The world of tax and finance is changing at a breakneck pace, and the world of tax advisory services is no exception — shaped by AI, automation, cloud and other digital trends. By 2025, these advancements are no longer ‘nice-to-haves’ but rather critical for tax professionals to remain competitive, work efficiently, and better serve their clients.

For CAs and tax agents, to become genuinely tech savvy will require a move away from time-wasteful manual activities to automated and intelligent systems that take the complexity out of compliance, improve the accuracy of their work and give them the ability to serve clients strategically.

This article discusses what are going to be the most significant trends defining the future of tax advisory, the regional landscape taking shape, key challenges and some strategic recommendations for thriving in this new reality.

AI and Automation: Tax Transformation with the power of AI and Automation

At the core of the tax advisory revolution is artificial intelligence. The ability of AI to process large amounts of data at a high speed and to find the nuggets of valuable information is transforming the way that tax professionals work. Automated bots are starting to take over monotonous, day-to-day tasks, such as data entry, document examination, tax computation and compliance verification.

Tax software powered by AI can even pinpoint disparities or inconsistencies with surprising accuracy, significantly minimising the chances of an audit or fines. This automation allows tax professionals to concentrate on value-added services such as tax advice customised to a client and strategic consulting. Machine learning models also improve predictive analytics, allowing companies to predict tax exposures and find new tax savings in client financial data.

For one, natural language processing (NLP) supports AI tools in understanding complex tax laws and regulations, in turn, responding to queries and adjusting to real-time changes in the regulatory environment. This increases not only the accuracy of compliance but also speed – which are both critical factors in today’s “tax is the new sexy” world.

RPA enables the automation of administrative workflows such as tax form population, income tax filing, and compliance reporting. Bots never stop; they never make a mistake. If you pay them once, they keep going – all day, every day – for free. These automation features are anticipated to save tax professionals hours each week and provide more time to engage with clients strategically.

Cloud Computing and Digital Infrastructure

Today, the cloud is essential in up-to-date tax advice. By leveraging the cloud, tax professionals can connect to data, tools and software from anywhere around the world, providing flexibility for modern working patterns and ease of connection with clients wherever they are.

Cloud computing can serve the scaling need so that companies can handle large volumes of data and customers without shelling out huge investments for infrastructure. Additionally, cloud providers employ among the finest security measures to prevent tax information breaches and cyber attacks.

This enhanced accessibility and security further advance client service and enable increased transparency and real-time visibility into the tax process. By 2025, next-generation tax advisory firms will take advantage of the cloud, performing complex tax scenarios and meeting compliance requirements with increased confidence.

BlockChain in RegTech: elevating transparency and conformity

Blockchain is emerging as a way to make tax administration more transparent and trustworthy. Requiring no trust among parties, the technology’s unchangeable ledger records transactions safely, guards against identity theft, and makes it easier to prevent fraud and establish clear customer audit trails. On blockchain, smart contracts can be used to automate tax calculations and payments, such as faster VAT refunds and cross-border tax compliance.

Compliance monitoring is also being automated by regulatory technology (RegTech). These smart solutions monitor changes in tax laws around the world and alert firms to relevant changes so they can adapt and stay compliant. They also simplify the reporting and risk management process by rolling up the compliance reporting and allowing for the early identification of any issues.

The future of effective, digital-first tax advice – transparent, reliable and able to cater to the emerging demands of the millennial market – will be based on blockchain and RegTech.

Market Trends and Regional Insights

Post-2025 there appears to be an increasing demand beyond just tax filing for advisory services. About 83% of taxpayers now want practitioners to provide them with strategic tax advice, so it is indeed turning to value-added services. Tax execs are reacting by broadening their services to include such things as business consulting, tax planning and risk advisory.

North America is a frontrunner in tax technology; under tax technology, global usage is that. Domain: Strong, mature infrastructure and regulatory environments lead to early adoption of AI, automation, and cloud solutions.

Asia-Pacific is the fastest-growing market for tax technology due to the presence of new reforms and digitalisation investment. Rapid adoption of insurtech and cloud computing suggests the region is fertile territory for insurers looking to innovate and win over growing client bases.

Adoption: there is a consistent and strong investment in compliance and cooperation across borders within Europe, where data privacy regulations are strong. Sophisticated EU and European companies will focus on complex tax regimes and will prefer advanced compliance management systems.

