting to earn more on your investments, investing starts to make sense. You might consider taking a balance between the two options, especially when it comes to your long-term wealth goals.

3. I’m already in my 40s/50s. Is it too late to fix financial mistakes and create wealth?

It’s never too late! “Compounding is most potent when started early, but even getting started in your 40s and 50s can have a big impact.”

Concentrate on aggressive saving, smart diversification and maximizing retirement contributions (including NPS) to compensate for lost time.

4. How can I determine what insurance I need and prevent under-insurance?

Consider your liability (loans), dependents’ requirements and potential loss of income. The general rule when you’re considering life insurance is 10-15 times your income.

When it comes to health insurance, make sure you’re covered for medical emergencies. Speak to an independent insurance broker for more information on all the options.

5. What’s one habit to establish for long-term financial success?

Consistent saving and investing. More than anything else about the markets, the act of habitually saving and investing a portion of your income, year in and year out, is the greatest indicator of long-term wealth.

Political risk continues to be one of the key issues for the economy, and geopolitical risk hangs over it at a time when India finds itself just over a year away, on July 9, 2025, from a crucial US tariff deadline.

At the same time, a huge global password leak and the Reserve Bank of India’s (RBI) relentless fight against cyber fraud reiterate the need for having strong cybersecurity in the financial system and more financial protection for all.

Impending US Tariff Deadline and Trade Deal Uncertainties

The Urgent present risk management India The media around the world is facing the impending deadline for a new trade deal on 9 July announced by US President Donald Trump. leading to continued trade wars.

Although President Trump tweeted on July 6 that “trade deals are moving along very well” and alerted that the imposition of tariffs is on the way, it is not clear if India makes it to any such definitive agreement. The tariffs – ranging from 10% to 50% – were due to kick in on August 1 and could hurt India’s exports and therefore the rupee.

The continuing talks, notably over US farm products’ access to markets, are tough. India’s inability to nail a fair US trade deal could up the ante on geopolitical risk and bring market volatility.

As a strong testament to the extent of cyber vulnerabilities, a July 7, 2025 report highlighted a large-scale worldwide leak of passwords, estimated at about 16 billion for use on assorted online accounts. That exposes customers to major risks, from social media hacks to potential bank hacks.

A strong government advisory tells people to stop reusing passwords and start enabling multi-factor authentication for all online services. This incident reflects the importance for you and me to take our digital hygiene seriously because our own financial security and security as a community depend on it. For more details on this significant password leak and recommended safety measures, see The CSR Journal’s report.

RBI Proactive Against Financial Fraud

The Reserve Bank of India’s (RBI) fight to cut down on banks for combating financial fraud is not showing any signs of slowing down. The DoT’s Financial Fraud Risk Indicator (FRI) tool is being fed into the systems of banks, and this treasure trove of information is more than any trigger that can be programmed into FRI.

This tech identifies mobile numbers according to whether they belong to the risk of financial fraud and allows banks and UPI platforms to take real-time action to prevent a dubious transaction in the first place.

HDFC Bank, PhonePe, ICICI Bank and Punjab National Bank are already using FRS, and these numbers exhibit the strict regulatory environment of India in fighting cyber-enabled financial crimes, The Economic Times reported.

The Complete Solution for a Digital World of Risk

Beyond immediate threats, holistic risk management is critical for an increasingly digital India. The combination of AI-based early warning systems, zero-trust security models and behavioural analytics is becoming a critical part of financial institutions’ ability to detect and address advanced attacks, such as those that leverage generative AI and deepfakes.

And, while it’s not directly related to today’s news, the larger conversation about preserving household wealth, especially as it pertains to assets such as gold in the face of price volatility, is another component in the background of the financial protection market.

The complex risk management in India in July 2025 is characterized by the interplay of global trade dynamics, sophisticated cyber threats and domestic policy responses.

Financial independence is a journey, not a race. But for those in the early years of How to Supercharge Your Savings in Your 40s and 50s, the decades are a pivotal period – a combination of a final sprint and a graceful victory lap where time remains to build substantial retirement savings and achieve some ambitious goals.

Odds are that you are in your peak earning years, that you have a wealth of experience and perhaps fewer short-term financial obligations than you did when you were younger.

