Apple today debuted a substantial addition to their financial services products, with the launch of a high-yield savings account available to iPhone users offering a 6.0% Annual Percentage Yield (APY).

The push is expected to increase the competition in the digital banking arena and will include additional financial services offered alongside the existing portfolio of products within the Apple ecosystem.

A Bold Step for High-Yield Savings

The new savings offering, which users can access right from the Wallet app on their iPhone when they use their Apple Card, offers an APY that far outstrips the current market national average, and which is also among the best APYs available to U.S. customers currently.

Most high-yield accounts right now have APYs from 4.0% to 5.0%, and Apple’s 6.0% APY is designed to draw a significant portion of its massive clientele to the bank. The service – with funds backed by Goldman Sachs Bank USA and insured by the Federal Deposit Insurance Corporation up to the maximum allowed by law of $250,000 – has many pluses:

Seamless Experience: Users can open and manage a savings account directly from the Wallet app, alongside their Apple Card. This deep level of integration is part of Apple’s overall strategy is to keep us inside its digital universe.

Automatic Daily Cash Redemption: Apple Card customers will have the new option to automatically redeem their Daily Cash as a statement credit. These rewards can add up over time for big savings on Apple products or that dream vacation everyone is looking forward to.

No Frills, No Minimums: The account has no monthly fees, no minimum deposit to open, and no minimum balance required to earn the APY offered, putting interest within reach for large numbers of consumers.

Simple deposits: Savings can be deposited to the savings account and removed from the savings account back to the linked bank account or Apple Cash balance.

Intensifying Competition in Fintech

The introduction is a serious escalation of Apple’s push into financial services and could be a challenge to traditional banks and other fintech companies. With its massive user base and integrated hardware-software ecosystem, Apple is poised to be a powerful force in consumer banking.

Apple initially rolled out a high-yield savings account with a 4.15% APY in April 2023, but the decision to aggressively raise the APY to the headline-grabbing 6.0% now could be a strategic statement to capture the market quickly, or a reflection on a change in economic outlook and interest rates.

The decision comes as high-yield savings accounts are in transition, with rates having been high across the board because of interest rate increases by the Federal Reserve in recent years. However, recent economic indicators, like the Bank of England’s surprise rate cut, point to the potential for changes to the world’s monetary policy down the line, which in the context of the current environment makes Apple’s 6.0% APY quite appealing.

For millions of iPhone users, the new high-yield savings account has the potential to offer a seamless way to get more from their savings in the one device they carry everywhere they go — and to upend what people have come to expect from their personal finances.

The Bank of England (BoE) rattled the global currency market today, July 17, 2025, when it shocked the world with an unanticipated 25-basis point reduction in its benchmark interest rate to 4.00%.

The move, which did not take place at the Monetary Policy Committee’s (MPC) typical monthly get-together, caused the pound to fall sharply and plunge to the lowest levels in 2021.

The Bank of England’s unexpected rate cuts have sent the pound crashing to its lowest levels since 2021. Discover the implications for the economy.

The Surprise Decision and Market Response

BoE’s MPC had been widely expected to keep rates unchanged at its next scheduled meeting on August 7, with market consensus suggesting a first cut in late 2025 or early 2026 – especially after the release of UK inflation figures in July, which showed an unexpected rise to 3.6% in June.

But the bank attributed its unscheduled move to growing concerns over the UK’s economic prospects in general and the effect of global trade tensions and slowing growth in particular.

“In light of the increasing downside risks to the global and U.K. outlooks and with domestic inflationary pressures remaining subdued, the Committee agreed that it was appropriate to take some action to support demand in the U.K. economy and to ensure that the recent fall in inflation did not undershoot the 2 per cent medium-term inflation target,” the BoE said in a brief statement. This is an even more pessimistic tone than had been previously communicated.

In response, the pound sterling (GBP) tumbled versus all of its peers in the spot market. Versus the dollar, GBP/USD lost ground rapidly, closer to its 2021 Alice lows and the 1.28-1.29 level. The pound was hit hard against the euro. This drop is a clear reflection of investor concern over the unforeseen move, expressing those fears over the UK’s economic health and a greater likelihood of additional monetary easing.

Why the Early Cut?

The BoE’s decision, which followed the Fed’s stance by a day, was said to be driven by domestic considerations such as growth and employment, yet market observers are searching for the actual catalyst for such an off-cycle move. Possible factors include:

Fading Growth Outlook: While some resilience became apparent, the latest data would have still suggested that a sharper contraction in activity or stagnation was taking place, with recent US tariffs on UK trade adding to the pressure.

Rising Forces in Trade Wars: We might add the incipient trading war that would evolve between the US and most of its key trading partners, which could have already exacerbated a downside threat to UK exports and economic stability that seemed likely to have been modelled before.

Breaking Away From Other Central Banks: The European Central Bank (ECB) has been lowering rates, while the Federal Reserve has held steady. The BoE might be getting ahead of the curve to avoid a firmer pound from undermining UK exports.

Consumer Spending Worries: The recent publication of inflation data, though higher, could have hidden weaker consumer confidence or spending power – something the BoE tried to tackle.

Implications for the UK Economy

The surprise rate cut is a double-edged sword for the UK economy. On one hand, it may offer a long overdue boost to borrowing and investment as a way of helping support businesses and homeowners who have been clobbered by high mortgage rates.

However, with the collapsing pound, imports will become dearer, which may prompt a rise in inflation and consumer purchasing power getting hit.

The cut brings immediate respite for homeowners on a variable-rate mortgage, but savers are set to experience a further decline in returns. Import-dependent businesses will face higher costs, and exporters might benefit from a currency that is weaker.

The BoE’s shock is a turning point in its monetary policy, showing up with solutions to counter economic headwinds. The BoE’s next MPC meeting is scheduled for August 7, and analysts will then be looking for more detailed forecasts and possible hints at the central bank’s forward guidance in light of this week’s speech. Sources

Private equity titans KKR & Co. and Blackstone Inc. are among the buyout firms said to be part of a group offering a massive $90 billion to buy the U.S. operations of viral video-sharing app TikTok from its Chinese parent company, ByteDance Ltd., in a deal that could shake up global social media, according to various media reports.

That new push for a sale is occurring as TikTok is confronting a potential ban in the United States over national security concerns.

