Real estate investing is one of the most common ways to accumulate wealth the world over. You watch property values increase, but how can you be sure if your investment is really profitable?

This post will break down how to calculate your Return on Investment (ROI) in real estate. You will understand all of the primary real estate ROI formulas, which costs and gains are important and how to calculate the profit of your property, regardless of where you are investing.

1. Understanding Real Estate ROI: The Basics

Definition:ROI (Return on Investment) is a percentage that indicates the amount of profit you have made on an investment compared to the purchase price. It’s your ultimate “profit score”.

Easy to Understand: In it, you invest money and try to get back more money. ROI measures how efficient that return was.

Why It Matters: ROI is important when it comes to assessing past investments, comparing opportunities, and making new ones in the future.

2. How to Calculate Your Real Estate ROI Step by Step

There are Different Things to Count as “Cost” and “Return”: Key Components

1. Total Investment (All money in the deal):

Purchase price of the property.

Closing Costs: Legal fees, transfer taxes, title insurance premium, appraisals, home inspection fees, loan origination fees (if any), and broker’s commissions (if you are paying them).

The remaining balance of any substantial repairs or rehab that need to be performed to get the property to functional or marketable condition.

2. Total gain (sum of all money received or gained):

Selling Price: The price at which you sell the property.

Rental Income: Everything you’ve ever collected from tenants while you’ve been an owner.

3. Rental & Sale Costs (Money you paid while in, or upon selling):

Property Taxes.

Homeowner’s Insurance.

Regular Maintenance & Repairs.

Loan Interest Payments (if financed).

Utility costs (if landlord pays).

Property Management Fees (if applicable).

Sale costs: sales commissions, legal fees, transfer taxes at the time of sale, possible capital gains taxes.

How to Calculate Return on Investment (ROI): Examples for Common Scenarios

Example 1: No Rental but a Resale Property from the Developer (Simplest Case)

You purchased a property for $200,000 (including all of your initial closing costs). You sold it 3 years later for $300,000. The total selling expenses (commissions and taxes on sale) were $15,000.

Solution: Net Gain = Selling Price – Total Initial Investment Cost – Total Selling Costs Net Gain = 300,000 – 200,000 – 15,000 = 85,000 [] ROI = \left( \frac{85,000}{200,000} \right) \times 100% = 42.5%

Translation: For each dollar invested, there was a profit of $0.425.

3. More Than Simple ROI: Advanced Metrics for Savvy Investors

Advanced Tools for a Clearer Financial Picture

1. Cash-on-Cash Return:

What it means: Your annual cash profit versus the actual cash you have put into the home (for example, the down payment and closing costs), not counting borrowed funds.

Why it’s helpful: Excellent for comparing a property purchased with a loan, and it displays gross cash flow.

2. Capitalisation Rate (Cap Rate):

What it means: The annualized rate of return on an income-generating property, based on the property’s purchase price and no financing (though financing may be used in the actual purchase).

Why it’s helpful: Can assist in quickly comparing the profitability of various income properties.

What it tells you: How much in interest the bank has paid you for your investment in one year’s time.

Why it’s useful: Allows for a more apples-to-apples comparison of investments held for different time periods that factors in the time value of money.

4. Main Factors of Your Real Estate ROI

What (or Who) Determines Property Profitability

Location: Value and rent demand of a property is largely a function of how close it is to amenities, infrastructure, jobs and good local economies.”

Market conditions: supply and demand, economic growth, interest rates and inflation.

Type Of Property: Home, business, industrial, land… each with its own risk/return profile.

Property Conditions & Maintenance: Well-kept-up properties bring in superior tenants and buyers. High costs of repair can cut into the returns.

Financing Expenses: Mortgage interest rates play a direct role in your available cash and overall returns.

Taxes & Fees: property taxes, transfer taxes, income taxes on rental profit, and capital gains taxes all cut into your net returns.

Vacancy Rates: Empty units bite into the bottom line for rental properties.

Section 5: Limitations of ROI

Behind the Number: What ROI Does Not Always Reveal

Time Value of Money (for the simple ROI): A simple ROI alone doesn’t tell us how long it took to get that back. Use CAGR for this.

Risk: A high return on investment can also mean high risk. It does not measure its own risk level.

Liquidity: Real estate is illiquid, and turning it into cash can be a big hassle.

Effort: It does not take into consideration how much time and effort it takes to manage the property.

Surprise Costs: Things like big-time repairs or legal problems can throw actual ROI for a major loop.

Inflation: Be sure to figure your real return after inflation eats away at purchasing power.