If you’re not sure how to navigate this key saving period, you’ve landed on the right page. This guide will give you practical strategies to increase your savings and enable you to build a strong fortune as you confidently approach your golden years. For an overall perspective on financial planning in your 40s and 50s, see Investopedia’s guide to saving in your 60s.

Why Your 40s and 50s Are Prime Time for Saving

Though sooner is always smarter, there are some special advantages of midlife for improving your financial planning:

1. Peak Earning Potential

For many, their peak earning years are in their 40s and 50s. This leaves you with more money that you can put towards savings.

2. Closer to Retirement

The retirement end-of-the-rainbow is just around the corner, so, there’s no better motivation than that sense of urgency to get your financial plan fixed up.

3. Reduced Early-Life Expenses

For many, some of their largest expenses — like child care or first-home down payments — may be in the rear view mirror, freeing up cash flow.

4. Financial Wisdom

What do you learn after suing and being sued by everyone from your most trusted adviser to your landlord? You pick up a few things that you would have liked to have known 10 to 20 years ago.

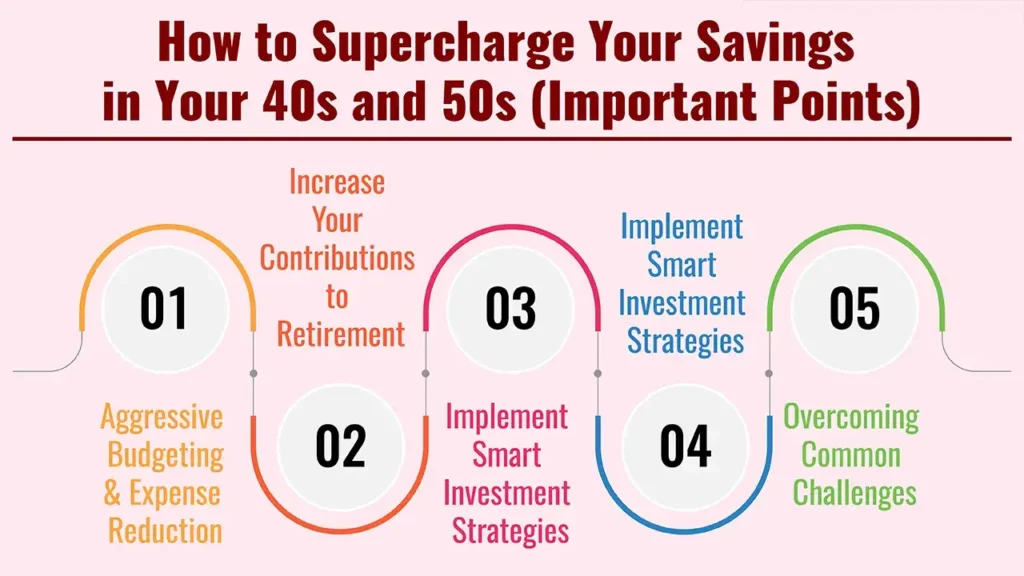

How to Supercharge Your Savings in Your 40s and 50s (Important Points)

It’s time to get strategic. What follows are the best strategies for crushing your savings goals in your 40s and 50s:

1. Aggressive Budgeting & Expense Reduction

Even if you’ve budgeted in the past, a deep dive is in order.

Conduct a Spending Audit: Carefully track all your spending for a month or two. You may be surprised how your money is spent.

Identify and Eliminate Non-Essentials: Consider any recurring subscriptions or unused memberships or any discretionary expenses that you can reduce or cut completely. Small, consistent savings snowball into something significant over time.

Optimize Recurring Bills: Research for lower rates of insurance (home, auto, life), internet, phone plans and utilities.

Reduce High-Interest Debt: Focus on paying back credit card debt, personal loans, or other high-interest debts first. The amount of money saved on interest can then be diverted into savings.

2. Increase Your Contributions to Retirement

It’s debatable, but one of the most important things you can do here.

Max Out Employer-Sponsored Plans: If your employer has a 401(k), 403(b) or other such plan, contribute up to the maximum at which an employer match is available. This is essentially free money.