High-Risk Gamble Under Current Geopolitical Conditions

The stratospheric valuation is further evidence of the extraordinary perceived worth of TikTok’s U.S. business, with its more than 170 million American users and over $12 billion in ad sales in 2024. The offer is being spearheaded by a group that also involves Oracle Corp.

And venture-capital firm Andreessen Horowitz, according to people with knowledge of the discussions. This isn’t the first time the group has tried to buy up TikTok’s U.S. operations. One such transaction, which would have given new outside investors half of TikTok’s US business and reduced ByteDance’s holding to below 20%, reportedly fell through in April when China refused to sign off its approval (paywall), after the US had applied a previous round of tariffs.

The current acquisition negotiations are being held under intense pressure. A law signed by then-President Joe Biden in the past year required ByteDance to sell TikTok’s U.S. operations by the deadline of January 19, 2025, or be forced to shut it down.

Though the U.S. Supreme Court has upheld the law, U.S. President Donald Trump’s administration has continued to delay the deadline (most recently to mid-September), hoping to broker a deal that would “save TikTok” for Americans.

Oracle’s Role and Data Security

One of the linchpins of the proposed deal is for Oracle Corp. to have a minority stake and provide assurances on the security of user data. Oracle already supplies the cloud infrastructure for TikTok in the U.S. under previous agreements, which were adopted months ago in an effort to allay concerns that Chinese authorities could obtain access to information from the app.

The new deal would probably entrench and expand Oracle’s oversight of U.S. user data and software updates to meet American national security needs.

Challenges and Chinese Approval

EVEN as it is, any deal is heavily conditioned – conditional on the approval of various players, including the Chinese government and its president, Xi Jinping, who must now struggle with the mixed feelings of dealing with an American president who demonstrates enough unpredictability to be dangerous.

China has repeated its “principled position” on TikTok matters, saying business conduct, including mergers and acquisitions, must follow market rules and respect international laws and Chinese laws. Beijing has previously signalled resistance to a forced sale of TikTok, especially of its core algorithm, which it has called a national asset.

The $90 billion number is a hefty premium over earlier valuations, which had the value of TikTok’s United States business ranging from $20 billion to $150 billion, depending on what terms and technology were involved.

Representatives for Oracle, Andreessen Horowitz, ByteDance and TikTok either did not respond to requests for comment or declined to comment, and neither KKR nor Blackstone have publicly commented on the matter, but during an interview last week, President Trump said he would be announcing the group of buyers “in about two weeks’ time”.

The weeks ahead will be crucial as the two sides try to unwind geopolitical complexities and navigate regulatory impediments to consummate a deal that could set the future of one of the world’s most influential social media platforms in the U.S. market.

You think you need a huge down payment and lots of cash to enter the world of real estate? Think again! The prospect of coming onto the property chain with a small amount of cash has never been more realistic.

This contribution will guide you through a number of tactics and concepts of low-capital investing so that you can take the first steps to create your real estate portfolio.

Ready to invest in real estate but short on funds? Explore our guide on starting with low capital and unlock the secrets to successful property investment.

Real Estate Landscape in the Age of Low Capital Investment

Dispelling Myths

A lot of people think that only rich people get into real estate, but creative financing and different investment vehicles make it so anyone can.

Why It’s Possible

There are new models, products, and investment structures that can drive down the cash required to invest in real estate up front and finally bring real estate investing within reach.

Understanding “Low Capital”

In this context, “low capital” might mean less than ₹5-10 lakhs, or even a fraction of that, relative to typical direct buys.

Important Priorities

If you have less cash to work with, you need to have your ducks in a row, a good credit score (for financing options), an emergency fund and be open to learning about the market.

Strategy 1: Passive and Indirect Investments in Real Estate

These are ways to invest in real estate without buying property with outright ownership and are ways with little upfront capital.

1. Real Estate Investment Trusts (REITs)

How They Work:REITs are businesses that own, operate or finance income-generating real estate. They are traded on exchanges, just like stocks, and you can buy shares in a portfolio of commercial or residential real estate.

Benefits for Those with Little Capital: High liquidity (able to sell shares), professional management of properties, and diversification between real estate sectors or geographies with a not-so-high investment amount (you can buy as little as one share).

Things to note: You can’t control the physical specs, and the performance of the assets might be affected by stock market movements.

2. Real Estate Mutual Funds and Exchange-Traded Funds (ETFs)

How They Work: These funds invest mainly in shares of real estate companies and REITs, creating a diversified basket of real estate-related securities.

Advantages for Small Capital: These provide IMMEDIATE diversification with very small investment OPERATE under Professional fund managers. Easy to enter and exit.

Considerations: You are indirectly exposed, with your position hinging on the fortunes of the underlying companies rather than the value of property merely. They also are subject to management fees.

3. Real Estate Crowdfunding & Fractional Ownership Platforms

How They Work: Investors pool small amounts of cash to collectively buy shares in larger properties or development projects (such as commercial buildings or holiday homes). You own a “fraction” of a bigger thing.

Adapted to Small Budget: They allow you to invest in high-value properties you cannot afford, provide diversification to different projects, and many times they generate you regular money from rents. Some platforms may also have entry points as low as ₹10,000 to ₹1 lakh.

Benefits: Investments on these platforms can be illiquid, while returns depend on the success of the project and platform fees. Platform and project due diligence is important.

Strategy 2: Strategic Funding is Done-for-Direct

These are methods where you buy the property outright, but you utilise some sort of financing option to minimise your upfront investment.

1. House Hacking (Owner-Occupied Multi-Unit)

How It Works: Buy a multi-unit property (duplex, triplex, or single-family with extra rooms) and live in one unit/room while renting out the others.

Low Capital Good: You’ll often be able to get owner-occupant loans with low down payments and better interest rates than you’d likely qualify for on investment property loans. And the rent from other units may cover much, or even all, of your mortgage, which means it’s possible to live for next to nothing.

Considerations: It requires living on the property; thus, you become your tenants’ landlord. It also involves mindful selection of a tenant.

2. Low Down Payment Loan Programs (FHA, VA, Government Loans)

How It Works: Though it’s not as commonly available for pure investment properties in India, one might find government housing schemes or some lender programmes that have lower down payment options, especially for first-time home buyers or if you are buying certain types of property (e.g., affordable houses). Look for plans such as Pradhan Mantri Awas Yojana (PMAY) if you are eligible.