Conclusion

Learning how to calculate your Return on Investment (ROI) in real estate is more than just serving and crunching numbers – it’s (arguably) the most important part of a real estate investment.

When you are computing your ROI correctly with all the costs and benefits and using the appropriate metrics for your particular situation, it provides you with a lot of great information as to how your property is really doing. It gives you that knowledge so you can make better, more lucrative investment decisions!

Call to Action

Begin to apply those formulas to your existing properties or future investments. The more you know, the more money you make.

Frequently Asked Questions

1. What is a “good” ROI in real estate worldwide?

There’s no such thing as a “good” ROI, and it’s conditional on location, type of property, specific market conditions and how much risk you and your client will take on. Most investors are looking for returns that far outstrip inflation and non-stock investments.

For rental income (cap rate or rental yield), perhaps a solid range for many stable markets is 4-8%, while overall ROI, including appreciation, might want to average 8-15% or more on an annual basis depending on the type of investment and specific market.

2. How is ROI affected if we are taking a mortgage (loan)?

The answer is :yes! Using other people’s money (aka leverage) can have a dramatic effect on your ROI. Though a simple ROI won’t include specifics about the loan, high interest payments lower your net profit.

Metrics such as Cash-on-Cash Return are engineered to show your profit measured against how much cash you put in the investment, which is specifically useful for mortgaged properties.

3. Do I have to add in the capital gain taxes that I have to pay when calculating the 9% return needed?

Absolutely. You also need to subtract all tax consequences of the investment, including capital gains taxes on sales, for an accurate estimate of your net profit. These are flat-out costs that syphon away the money you get to keep.

4. Can we always say that the higher the ROI, the better?

Not necessarily. A very high ROI might mean that there’s a greater associated risk. Return potential must be balanced against risks, liquidity and work involved in the investment. Always consider the risk-adjusted return.

Bored of your money just sitting there? Think of it as a friend doing the work for you, growing riches while you sleep. Investing in real estate is a great way to build long-term wealth and financial security.

To help you get started, we have put together a complete a beginner’s guide to real estate Investing that covers the steps needed to begin investing in real estate. From learning how to invest in real estate to finding your first investment property and taking care of it, we’ve got you covered.

Why Real Estate Investing?

Investing in real estate has some fantastic advantages making it one of the best ways to build wealth! Here are some key advantages:

Passive Income: Rental properties can create a passive income stream allowing you to earn money while you are off doing other things.

Appreciation: As your property value generally increases over time, you’ll have a capital gain when you sell.

Tax Benefits: Real estate investors enjoy a number of tax benefits, such as mortgage interest deductions, property taxes and depreciation.

Inflation Hedge: Real estate generally increases in value during times of inflation, preserving the purchasing power of your investment.

Control and tangibility: Real estate which is unlike stock or bond, is a tangible asset that is yours to work on and to improve.

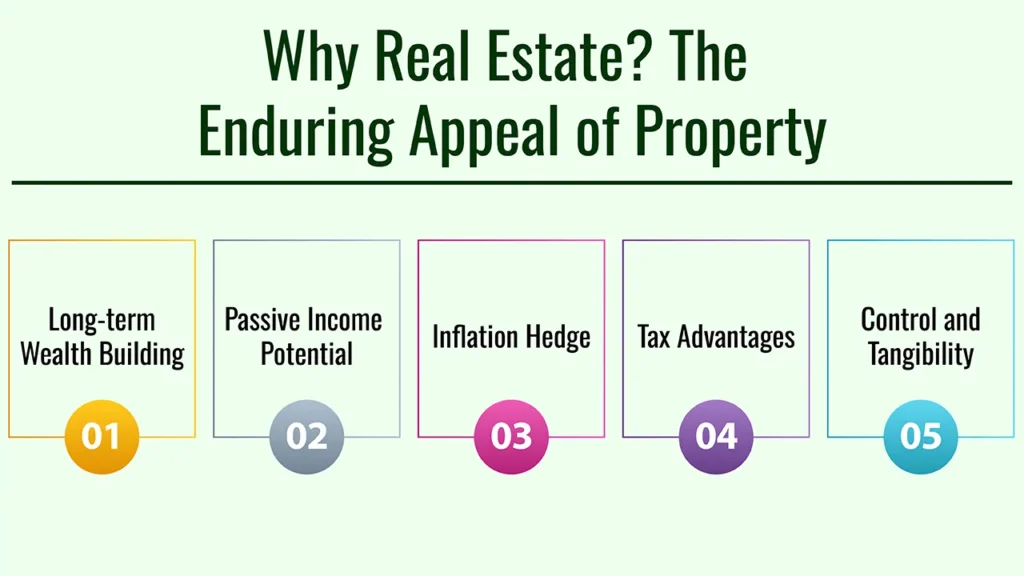

Why Real Estate? The Enduring Appeal of Property

1. Long-term Wealth Building

Real estate has always been one of the most reliable ways to accumulate wealth over the long term. Property tends to increase in value, so your investment has the potential to increase in value as well.