Utilize Catch-Up Contributions: Someone who is aged 50 or older can usually take advantage of tax laws that also permit higher extra contributions to retirement accounts (such as 401(k) and IRA). Use them to speed up your savings.

Use of a Traditional/Roth IRA or Roth/Traditional Account(s) (ROTH AND/OR IRA): If you’re maxing out your employer plan or don’t have an employer plan, you should be contributing to an I.R.A. or Roth I.R.A., depending on where you’ll be eligible for tax incentives.

Understand and Optimize Pension Plans: If you have a defined benefit pension, know what its payout options are and how it fits with your other savings.

3. Implement Smart Investment Strategies

Your investments should be earning their keep.

Review and Adjust Asset Allocation: As you get near retirement, your ability to prioritize one goal over another changes. And make sure the assets in your portfolio (the mix of stocks, bonds, and so on) are appropriate for your timeline and tolerance. And while you can mitigate risk, just keep in mind that you still have to have growth to fight inflation.

Increase Investment Contributions: Money from raises, bonuses or spending cuts should go directly to your investment accounts.

Diversify Your Portfolio: Diversify money across asset classes, sectors and geographies to reduce risk.

Consider Professional Financial Advice: A certified financial planner can help you develop a personalized investment strategy, maximize your portfolio and handle difficult financial decisions.

Boost Your Income: More money means more to save.

Explore Side Hustles: Put your experience and skills to use on freelancing, consulting or a part-time project.

Negotiate Salary and Promotions: Advocate for yourself at work. Being in your 40s and 50s is valuable.

Monetize Hobbies or Skills: Turn a passion into a source of income.

Consider Rental Income: If you have some extra space, you might be able to rent out a room or property.

4. Optimize Major Expenses

Some of the largest expenses you face may have the potential for great savings.

Mortgage Strategy: Think about putting more money down on your mortgage to own your home that much faster and free up substantial cash flow in retirement. Refinancing at a lower interest rate may also save you money.

Children’s Education Planning: “If you can, try out for selective universities and win scholarships and grants, or look around for a less expensive school, such as a community college. Balance their interests against your own retirement security.

Downsize Your Home: If you find your current residence is larger than you need and there are substantial maintenance costs involved, think about selling and downsizing. And the equity freed up can make quite a difference in your retirement savings.

Healthcare Planning: Outside of insurance, look at Health Savings Accounts (if you can get one), which offer a triple tax whammy (deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses).

5. Overcoming Common Challenges

Hurdles are bound to happen, but you can work through them.

The “Too Late” Mindset: You can never be too deep into improving your financial future. A string of aggressive saving, even just a few years’ worth, can have a significant effect thanks to compounding.

Competing Financial Priorities: Manageing retirement savings alongside other goals (like your kids’ education or caring for ageing parents) takes thoughtful planning and prioritizing. Ensure a balanced message by consulting with the selling agent.

Market Volatility: Avoid letting short-term swings in the market knock you off your long-term course. Stay the course with your diversified investment approach and do not make any emotional decisions.

Conclusion

Your 40s and 50s provide a significant window to reset your financial future. Two other solid vote-getters were small potatoes – paying yourself a portion of everything you earn and squeezing every bit of cost out of a recurring expense.

Get a handle on things, be consistent and get peace of mind from ensuring your retirement is established on a strong foundation – one that will lead to financial freedom and fulfilment.

Frequently Asked Questions

1. What are retirement “catch-up contributions” accounts?

Catch-up contributions refer to extra amounts that people 50 and older can contribute to retirement accounts (such as 401(k)s, 403(b)s and IRAs) beyond the regular annual limits. This is intended to enable older workers to save more for retirement.

2. How much should I be saving each month in my 40s and 50s?

It depends on your income, expenses and retirement goals. Yet a lot of money gurus would advise you to save 15% to 20% or more.

Even if you began saving late or are aiming to retire early during these years. Run a retirement calculator to get a personalized target.

3. Debt repayment versus savings in your 40s and 50s

It really does depend on the nature of the debt. You should probably tackle high-interest debt (such as credit card debt) first, as it is the most corrosive to your financial situation.

Low-interest debt (say, a mortgage) generally comes with advice to take a balanced approach, for instance, paying it down while continuing to save for retirement.