Benefits for Low Capital: These initiatives lower the amount of upfront cash, which can help make homeownership (and possibly house hacking) more achievable.

Benefits: These tend to have strict qualification requirements, and some require mortgage insurance, typically only for owner-occupied residences. Research specific lender offerings.

3. Seller Financing (Owner Financing)

How It Works: In lieu of taking a loan out from a bank, the property seller agrees to function as the lender (typically with a lower down payment and interest rate agreed upon between the two of you).

Perks for Low Capital: It’s an escape from bank standards, and it can require a smaller down payment with more relaxed terms based on your own situation.

Drawbacks: You have to find a motivated seller who is willing to provide this, and interest rates could be higher than those for bank loans. Legal counsel is essential.

These are a little more hands-on, but they provide a high payback for a relatively low investment if applied well.

1. BRRRR (Buy, Rehab, Rent, Refinance, Repeat)

How It Works: You purchase an income-producing property below its value, rehab it to raise its worth, rent it out to generate income, refinance it to pocket your original investment (and ideally a little more), then start the cycle anew.

Advantages for Small Capital: Done rightly, you are able to reinvest the very first capital and grow another Arabic copy from it. The refi step effectively transforms short-term capital into long-term equity.

Considerations: This is a hands-on strategy that would have some project management skills in place – solid rehab cost estimating and a heavy ability to finance short-term for the purchase and rehab.

2. Rent-to-Own / Lease Options

How It Works: You rent a property with the right to purchase it at a predetermined price later. Some of your rent may be credited toward the down payment.

Benefits for Low Capital: Can get control of property with low upfront option fees, can see if property/neighbourhood is a fit for you before purchasing, and can build your equity over time.

Considerations: The option fee is almost always nonrefundable, and you need a contract, written generally, that holds up in court. Fine, lenders are banking on market conditions to change and for the pre-agreed price to become less attractive.

Essential Steps Before You Invest (Regardless of Capital)

You Must Learn Relentlessly: Get stuck into books, webinars, podcasts, other investors; just learn stuff!

Grow Your Network: Meet and build relationships with real estate agents, lenders, investors and contractors. Your network is your net worth.

Know Your Local Market: Study up on neighbourhoods, demand for rentals, property values, and future development plans.

Detailed Financial Plan: Know your budget, funds available, swap script and exit plan even with a low budget.

Start Small and Learn: Don’t go for the perfect deal right out of the gate. Concentrate on getting experience and learning the process.

Conclusion

In conclusion, there are some great ways to get started in real estate with little money. Affluent investors shouldn’t be the only ones excited about no monster front-load costs.

People get started in real estate because there is so much potential to invest in one of its greatest commodities: space. Let creativity, education and planning unlock that potential.

Call to Action

Begin learning these low-capital methods today! Get our free real estate crowdfunding guide and connect with a local real estate mentor!

Frequently Asked Questions

1. What is the least amount of capital required to start investing in real estate?

The minimum amount when it comes to the capital required can greatly vary depending on the type of investment strategy you choose; however, some of the crowdfunding platforms may let you start with just a few thousand rupees.

2. Low-capital real estate investments are riskier?

All investments have risk, but low-money plays can be less risky due to diversifying & getting a feel without a large financial commitment.

3. How are dividends paid for REITs?

As a general rule, REITs pay dividends based on the rental income that comes from the properties they own and operate, paying out most of that income to shareholders.

Fed up with your money just languishing there? Imagine it working for you, accumulating wealth as you sleep. Real estate investment represents a compelling path to wealth, and this guide will help you get started investing in real estate property.

We’ll cover the most important concepts, including the benefits of real estate and actionable tips for starting out. Whether you are a novice investor or just interested in diversifying your portfolio, this guide is for you.

Unlock the potential of real estate to diversify your investment portfolio. Find expert tips and strategies to achieve financial growth and stability.

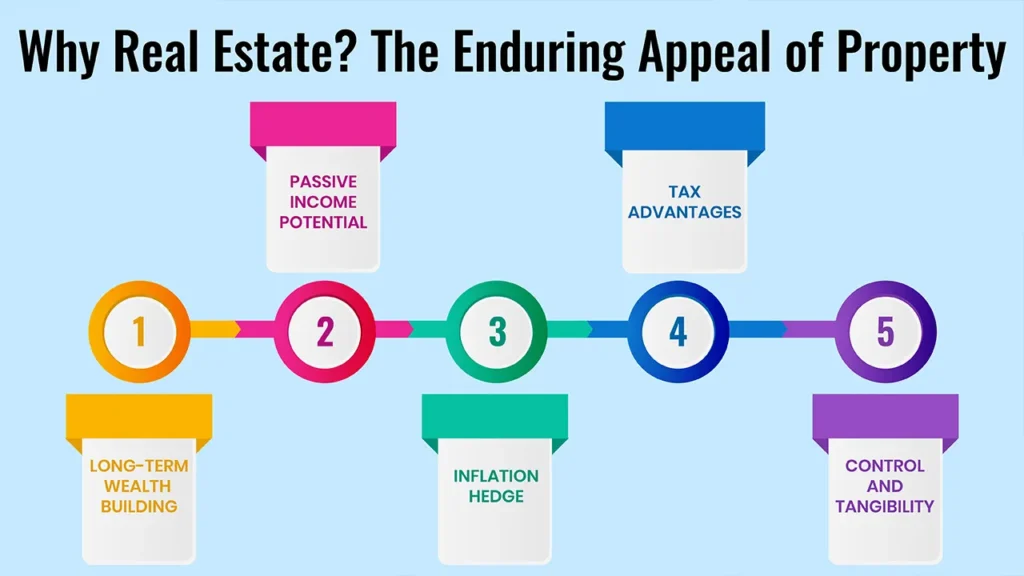

Why Real Estate? The Enduring Appeal of Property

Long-term Wealth Building: Values of property appreciate with time, leading to substantial wealth creation. Real estate investment is an excellent foundation for a solid financial future.

Passive Income Potential: Rent providing an ongoing influx of cash makes the purse strong and enables one to save and reinvest (in more property).

Inflation Hedge: Real estate can hedge against inflation, preserving your purchasing power over time.