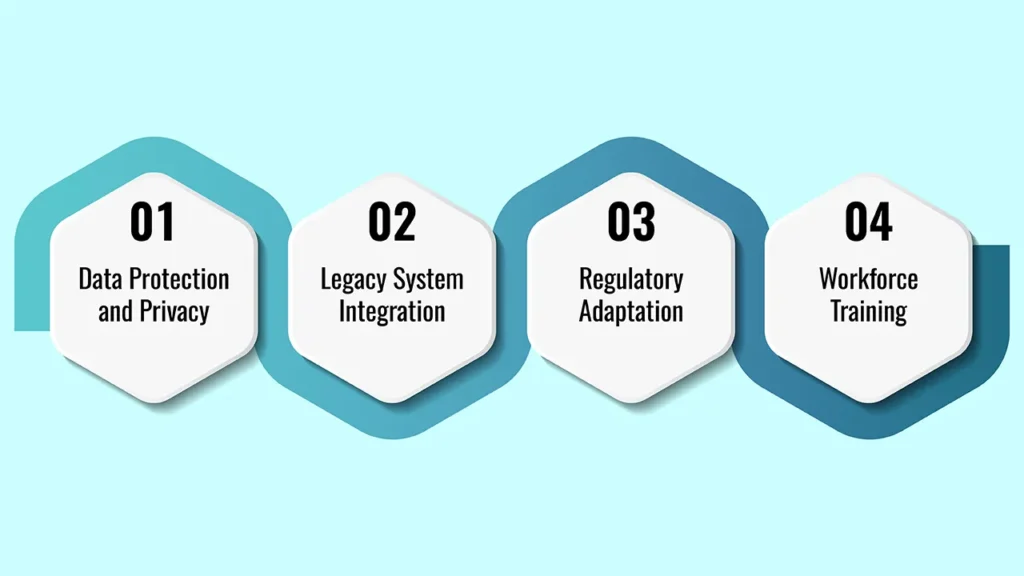

Challenges in Adoption

Despite the encouraging benefits, the introduction of AI and automation to the context of tax advisory is not without its hurdles:

- Data Protection and Privacy: tax data is extremely sensitive and requires state-of-the-art security measures to protect against unauthorised disclosure.

- Legacy System Integration: Many of a company’s legacy systems were not designed for easy integration with newer AI-based or cloud-based systems and result in substantial costs associated with expensive replacements.

- Regulatory Adaptation: The change in tax laws is often continuous, and the AI and digital tools must be ever-updating with these changes.

- Workforce Training: Employees need upskilling to align with technology-driven processes and to effectively and responsibly apply AI.

Overcoming these challenges is entirely essential for the optimum advantage of digital transformation in tax advice services.

Human and Tech Synergy: Skills and Strategy

Technology augments, but does not substitute for, the profound knowledge our tax professionals offer. The future, in 2025 and beyond, will look like a combination of mixed skills, where advisors will have deep technical knowledge combined with AI tooling capability and data analytics.

This also requires that firms invest in long-term (ongoing) training to enable staff to make use of technology and provide personalised service. Strategic use of AI and automation empowers firms to ease the transition from hourly billing to value-based pricing methods that both increase profitability and ensure client satisfaction.

Valuable partnerships with tech vendors and regulatory specialists keep firms ahead of the curve and share the risks and rewards that come with new tech deployments.

Future Outlook and Recommendations

The future of the tax consultancy space belongs to firms that will marry strong human expertise with technology, AI, automation, cloud, and blockchain. To thrive in 2025:

- Focus on AI and automation to enhance process efficiency and effectiveness.”

- Use the cloud for scaling, security, and remote accessibility.

- Utilise blockchain and RegTech solutions for greater transparency and compliance.

- Commit to training staff and managing change to bridge cultural and skills divides.

- Take on value-based pricing via complete service offerings.

- Take advisory services away from compliance, and provide advice that is strategic and predictive.

- Seek out alliances that leverage technology and domain knowledge assets.

- These are the types of sales and marketing approaches that will set the tax advisory firms apart in the years to come.

Frequently Asked Questions

1. How will AI change tax consulting in 2025?

Predictive analytics from AI will empower tax professionals to provide tailored advice on tax planning and risk mitigation, particularly around strategic issues, taking them on an increased advisory role over and above compliance.

2. How does the cloud impact contemporary tax advisory?

It also gives companies the ability to grow without major IT investments yet have the peace of mind that their data is safe and secure with disaster recovery in mind.