Retirement is one common dream – to put away the daily grind and welcome in a new, free chapter of life. But for most people, the real question is, “How Much Do I Need to Save to Retire?” There is no specific number you should enter; only you can provide the right answer to that deeply personal calculation, based on the kind of lifestyle you hope to lead in the future, your current age, anticipated lifespan and the ever-looming factor of inflation.

This article will help you piece together the retirement so that you can not only gauge how much money you’ll need to build for your golden years but also construct a powerful financial planning for a secure future – no matter where you live.

Knowing How Much Do I Need to Save to Retire?: It’s More Than Just a Number

Only once you’ve seen yourself in your post-retirement life can you determine how much you need.

1. Define Your Retirement Lifestyle

Current Expenses vs. Future Spendings: To compare your current monthly and annual expenditures to how you will retire, begin by recording both sources of data in a list. Now consider how these could change in retirement. Will you travel more? Pursue new hobbies? Or perhaps downsize your home?

Necessity Spending vs. Want Spending: The overall idea is to prioritize your spending between the necessities (housing, food, healthcare, utilities)and the wants (travel, entertaining, luxury products). While some costs may go down (such as commuting), they would also likely rise in some cases—such as healthcare.

Medical Costs: A key, underappreciated issue. Medical expenses the world over are soaring; in such an environment, a sound health corpus or a good cover becomes indispensable. Experts are advising people to set aside a hefty chunk of your retirement treasure chest to be used in medical expenses specifically. For insights into the importance of health insurance in retirement, Acko offers valuable information.

2. Consider Inflation: The Silent Wealth Erosion

Rising prices are a major problem when it comes to planning for the long-term financial stress. What might feel like a comfortable amount today isn’t likely to feel as comfortable 20-30 years from now. Inflation is different in different countries and economic conditions, but it’s something to factor in.

The Impact: Your current spending floor may not be sustainable in 25 years, when your expenses could more than double to over $120,000 a year at a 3% annual inflation rate.

Mitigation: You’ll need to ensure that retirees’ investments grow enough to outpace inflation and protect your buying power.

3. Figure Out When You’ll Retire and How Long You’ll Live

When Do You Plan to Retire? The younger you retire, the more years you will have to cover your expenses during retirement, and hence, would need a higher corpus. Some are targeting early retirement in their 40s or 50s, while others hope to work until their late 60s or even longer.

How Long Will You Live? Life expectancy is increasing all around the world as health care and living conditions get better. It is wise to assume a retirement of at least 25-30 years, if not longer, to avoid outliving your assets.

How to compute your retirement corpus? Practical methods.

And as good as online retirement calculators are, knowing how to calculate retirement yourself is important.

Exponentials, the “25x Rule” (and its Variations)

A common rule of thumb is to aim to have saved 25 times your projected first year’s retirement expenses. For instance, if you want to spend $60,000 a year in retirement (in current dollars), then you would need $1.5 million.

This rule presupposes a somewhat stable withdrawal rate (generally estimated to be around 4%, although it can fluctuate depending on market conditions and personal risk tolerance).

A More Comprehensive Approach:

Here is a step-by-step approach which also addresses the financial realties:

1. Calculate Your Retirement’s First-Year Spending Needs (Inflation Adjusted):

Take your current annual expenses. Then forecast that number forward to your retirement year, with an inflation rate plugged in (3%, say). Example: Annual expense at present = 50,000 * (1 + 0.03) ^ 25 ≈ $104,680.

2. Determine Your Total Retirement Corpus:

And here is where a retirement calculator can be an enormously useful tool. It will consider your annual expenses in the future, how long you expect to live in retirement and what rate of return you expect on your investments during retirement.

Formula (simplified):

Corpus Required = (Future Annual Expenses / (Expected Return Rate in Retirement – Inflation Rate)) * [Factor of life span]

Many of the financial institutions from around the world that we have compared have an online calculator that will assist you with this hard-to-calculate figure, which will consider elements such as:

Current age

Retirement age

Life expectancy

Current monthly expenses

Expected inflation rate

Expected pre-retirement investment return

Expected post-retirement investment return

Current retirement savings

Any anticipated pension income (social security, company pensions, etc.)