Tax Advantages: There are potentially deductions and depreciation benefits and the rules for what are known as 1031 exchanges (there are many rules, and it is generally the best plan to seek a professional with experience in this complex manoeuvre).

Control and Tangibility:Real estate investments are physical assets you can touch, and that means stability and security.

Before You Start: Essential Foundations for Aspiring Investors

Financial Health Check

Good Debt Vs. Bad Debt: Determine the Difference Learn how to manage existing debt so that it doesn’t take away from your financial standing.

Save your Emergency Fund. Save your emergency fund and build it up to be a bit more robust when compared to the norm of 3-6 months of expenses that people stress over.

Good Credit Score: It’s important to have a credit score in good standing to receive financing at lower interest rates.

Setting Clear Goals

Define your objectives in terms of investment, such as passive income purpose, target for capital appreciation, and early retirement. Discriminate between short (and long) range objectives that will shape the strategy.

Education is Key

Invest in your knowledge by those books, podcasts, online courses and mentorship which you trust the most. It is essential to be familiar with the local real estate cycles and trends as you make critical decisions.

Assembling Your Team

Find the necessary professionals to help you on your investment path, such as a reputable realtor, an educated loan officer, an attorney, an accountant and even a property manager.

Most Popular Real Estate Investment Strategies for Beginners

1. Rental Properties (Long-Term)

Concentrate on residential (single-family, multi-family) properties as a means of income. It could be the concept of buying properties and renting them out for predictable, monthly cash flow, albeit with landlord responsibilities that can be transitioned to the use of a property management service.

2. Real Estate Investment Trusts (REITs)

Owning a portfolio of income-generating properties via the public markets provides liquidity, diversification among a range of property types, and professional management. But it can have less direct control over specific IMTs of metadata than direct ownership.

3. Real Estate Crowdfunding

This also pools money with other investors to fund large real estate projects, so you don’t have to fork over a tonne of money to get into commercial or large residential projects. But investments may be less liquid than REITs, and control is minimal.

4. House Hacking

Owner-occupied rentals – Housing costs can be reduced through purchasing a multi-unit property (e.g., duplex, triplex) in which you live in one unit and rent out the others – This also offers first-time landlords a taste of on-the-ground landlording experience. But that depends on having to live on the property, and that might pose a privacy issue.”

5. Market Research

Evaluate the critical factors — such as population growth, job growth and median income patterns. Look into rental demand, average rental prices and vacancy rates, and the amenity and future infrastructure plans for the area.

7. Neighborhood Analysis

Evaluate factors such as the quality of school systems, the area’s crime rate and property value history. Find out if there are any planned development projects in the area.

8. Property Analysis

Do a complete cash flow analysis—projection and calculation of the rental income against every expense. Familiarise yourself with terms such as ‘Cap Rate’, ‘Return on Investment’ (ROI), and ‘Gross Rent Multiplier’. Closely inspect the condition of the property itself and figure out what real estate repairs or renovations you’ll need to make.

9. Networking

Network with local real estate agents, other investors, and residents for leads and insights.

Funding The Dream Of Real Estate: How Various Strategies Stack Up

Traditional Mortgages: Consider such options as conventional loans, FHA loans and VA loans (if you are a veteran). Know the minimum down payment and interest rate.

Hard Money Loans: These are short-term, high-interest loans that will be used for quick acquisition and rehab deals.

Private Money Lenders: People often have more flexibility when borrowing from individuals than from a traditional bank.

Seller Financing: Under this collision, the property seller is turning out to be the lender, thereby lowering the vast dependence on banks.

BRRRR as in “Buy, Rehab, Rent, Refinance, Repeat: this dynamic system gives you the ability to grow your real estate portfolio using the equity from the properties you acquire.

Taking Care of Your Investment: From Tenant Selection to Residential Maintenance

Tenant Screening: I’m assuming you have the service right out of the leg iron; no suggestion that you have no screening, just trying to help you. You should, of course, always protect Fair Housing laws when you screen.

Lease Agreements: Prepare comprehensive lease documents covering all the important terms and legalities to save your property investment.

Rent Collection and Evictions: Create procedures for swift rent collection and learn the laws and numbers to evict when necessary.

Property Maintenance and Repairs: Establish a maintenance schedule, and have plans for emergencies and how to locate trustworthy contractors.

Hiring a Property Manager (Optional): If you’re too busy or you live a great distance from the property, you may want to hire a property manager. Learn what to consider when choosing a qualified property management company.

Common Challenges and Strategies for Overcoming Them

Vacancy Periods: Put measures in place to reduce downtime between tenants, for example, strong marketing and proactive tenant retention.

Problematic Tenants: Learn your legal recourse and how to prevent problems in the first place during the screening process.

Unexpected Repairs: Keep a good reserve fund for emergencies and unexpected costs so you can take care of major repairs without going into debt.

Market Downturns: Take the long view and make sure you have the financial staying power to survive swings in the economy.

Legal Issues: For any complex dispute or question of compliance, contact attorneys to preserve your investment.

We take a closer look at why multitasking is not an asset when it comes to investing in real estate (or anything for that matter).

Conclusion

All in all, beginner real estate investing is realistic, and there are many opportunities to do so. With the tactics provided in this guide, you can open the door to financial independence through real estate investment.

Call to Action

Get the ball rolling on your real estate dreams! Get the real estate investment checklist for FREE and subscribe to get the best tips!

Frequently Asked Questions

How much can I invest in real estate with little money?

The investment minima can range from hundreds to thousands of dollars, but some crowdfunding sites let you get started with just a few hundred dollars.

Is investing in real estate risky?

It is easy to take issue with the pros and cons of the matter, but here’s what I can clarify: Like any investment, real estate comes with risks — market fluctuations, tenant problems, etc. However, if properly researched and managed, these risks can be minimised.

When do you start to make money in real estate?

There is a range of returns based on the nature of the investment, but many investors start seeing cash flow from rental properties in just a few months from closing on said property.

Woodward, Inc. (NASDAQ: WWD), a designer and manufacturer of control and energy system solutions, shares are rocking up 19% on July 16, 2025, without any real company news but with its new bread-and-butter opportunities in a booming artificial intelligence (AI) data centre market and a strong aerospace sector coming back. The company’s shares have jumped more than 50% over the last three months, compared with gains on broader market indices and its peers in the industry.

