Small business owners everywhere need one thing: affordable, adaptable credit for growth, to manage cash flow, or to take advantage of new opportunities.

As the worldwide small business lending market is expected to exceed the value of $3 trillion by 2032, there is an extensive range of creative lending options in every corner of the globe, whether in North America or Asia-Pacific, Europe or Africa.

That could help entrepreneurs make strategic decisions on borrowing regardless of their business’s location in 2025.

Small Business Differential Power and Global Lending Trends

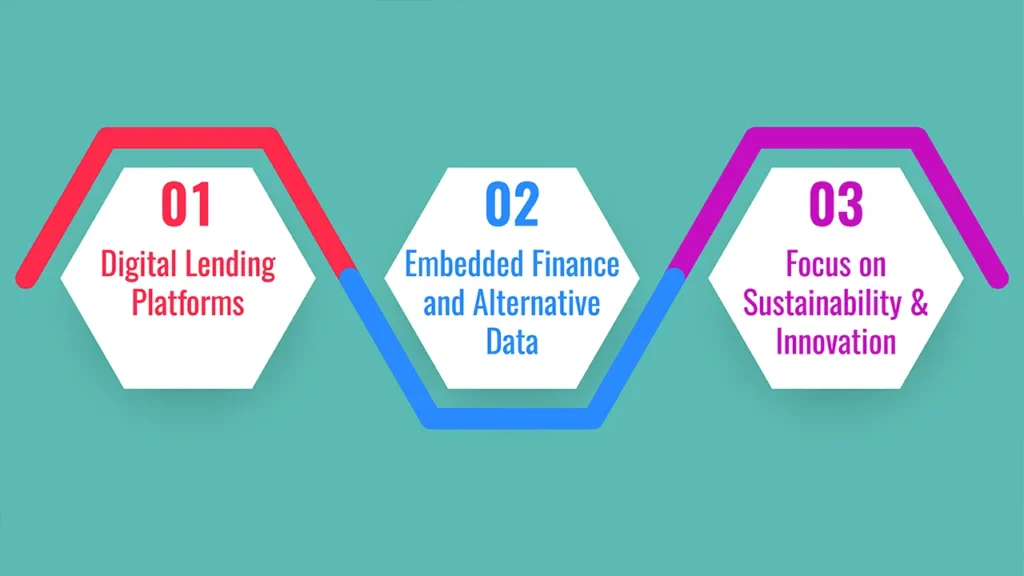

Digital Lending Platforms

Fintechs and digital banks are revolutionising small business lending on every continent. That’s where online players can play; don’t underestimate the speed of approval and very low paperwork, and they employ advanced analytics/alternative data in underwriting so it increases access to finance even in the underserved markets, achieving mass affluence.

Embedded Finance and Alternative Data

Progressive lenders are integrating financial products into e-commerce and payment platforms (such as PayPal) and tapping data like business cash flow, sales data and even social signals to offer loans faster to more entrepreneurs.

Focus on Sustainability and Innovation

In Europe and some parts of Asia, “green loans” and technology-focused funds are the rage, assisting businesses that are more environmentally minded or pursuing improved technology.

Top Small Business Loan Options and Providers Worldwide

1. Bank and Government-Backed Loans

United States:

- The SBA guarantees 7(a), 504 and microloans, with funding between $500 and $5.5 million at interest rates between 6.6% and 11.5%, on average.

- Large banks such as Bank of America, Wells Fargo, and TD Bank provide solid products for small business lending, generally for more established companies.

Europe:

- State-run and -regional banks, often with EU assistance from its European Investment Fund, are promoting flexible credit and green financing for startup and SME loans.

- Interest rates may vary on small business loans: the last data for the Eurozone is the 6–8% range, and the US rates are around 7–13%. These rates can be higher due to the risk in the business and the low collateral value of the financed asset.

Asia-Pacific:

- The growth markets—such as India and China—have been experiencing dramatic growth in small business lending—often brought about by national banks and digital-first lenders, aided by government subsidy programmes for newly minted small business entrepreneurs.

- Examples of programmes: India’s Mudra Yojana and Unified Lending Interface; China’s SME digital bank loan facilities.

Latin America & Africa:

- The expansion of microfinance and mobile lending through companies such as Nubank or M-Pesa and from commercial banks is helping to make life easier for SMEs.