Ballpark Figures (Highly Variable):

Although it’s very much a personal choice, rule-of-thumb figures for a comfortable retirement tend to range from $1 million to $5 million (or more). A $40,000–$60,000 lifestyle could suffice for a simple, comfortable existence. This comes from a corpus of $1 million – $1.5 million over 25-30 years. For a large city or a more extravagant lifestyle, this amount could be doubled or tripled.

How to build your Retirement Corpus

With the target corpus in mind, it is on to setting up a strong savings and investment plan next.

1. Start Early, Save Consistently

It’s compounding that is your best friend. The sooner you start, the less you have to save each month to hit your target. And even relatively modest routine investments can grow to a significant sum over decades.

2. Automate Your Savings

Automate contributions to your retirement-themed investment accounts. What people don’t see, they don’t think about, and that can be a great motivator to save more.

3. Diversify Your Investments

Avoid putting all of your eggs in one basket. A balanced portfolio typically includes:

Equities: For long-term growth and returns that beat inflation (for example, diversified stock funds, index funds, ETFs).

Fixed Income: Stick to these easier for stability and less for risk, especially the closer you get to expecting retirement (bonds, government securities, certificates of deposit).

Real Estate: Has the potential for rental income or capital appreciation.

Other investment options: (e.g., commodities such as gold) can be a way to hedge against inflation and economic instability.

4. Leverage Tax-Advantaged Accounts

Research tax-advantaged retirement plans in your country (the United States), such as employer-sponsored plans (401(k), 403(b), 457, and pensions) or individual retirement accounts (IRAs, Roth IRAs, and RRSPs in Canada).

5. Prioritize and Review

Retirement planning is not a one-shot deal. Revisit your plan on a regular basis (at least once a year) and make necessary updates due to changes in income, expenses, inflation or the performance of the market.

6. Consider Professional Advice

With local CFPs, you get that personal touch to set up your tailor-made retirement plan and wade through the murky world of investments while getting clarity on tax rules in your area.

Conclusion

Retirement planning can sound intimidating, but with a few easy steps and a head start – don’t delay – you could have a bright and secure future. Because remember, it’s not just about having as much as you can in your account.

It’s about being able to finally live the dream retirement you’ve always imagined. Take action today, decide what you want out of life, and allow the magic of regular saving and smart investing to move you closer to your goals.

Frequently Asked Questions

1. What is a reasonable corpus to have at retirement?

It’s complicated and depends in large part on your lifestyle and where you live, but in simple terms, a realistic average “corpus” you’ll need for a comfortable retirement might be anywhere from $1M to $5M+ in terms of income associated with inflation and a long retirement.

2. Is the 4% rule a good rule of thumb for retirement withdrawals?

There’s that ol’ 4% rule (taking half your portfolio in the year you retire and then adjusting for inflation) that may apply somewhat differently.

Its efficiency may be affected by factors such as how the market is performing, the level of inflation, and individual risk appetites.

Some financial planners recommend a more conservative or aggressive withdrawal approach.

How much should I save on a monthly basis for retirement?

The monthly savings amount would be a function of your current age, when you would like to retire, expected income need post-retirement and the target corpus. Online retirement calculators can provide an exact number for how much you need to invest each month.

As a rule, the sooner you begin saving, the smaller the percentage of your income you’ll need to save (say 10-15%); the longer you wait, the more you’ll need to save (20-30%, or more).

4. Do I need to pay off all my debt before I can begin investing?

Ideally, yes. It can also keep your post-retirement expenses lower and make you feel even more financially secure going into retirement if you are debt-free, especially with high levels of debt such as a mortgage. That’s one way to keep your retirement money going longer.

5. Just how important is retiree health insurance?

Extremely important. Retirees are also facing significant health costs globally. That’s why its important to have good all-around health insurance and a separate medical fund (outside of your FRS) to protect your retirement savings from health-related expenses not covered by insurance.

As it prepares for a US tariff deadline looming for India on July 9, it is at a crossroads as crucial trade talks with the United States take a crucial turn. The result of these discussions will have significant importance for the stability of the rupee and the overall external finances of the country and are therefore an important focus for risk mitigation in India in the days ahead.