Uncover the reasons behind Woodward stock surge, fueled by AI data center innovations and aerospace prospects. Get insights into future growth potential.

The AI Boom: How the Next Industrial Revolution Is Being Driven by Data Centre Demand

One of the key drivers of Woodward’s recent rise has been its central role in enabling energy-hungry AI data centres. Although Woodward has long been recognised for its aerospace products, the company’s industrial segment is leveraging the increasing demand for dependable power generation and control systems at these essential installations.

In particular, the company’s reciprocating engine division is proving more attractive as big internal combustion engines become more prevalent in base-load generation and critical backup power at AI data centres and microgrid applications.

That places Woodward squarely in the infrastructure build-out driving the AI revolution. Its controls serve the hydro-turbine, steam-turbine (including fossil, nuclear, ultra-supercritical and geothermal), gas-turbine and centrifugal compressor (including pipelines and injection and removal storage and retrieval) markets, along with other power generation solution applications requiring power up to 700 megawatts.

Aerospace Soars: Commercial Rebound And Defense Spending

At the same time, Woodward’s legacy aerospace business is rocking and rolling with solid recovery in commercial aviation and heightened global defence spending. The company makes crucial fuel systems, actuators and controls for commercial and military aircraft and supplies industry giants like Boeing and Airbus.

Recent highlights include:

52% increase in defence OEM (Original Equipment Manufacturer) sales in Q2 fiscal 2025 driven by increasing global military budgets.

A 23% spike in commercial aftermarket sales in Q2, meaning more use and maintenance of older aircraft.

Prominent Airbus contract to provide the electro-hydraulic spoiler actuation system for the A350 aircraft, deepening Woodward’s presence on advanced new commercial aircraft.

A partnership with Boeing and NASA on a new fuel-efficient aircraft that will be compatible with the aviation industry’s net-zero emissions aspirations.

“Woodward’s precision components are in high demand and at the centre of what makes flight possible, and we see this continuing well into the next decade.

Strong Performance and Positive Financial Outlook

Woodward has fared well financially, posting net sales of $884 million in its second fiscal quarter of 2025, a 6% increase from the year-ago period and topping Wall Street analysts’ estimates. Adjusted earnings per share (EPS) also beat expectations.

The company has raised its fiscal year 2025 sales guidance to be in the range of $3.375 billion to $3.500 billion, which reflects the company’s confidence in its ability to maintain growth. Analysts are optimistic about the company, and several of them rate it as a “buy” or “hold”, noting that the company has positioned itself well in the market and performs well in the segment.

The company competes with other industrial and aerospace giants and wide-ranging economic concerns such as tariffs, but its diversified portfolio and critical role in high-growth sectors set it up well for further growth. Investors will be listening to Woodward’s Q3 fiscal 2025 earnings report on July 28 for more details regarding its performance and strategic direction.

TOKYO/HONG KONG: Asian stock markets were mixed Thursday as investors tried to digest the latest US inflation data and navigate shifting trade policies while technology companies pushed higher on Wall Street.

Particularly in the semiconductor sector, for pockets of optimism. Explore the latest market movements as Asian stocks dip after CPI data while tech gains: markets wrap, while tech stocks gain traction. Get the full analysis in our market.

CPI Data Takes Wind Out of Rate Cut Bets, Pharma’s Dropание

By and large, Asian shares inched down as traders adjusted the degree of interest rate cuts that the Federal Reserve would make. The US Consumer Price Index (CPI) minus volatile food and energy categories rose 0.2% from May – a modest figure, but one that provided a sign that some US companies are raising their prices to counter cost pressures due to new tariffs.

“While any tariff-induced jump to inflation is expected to be temporary, more higher tariffs being imposed means the Fed should still refrain from raising interest rates for a few months at least,” said Seema Shah at Principal Asset Management.

The cautious outlook encouraged traders to chip away at the odds of multiple Fed rate cuts this year, with the likelihood of a September cut now barely better than a coin flip, less than a 20% chance of two rate cuts this year. These revised policy bets typically bear down on riskier assets in Asia.

In a similar sector-specific drag, Asian pharma stocks fell following renewed threats by US President Donald Trump to impose tariffs on pharmaceuticals by the end of the month.

(Tech Outperforms as Chip Export Expectation Lifts Seoul)

Tech stocks across Asia, in turn, bucked the broader market decline, supported by favourable developments in the semiconductor sector. The Hang Seng Index in Hong Kong added 0.3 per cent, largely on the back of tech companies.

One big catalyst was word that US chip behemoth NVIDIA has received assurances from the US government that it will be able to resume exporting its H20 artificial intelligence accelerator chips to China.

This radical shift from an earlier position held by the Trump administration is considered quite bullish for the AI semiconductor supply chain and general US-China relations, especially when the two sides are negotiating levels of tariff amounts, which is a very positive development.

Taiwan Semiconductor Manufacturing Co. (TSMC), a critical NVIDIA partner and one of the largest global manufacturers of chips, TSMC, TSMC, Copper Tubes, TYO, 2330 c1, rose as much as 1.8% in Taipei after a media report suggested the company intends to build a second chip plant in Japan to diversify its production, including for chips used in the automotive sector.

South Korean tech companies including Samsung Electronics (005930.KS) and SK hynix (000660.KS) are also riding the wave, as Samsung Electronics ended 1.57% higher on Monday, a sign of broader optimism across the semiconductor sector.

Regional Performance Snapshot

Japan’s Topix was little changed as the Nikkei 225 edged 0.58% higher on July 15, supported by tech advances amid broader market wariness.

Australia’s S&P/ASX 200 lost 0.8 per cent, with the broader index weighed down by inflation worries.

Hong Kong’s Hang Seng index rose 0.3 per cent, boosted by its tech component. Chinese mainland markets, including the Shanghai Composite, fell slightly, down 0.1%.

South Korea’s Kospi fell 0.73% as broader worries about the economy overwhelmed technology sector optimism for the overall index.

Meanwhile the Japanese yen was 0.2% weaker versus the dollar, close to levels not seen since April, as the market considered the possibility of divergent monetary policy stances in the US and Japan. Gold, another traditional safe haven, nudged higher.

As global financial markets grapple with the prospect of inflation, interest rate assumptions and the changing world of trade, the gap between general market sentiment and the success of AI-powered tech stocks illustrates the themes dominating investment strategy decisions in mid-2025.