2. The World’s Leading Online Lenders & Marketplaces

Fast, Unsecured Business Loans and Lines of Credit: The 11 Best Options International fintechs lead with lightning-fast, unsecured business loans and lines of credit:

Bluevine, Lendio, OnDeck, Fundbox, Finance Factory (US/global):

- Short-term loans, lines of credit, and working capital with simple online applications, fast decisions, and a high likelihood of being approved for companies or new or small businesses with limited revenue.

- Users generally borrow between $5,000 and $500,000.

- Rates: APRs vary, but short-term products can have rates from 12% to 35%.

PayPal Working Capital (US, UK, Australia, and more):

Soft loans are facilitated by sales made on PayPal, where the payments are in turn deducted based on portions of future revenues, instead of fixed monthly amounts.

Regional Fintechs (e.g., Kabbage, Capify, Funding Circle, QuickBridge):

- Localised (UK, EU, Australia, Canada and some Asian countries) for these lenders are all unsecured loans, invoice factoring and equipment finance.

3. Sector-Specific and Green Financing

- Green loans: These are used to finance energy-efficient projects, sustainability programmes, or environmentally focused startups and are more common in Europe and Asia.

- Equipment and invoice finance: Available globally, providing companies with access to money against assets or receivables.

Small Business Loan Offers: By The Numbers – Regional Breakdowns

| Region | Common Loan Products | Typical Interest Rates | Notable Lenders/Schemes |

|---|---|---|---|

| North America | SBA loans, Bank and Fintech loans | 6.6%–14% (bank/SBA); 12%–35% | SBA, BoA, TD Bank, OnDeck, Bluevine |

| Europe | EU, national bank, fintech, green | 6%–9% (bank/EU); 12%+ fintech | EIF, Funding Circle, Capify, PayPal |

| Asia-Pacific | Gov’t programs, banks, fintechs | 7%–18% (bank/gov); 12%+ fintech | Mudra Yojana, ULI, Kabbage, Funding Soc. |

| LatAm/Africa | Microloans, new digital lenders | 12%–40% (wide range) | Nubank, M-Pesa, local MFIs |

What Matters Most in 2025

Speed and Accessibility

For growing businesses, speedy approvals and little paperwork are table stakes — and fintechs and online lenders have overlap here.

Cost and Repayment Flexibility

Compare effective APRs, fees and terms of repayment (monthly, weekly and by per cent of sales).

Support and Extras

Many lenders also provide educational resources, mentoring, or links to business management tools so owners can make a success of the business.

Creditworthiness

Traditional banks prefer more established or creditworthy companies, while fintechs and micro-lenders take a broader view, not least in developing markets.

Practical Tips for Global Entrepreneurs

- Define the Purpose: Is this money going toward working capital, inventory, machinery or a big expansion? Tailor your loan to your business purpose.

- Shop and Compare: Be sure to compare offers at traditional banks with government programmes and with those of small-business lenders on fintech and marketplace platforms.

- Gather Documents: Get your financials, business plan, and any applicable credit or registration documents prepared in order to quicken the approval process.

- Respect Local Rules: Rates and fees vary by country—check local deals before applying.

- Factor in Currency & Economic Impact: When borrowing internationally, consider the impact from currency changes and world interest rate trends.

Conclusion: The Small Business Loans of 2025

Small business lending in 2025 is more dynamic, more inclusive and more tech-enabled than ever before, around the world. From the world’s largest international banks and government-sponsored programmes to nimble fintech startups, today’s entrepreneurs have access to an incredible array of funding options to get the capital they need — either at home or abroad.

The trick is to make an educated choice — that means comparing those costs alongside speed, service and how each product fits into its unique business objectives. With information and clever comparison, small business owners can make decisions that get them on the right course to financial growth and resilience.

Frequently Asked Questions (FAQs)

1. What are the various kinds of small business loans in the world for 2025?

Terms of loan, interest rate, eligibility, and promptness differ by region, type of lender, and borrower’s purpose for the loan. There are also several government schemes designed specifically to assist small businesses here with access to low-interest or security-free credit.

2. What can small businesses do to increase their odds of getting a loan?

Clearly state the loan purpose. Show firm business planning and realistic cash flow projections. Picking a lender that’s the right fit for business size and stage, as well as talking to government guarantee schemes or fintech lenders that use alternative data, can also make a difference.

3. What should small business owners look for in a loan?

It’s also important to take into account how well the loan aligns with the business’s specific needs — whether for working capital, equipment, or to expand — and to be aware of local lending regulations and currency risks in international facilities.