Crucial US Tariff Deadline Approaching

As of July 4, 2025, India and the US are in the throes of an extremely intense dialogue to seal a trade deal before US President Donald Trump’s July 9 tariff deadline.

The inability to reach a sensible deal, or visible progress to that effect, could prove to be a huge strain on the INR and the external balance of the country. This is also one of the single greatest geopolitical risks being watched by the markets.

Most expect a positive result, given the mutual economic and geopolitical interests at stake, but it’s hard to have confidence in that. And that’s a major market risk.

One of the contentious points of negotiations is India’s access to the market for genetically modified (GM) crops. A new option being considered is a “self-certification” mechanism for US exporters who will have to meet India’s GM-free mandate but with a sense of comfort on food safety.

The writings also pertain to India’s food safety protocols under the ‘certification’ and ‘registration’ of certain ‘high-risk’ imports such as dairy, meat, poultry, fish and infant foods.

Improving National Security by Buying Locally

Also, as a boost to the national financial security and to ensure greater self-reliance in the country, the Defence Acquisition Council (DAC), chaired by Raksha Mantri Rajnath Singh, here today accorded approval for capital acquisition proposals valued at over 1.05 lakh crore on 03 Jul 2025.

All these acquisitions are under the ‘Buy (Indian-IDDM)’ category, which prioritises indigenisation of design, development and manufacturing. This policy move is in line with the government’s thrust on defence sector self-reliance.

These cleared purchases would contain vital things like Armoured Recovery Vehicles, Electronic Warfare Systems, and Integrated Common Inventory Management Systems for the tri-services besides surface-to-air missiles.

For the Navy, the acquisitions include moored mines, mine countermeasure vessels, super rapid gun mounts and submersible autonomous vehicles.

These indigenised defence procurement plans, once executed, will improve the mobility, air defence and logistical capabilities of the Armed Forces on the one hand and, on the other, give a significant fillip to the country’s indigenous defence manufacturing environment. You can find the official press release from the Press Information Bureau (PIB) regarding these approvals.

Rupee Performance and External Resilience

The Indian rupee Strong rupee The Indian rupee opened flat against the US dollar on June 30, 2025, at ₹85.48, having registered its best weekly gain since January 2023.

This stability was largely supported by tumbling global crude prices and détente in West Asian geopolitics. India stands to gain, with lower oil prices helping to cut its import bill and support the current account, key to external finances in India.

Active management of currency volatility by the RBI, including buying dollars at key levels, also helps maintain order in the markets and ensures that there are enough reserves for the pots of the financial protection that India has erected for itself against external shocks.

A combination of international trade chop and change, strong domestic defence and central bank initiatives exemplifies the multi-dimensional nature of India’s risk management in times of global and home-brewed challenges.

July 2025: It is an important month for personal finance in India, as it announces an extension date for ITR Filing Deadline Confirmed 2025 and various changes that can affect daily financial transactions.

While taxpayers are paying attention to being compliant, they should also get prepared for increasing ATM charges and new guidelines for Tatkal train bookings by taking proactive steps towards money management.

ITR Filing Extended Date for Salaried Employees

In a sigh of relief for the salaried class, the Income Tax Department has officially announced that the last date for filing ITR 2025 for the financial year 2024-25 (assessment year 2025-26) will be extended from July 31 to September 15, 2025.

This extension, news of which was informed on July 3, would help taxpayers in getting more time for accurate compliance as certain ITR forms (like ITR-2 and ITR-3) are being made more user-friendly, which required more time, for which the last date was being extended.

Taxpayers can now utilise this additional time for filing returns to compile details like borrowings, capital gains and other investment income during the extended period. For an official press release regarding the ITR filing extension, refer to the Press Information Bureau (PIB).

How Increasing ATM & Bank Fees are Affecting Everyone

ATM finders: can be used for other banks as well. Some banks, such as Axis Bank and ICICI Bank, have revised their ATM transaction charges from July 1, 2025. At Axis Bank, the charge on such transactions above the free limit has been hiked from ₹21 to ₹23 a transaction for a gamut of accounts – savings, NRI and so on.

ICICI Bank is also revising service fees on ATM transactions, cash deposits and withdrawals and IMPS money transfers. The rate revision due to higher operating expenses will apply to customers in metro and non-metro markets.