Retirement is creeping up on you, and perhaps you feel the ticking of the clock. But the good news is this: your later career years can actually be some of the most impactful when it comes to turbocharging your retirement savings!

This guide is intended for people in their 50s and early 60s who are nearing retirement. This stage is so important because you have a lot working for you, including peak income potential, the ability to maximize your contributions to savings and retirement, and having an idea of what retirement feels like.

Navigate the complexities of late career retirement planning. Learn how to maximize your savings and ensure a comfortable retirement lifestyle.

The Landscape of Late-Career Retirement Planning Tap Qualified or not?

Advantages You Have

Greater Income Potential: Typically this is when you make the most money.

“Catch-Up” Contributions: Designed as a way for older savers to make up for lost time, you can contribute more to retirement accounts.

Less Debt (Maybe): Some people may have paid off — or paid down — their mortgage.

Sharper Vision: You probably have a clearer vision of your retirement dream.

Specific Challenges

Time Horizon: Time for Compounding to Wonder on Miracles.

Risk of Market Volatility: Less time to recover after a large market decline.

Health-Related Expenses: A significant worry that rises as we age.

Caregiving Duties: You might have to help ageing parents or grown children.

Insecure employment: The possibility of unexpected job loss is more threatening as retirement nears.

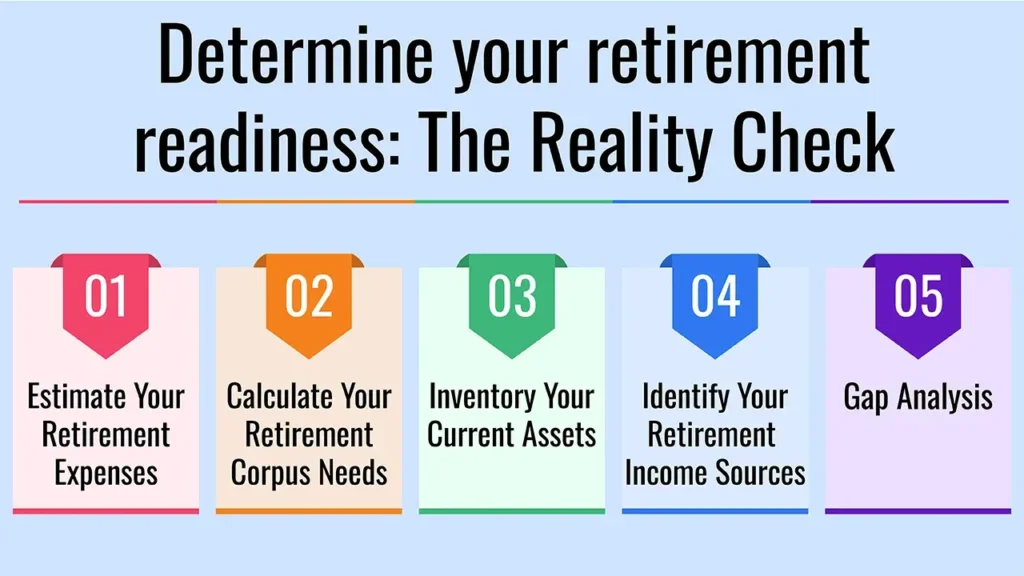

Step 1: Determine your retirement readiness: The Reality Check

Determine Your Retirement Date: When do you want to retire versus when can you afford to retire?

Estimate Your Retirement Expenses: Establish a comprehensive post-retirement budget to cover housing, food, health, travel, hobbies and entertainment. Keep in mind to adjust for inflation and the possibility that other spending niches could increase.

Calculate Your Retirement Corpus Needs: What target do you need to hit to sustain the lifestyle you want? It’s best to use rules of thumb, such as 25-30 times annual expenses, or a comprehensive retirement calculator.

Inventory Your Current Assets: Mention all retirement accounts (EPF, NPS, PPF, mutual funds, stocks, and real estate), savings and other investments.

Identify Your Retirement Income Sources: Include pensions (if any), NPS annuities, rent and systematic withdrawal plans (SWPs) from mutual funds.

Gap Analysis: Compare your estimated future needs with your existing savings and income sources to determine the “gap” you have to make up.

Step 2: Save and Contribute as Much as Possible

Supercharge Retirement Accounts

Catch-Up Contributions: Avail of such enhanced limits for above 50 category (following are the specific provisions concerning NPS, EPF or such other government/employer schemes in India)

Leverage EPF/VPF: To the extent applicable, enhance voluntary provident fund (VPF) for assured return and tax advantage.

NPS (National Pension System): Avail of tax benefits under Section 80CCD(1B) for investments over and above 80C.

PPF (Public Provident Fund): Invest the maximum every year and get tax-free returns.

ELSS (Equity Linked Saving Schemes): For 80C tax benefits along with exposure to equities, you may consider this.

Aggressive Savings

Trim your discretionary spending and figure out how to raise your savings, perhaps by paying yourself first via automatic transfers.

Convert Non-Earning Assets

Some things you should consider: Selling off your “extras” (like a second home or expensive cars) in order to ramp up your retirement savings.

Step 3: Refine Your Investment Plan

Risk Reassessment

Start the transition of your portfolio from high growth to balanced or conservative. And the aim should be to preserve capital and to grow income, not to see aggressive how-much-can-I-do growth.

Asset Allocation

Talk about the need to “rebalance” as you get older and reduce your exposure to stocks and increase exposure to debt/fixed income as retirement edges closer (i.e., you’ve got a 60/40 equity-to-debt ratio when you’re 40, but that should maybe be more like 40/60, eventually 30/70).

Income-Generating Investments

Debt Funds: For stability and moderate returns.

Fixed Deposits (FDs): Safe and sure income, but no tax benefits.

Senior Citizen’s Savings Scheme (SCSS): The SCSS is a government-guaranteed scheme for regular post-retirement income (if you were eligible).

Annuity Plans: Explain about them being the source of providing guaranteed income for life but also their drawbacks (no liquidity, low returns)

Tax-Efficient Withdrawals

Develop a withdrawal strategy for your various accounts (taxable and tax-exempt) to reduce your tax liability in retirement.

Step 4: Strategic Debt Management

Goal: Debt-Free Retirement

Pay off all high-interest debt (credit cards, personal loans) before retirement.

Mortgage Strategy

Strive to have your home loan repaid or a substantial debt reduction by the time you retire. This will leave you with a sizeable amount of cash flow in retirement.

Avoid New Debt

Be very cautious about taking on extra loans or expanding your debt as you near retirement.

Step 5: Critical Insurance and Healthcare Planning

Health Insurance

Make sure you have good health insurance that carries over into retirement. Think about a super top-up or critical illness policy to meet larger medical expenses.

Long-Term Care (LTC) Insurance

Although relatively infrequent in India compared with parts of the West, talk about whether it makes sense to provide for the possible cost of assisted living or nursing care.

Life Insurance Review

Reevaluate whether you still need term life insurance. If your dependants are no longer depending on your income, you may have the option of scaling back or completely dropping coverage in order to cut costs.

Step 6: Retirement’s Non-Financial Impacts on Households

Define Your Retirement Lifestyle

What are you going to do when you retire? Think about hobbies, travel, volunteer work, family or a passion project.

Social Connections

Be sure to make time for socializing in order to improve your quality of life.

Housing Decisions

Consider downsizing, moving to a less expensive part of the country or taking out a reverse mortgage (on which you should be very sceptical and very careful and should consult experts).

Part-Time Work/Encore Career

Could you work part-time in retirement for a little extra income?

Estate Planning

Review any will or power of attorney documents you have, and think about designating beneficiaries for your assets.

Step 7: Importance of Seeking Professional Help

When You Need a Financial Adviser

If you feel frazzled or have complicated financial circumstances, consider hiring a financial adviser to help with a personalized game plan.

What a Financial Planner Can Offer

A financial planner can help with goal identification, cash flow analysis, investment rebalancing, tax planning, estate planning and withdrawal strategies.

Choosing the Right Advisor

Identify SEBI-registered Investment Advisors (RIAs) or Certified Financial Planners (CFPs) who would provide independent advice and work on a fee-only model.

Conclusion

Focused action in these late working years really can make a difference in your retirement security and comfort level. And with the right moves today, you can be on the road to a full and financially secure retirement.

Call to Action

Begin your retirement checkup today! For help putting the finishing touches on your late-career strategy, seek advice from a financial planner — and download our retirement checklist!

Frequently Asked Questions

1. At age 50-something, is it even worth saving for retirement?

It’s never too late! Although you can’t save as long, there are ways to make the most of your retirement savings.

2. What are the best low-risk investments for someone about to retire?

For stability and predictable returns, you can look at vehicles such as fixed deposits, debt funds, government-backed schemes, etc.

3. What are the best health insurance options for retirees

Ideally, you should look at a comprehensive health insurance plan which includes hospitalisation and outpatient cover and also consider Super Top-up plans for additional cover.

That shiny new “real” job just land in your lap? Excited, yes, but also a little overwhelmed by adulting and running your own finances? You’re not alone! Young professionals have a difficult road to hoe when it comes to money.

Early financial education ensures long-term prosperity and helps to avoid common pitfalls. This manual covers important topics including budgeting, investing and debt reduction and will equip you with the knowledge that you need to secure the financial future that you deserve.

Empower your personal financial planning for young professionals. Learn to budget, save, and invest wisely for a prosperous future.

The Financial Reality of the Young Professional

Common Challenges

Student Loan Debt: A heavy onus for the young workforce.

Lower Starting Salaries: Aspirations vs. current salary is always a conflict.

High Cost of Living: Being so even more in the cities.

Lack of Financial Education: Money management is typically not part of an official curriculum.

Peer Pressure/Lifestyle Creep: Keeping up with the spending of pals can put your finances in a bind.

Shaky Economy: Swings in the job market and at the pump can add to frayed nerves.

The Advantage: Time!

The biggest advantage you have as a young professional is time. Beginning your financial planning process early helps you realize the magic of compounding that adds to your wealth to a great extent in the long term.

Step 1: Take Control of Your Cash Flow with A Great Budget

Why Budgeting is Essential

Budgeting is the cornerstone of any financial planning. It gives clear insight into where your money is going, and ensures that you’re able to reach all your personal spending and savings goals.

Understanding Income & Expenses

Net Income vs. Gross Income: Understand the gap between what you make and what you keep.

Fixed vs. Variable Expenses: Determine what you COULD spend, compared to what you NEED to spend:

Famous Budgeting Methods For The Young Professional

50/30/20 Rule: Give 50% of your income to needs, 30% to wants and 20% towards savings or debt.

Every Rupee Has a Job – Zero-Based Budgeting: Income – Expenses = Zero.

Envelope System: This one is great for tactile learners and involves using cash to budget.

Tools for Budgeting

You could use an app like Mint or YNAB, spreadsheets or banking apps to track your spending.

Tips for Sticking to a Budget

Automate your savings, keep an eye on your spending, revisit your budget often and adapt when necessary.

Step 2: Lay the Foundations of Your Financial House: The Emergency Fund

What is an emergency fund?

An emergency fund is a sum of money set aside for unanticipated expenses, such as losing your job, a medical crisis or auto repairs.

Why You Need One: Having an emergency fund is crucial for peace of mind and financial security amid challenging moments.

How Much to Save: Really try to save 3-6 months’ worth of basic living expenses this time, adjusting based on your job security.

Where to Keep It: Look into high-yield savings accounts (HYSAs) for liquidity and growth.

Step 3: Tackle Debt Strategically

Identify Your Debts

What are common types of debts?

Prioritize High-Interest Debt

You’ll want to pay off credit cards first because they typically have the highest interest rates.

Debt Repayment Strategies

Debt Avalanche: Repay debt with the highest interest rate first to save the most money.

Debt Snowball: Pay your smallest balance to gain a mental win.

Student Loan Specifics

Know your options when it comes to repayment, to include refinancing and deferment/forbearance (but only if you must).

Avoid New Bad Debt

14 of 19 Practice credit card discipline and know your APRs Whether using a credit card to bridge the gap, always practise credit card discipline to avoid adding to your debt.

Step 4: Begin Investing Young: Your Wealth Turbo Charger

The Power of Compounding (Revisited)

Demonstrate the concept of compounding over time and how an early investment can result in exponential growth later.

Defining Your Investment Goals

Think about your objectives — whether it be retirement, a down payment on a home, or early financial independence.