That’s why it’s important for them to review these changes so they don’t get saddled with surprises and so they can tweak their budgeting strategies and transaction habits accordingly to better manage their personal finances.

Tatkal Train Rules Changed: Other things to know

In what is another layer of complication to regular financial and travel planning, new guidelines for Tatkal train ticket booking will be effective from July 15, 2025. Wait no more! For from this very date, all online Tatkal ticket transactions will need to be Aadhaar-based OTP authenticated!

The same is intended to prevent false bookings and improve the security of the booking system. The masses have to link and validate in the coming days for a seamless experience while keeping security in place and adding yet another layer of protection to their daily digital transactions.

Proactive Financial Planning is Key

Apart from these immediate switches, financial planning-related challenges in India are constantly changing. But with the EPFO increasing the auto-settlement limit for advance claims from ₹1 lakh to ₹5 lakh (certain categories of withdrawals in three days for different types of needs) and little better to do with savings at this juncture, the need for caution, in the larger interest of the economy, stands reinforced.

Experts also continue to caution against holding large amounts of cash in low-interest savings accounts that don’t even keep pace with inflation and recommend other high-yield investment options. This personal finance news in India for July 2025 tells us that the need of the hour is that we should all stay informed, agile and proactive in managing our personal finances if we don’t want to be hurt financially when it all unfolds in the years to come!

The magazine highlighted India’s economic resilience, quoting a healthy 6.4-6.7% GDP growth forecast for the Indian economy by the CII Projects Strong GDP Growth Amidst RBI Rate Cut; India’s Economic Resilience in July 2025

This positive India economic outlook for 2025 is supported by robust domestic demand and recent proactive steps taken by the Reserve Bank of India (RBI).

Driving Factors for Economic Growth

Speaking at a press conference on July 3, 2025, CII President Rajiv Memani said despite rising global economic and political turmoil, India continues to shine as one of the “bright spots”. Key reasons for this optimistic sentiment are positive monsoon forecasts (key for farm output) and an increase in liquidity in the financial system. For more details on CII’s economic outlook, you can refer to the Economic Times’ report.

Big Role of RBI monetary policy The RBI has significantly played the role after it reduced the repo rate by 50 basis points to 5.50% at the June 2025 meeting and a 100 basis point reduction in the Cash Reserve Ratio, opening liquidity of over ₹2 lakh crore for the banking system.

These acts are designed to increase the country’s credit growth and encourage economic activity, which is important Indian economy news.

Inflation and Policy Stance

RBI’s decision to lower rates was spurred by a sharp easing of inflation, with the CPI inflation dropping to 3.16 per cent in April 2025, its lowest since July 2019. The policy bias has transitioned from an ‘accommodative’ bias to a ‘neutral’ stance, implying a neutral outlook and a data-dependent approach to future rate moves.

Inflation expectation for FY26 has been slashed to 3.7%, giving confidence in stable and limited inflation. Although headline inflation has moderated, observers will keep a close eye on whether core inflation (which excludes food and fuel) does the same, as the two have historically tended to converge.

Focus on Reforms and Competitiveness

CII has also announced its theme for the year 2025-26, “Accelerating Competitiveness: Globalisation, Inclusivity, Sustainability, Trust”, with suggestions for strategic economic reforms. These are ways to increase manufacturing, exploit technology and AI (including the proposal for a National AI Authority), accelerate sustainable processes and improve livelihoods.

Emphasis is laid on enhancing India’s competitiveness through global engagement and inclusive growth, which is necessary to achieve sustainable economic stability. Loans for MSMEs needed to be scaled up and R&D supported across industries as well, according to CII.

Fiscal Discipline and External Stability

We view the government’s decision to stick to the 4.4% of GDP fiscal deficit target for FY26 (Apr-Mar) and the shift to medium-term debt targeting from FY27 and beyond as positive for fiscal discipline.

Externally, though FDI and FPI could continue to be sluggish on account of global vagaries, the strong quantum of India’s foreign reserves, at around $691.5 billion in June, is comforting and provides sufficient cover against external volatility (it covers over 11 months of imports), thereby ensuring a stable BOP.

Together, these factors further confirm the optimistic market views July 2025 for India’s economic odyssey.