Understanding Risk Tolerance

Determine how much volatility in your investments you can handle.

Beginner-Friendly Investment Options

Employer: Sponsored Retirement Plans: Like 401(k), EPF, and NPS, if your employer provides a match.

IRAs (PPF/Roth IRAs): Explain tax benefits and flexibility.

Index Funds & ETFs: Perfect low-cost diversification.

Mutual Funds: Diversified portfolios managed by professionals.

Direct Stocks: If you’re willing to do the homework and accept more risk.

Automate Your Investments

Create scheduled contributions to streamline investing.

Step 5: Watching Your Back: Insurance Basics

Why Insurance Matters

But insurance does protect you from unexpected risks that could derail a plan you’ve worked hard on creating.

Young Professionals, 5 types of insurances you should have

Medical Insurance: Most important for accidents and illnesses.

Term Life Insurance: This is a term. Insurance is substantial if you have dependents and/or co-signed loans.

Disability Insurance: Provides income if you become unable to work.

Renter’s/Homeowner’s Insurance: Covers your stuff and liability.

Car Insurance: Compulsory for all owners of cars.

Understanding Coverage and Premiums

You can’t just shop for the lowest price; you need to know you have the coverage you need.

Step 6: Factor in Big Life Events (not Just Retirement)

Buying a Home: Begin saving for a down payment and familiarise yourself with mortgages and property taxes.

Marriage & Family Planning: Think about your shared finances and expenses for the child – for example, schooling and health care.

Career Growth & Upskilling: Put money in yourself to make more.

Wealth Building Mindset: Take a long-term view and resist the urge to splurge.

Step 7: Get Professional Help (When to Find a Financial Planner)

When It’s Beneficial

If your finances are complex, such as when you are high-net-worth or have something unusual like an early retirement, it may be a good idea to seek the help of a financial advisor.

Types of Advisors

Get the distinction between fee-only and commission-based advisors.

What to Look For

Look for certifications (like CFP), experience and a clear fee schedule.

Conclusion

It’s a lifelong process, not a one-time event. When you take control of your personal financial situation now, it becomes a platform on which you can build a better future.

Call to Action

Get started on the journey of financial planning! Download our budget template here for free, and subscribe to get more financial advice.

Frequently Asked Questions

1. How much savings should I be doing as a young professional on a monthly basis?

A good general rule is to save at least 20% of your income, but it varies depending on your personal situation.

2. What are the top financial mistakes young professionals make?

People often fail to budget, rack up high-interest debt and don’t save for an emergency.

3. Which is better, to pay off students loans or think about investing first?

It all comes down to your interest rates and financial goals. For the most part, if you have a low student loan interest rate, getting invested early can pay off.

Swiss Re Institute predicts that a potential impact of rising US tariff policy is slower global economic growth. The reinsurance colossus’ most recent “World Insurance sigma” report, published July 9, 2025 says these protectionist steps will not only hinder global GDP expansion but will also inhibit insurance premium growth internationally.

Explore how US tariffs are set to impact the global economy and insurance premium growth, as analyzed by Swiss Re. Stay informed on key economic trends.

Tariffs to Trigger “Stagflationary Shock”

The global average rate (real GDP growth) is expected to slow to 2.3% in 2025 and 2.4% in 2026, having stood at 2.8% in 2024. This slowdown has been primarily caused by the widening US tariff policy which is causing a ‘stagflationary shock’ to the US, and by extension the broader global economy, and is designed to obliterate policy uncertainty worldwide, the report states.

Jérôme Haegeli, Swiss Re’s Group Chief Economist, pointed to the short-term effect. “US consumers will be the most affected by US’ tariff policy and cut their consumption because of increased prices. This will in turn bear down on US growth which is largely driven by household consumption.” Swiss Re expects a slowdown in US GDP growth to just 1.5% in 2025 after 2.8% in 2024.

“Additional tariffs would lead to structurally higher inflation in the United States” as supply chains become less efficient and domestic industries face reduced competition from other countries, the report said. This mix of weaker growth and accelerating prices creates a thorny new world for businesses and consumers.

Insurance Premium Growth to Halve

There’s to be a ripple effect from a lightened global growth and increased uncertainty, and the insurance sector like no other will suffer. Global insurance premium development will slow down considerably to 2% in 2025, about half of the 5.2% seen in 2024, according to projections by the Swiss Re Institute. In 2026, a low partial recovery to 2.3% is expected.

Premium growth down in both life and non-life segments:

Nonlife growth of premiums is forecast to fall to 2.6% in 2025 from 4.7% in 2024 as competition in personal lines and softening market in some commercial lines.

The pace of growth in life insurance, in particular, will cool even more sharply, with premiums rising 1% in 2025, down from a 6.1% increase in 2024 — higher interest rates are set to moderate.

US tariff policy is another step toward increasing market fragmentation longer-term, which would decrease insurance affordability and availability, and thereby global risk resilience, Haegeli cautioned.

Trade barriers potentially leading to higher claims costs for insurers and supply chain disruptions, and cross-border flow of capital restrictions on reinsurers that may lead to capital allocation inefficiencies and higher capital costs and, ultimately, higher insurance pricing, are cited in the report.

Uneven Impacts and Emerging Opportunities

While the tone is in general cautious, the report states that the impact of tariffs on the insurance sector is likely to depend on geographic regions and lines of business.

US Motor Physical Damage This insurance sector is anticipated to bear the brunt of the tariff rise with auto parts and new/used cars prices surging and hence higher claims severity. Swiss Re predicts US motor damage repair and replacement costs will rise by 3.8% in 2025.

Our commercial property and homeowner and engineering lines in the US could also experience an increase in claims severity coming from higher costs for the intermediate goods, machinery, and commodities.

Tariffs outside the US are usually thought to be more disinflationary and could reduce claims pressure.

But the added uncertainty and economic disruption could also present opportunities, and credit and surety insurance that guard against economic disruption might be in higher demand. Alives could affect marine insurance as well, given changes to trade routes and supply chain realignments.

Notwithstanding the decline in premium growth, Swiss Re says that the overall profitability position of the global insurance industry remains robust, benefiting principally from ongoing investment income gains.

Yet the report is a stark reminder of how international trade policies and protectionism can have such widespread economic implications for wider global growth and important sectors, such as insurance.