Historically, real estate does extremely well relative to other asset classes over long periods of time, and so it’s a good decision that should provide you with lots of wealth over time.

2. Passive Income Potential

One of the appealing things about real estate investment is the promise of passive income. Through buying rental units, you can make money on a monthly basis with tenants.

This income can be put toward your mortgage payments, property taxes, and maintenance and can also give you an additional cash stream.

3. Inflation Hedge

Real estate is an inflation hedge. If the cost of living is going up, if rents are going up and property values are going through the roof. This is what one calls protecting your investment from the ravages of inflation and choosing wisely for your financial security over the long run.

4. Tax Advantages

There are many advantageous tax benefits to investing in real estate. Mortgage interest, property taxes and certain costs associated with property management can all be written off for investors.

Moreover, depreciation enables you to lower your taxable income, maximizing your cash balance even more. Another tax strategy is the 1031 exchange, which allows you to defer capital gains tax when you sell one property and invest the proceeds in another property. This is likely to be complicated and you may need some professional help.

5. Control and Tangibility

Real estate provides more power being tied to it as an investment, during this period. Property management can be done by you, you can also decide which tenant you want to have, and you can decide if you need to do renovations.

And there’s something about real estate that is a physical, touchable investment, as opposed to something intangible real estate can provide that security other investments can’t.

Before You Start: The Must-Know Fundamentals for Aspiring Investors

Financial Health Check

Before jumping into real estate investing, you need to get a handle on your finances. Here are several factors to keep in mind:

Debt Management: Understand the difference between good and bad debt. Good debt, such as a mortgage, can help you build wealth, while bad debt, like high-interest credit cards, can hinder your financial progress.

Emergency Savings: Make sure you have a cushion to cover any unforeseen costs. Having a well-funded emergency fund can keep you off credit in hard times.

Credit Score: Your credit score is crucial in helping obtain favorable loan terms. Review your credit report for mistakes and if needed work to get your score up.

Setting Clear Goals

Setting clear objectives is crucial to your success in real estate investment. Consider the following:

What Do You Want to Achieve? Define your goals: so that may be passive income, wealth creation, or even early retirement.

Short Term Vs Long Term Goals: Classify between what you want immediately with your future. Short-term goals may be buying your first property and long-term ones would be to accumulate a range of real estate properties.

Education is Key

In fact, it really does come down to power in real estate investing. Here are a few places to educate yourself:

Books: Read books on real estate investing, property management, and market analysis.

Podcasts: There are podcasts where successful investors talk about their experiences and pundits explain their methodologies.

Online courses: Sign up for online courses that explain real estate investing in different aspects.

Mentors: Find other investors, so you can tap into and get advice from as you go through the market.

Assembling Your Team

You will need to develop a solid support system. Consider the following professionals:

Realtor: Look for a good agent who is knowledgeable about the local market and will assist you in finding the right investment property for you.

Lender: Know your financing options and identify a lender that can assist you in reaching your goals.

Legal guidance: Speak with an attorney to make sure you’re making decisions that are informed and within the parameters of local laws.

Accountant: A great accountant can guide you through tax laws and help make the most of your returns.

Property Manager: If renting, a property manager will manage tenant issues and maintenance.

Enticing Strategies On How To Invest In Real Estate For Beginners

Rental Properties (Long-Term)

One of the most popular strategies, even among beginners, is investing in rental properties. Here are some of the important factors to keep in mind:

Residential Properties: You can purchase single-family or multi-family residences. Residential properties experience an unceasing demand as people will always require somewhere to live.

Pros and Cons: Rental properties can offer a reliable income stream, but also involve hands-on management and the costs of upkeep.

Real Estate Investment Trusts (REITs)

REITs offer a way to invest in a portfolio of income-generating properties, without the hassle of managing properties yourself.

Pros and cons: They provide liquidity and diversification, but you may have less control of the properties and their management.

Real Estate Crowdfunding

Crowdfunding platforms (like Fundrise) give you the ability to team up with other investors to fund major real estate developments.

Pros and Cons: This approach creates a lower barrier of entry to the new investor, by potentially relinquishing some control and giving up some liquidity.

House Hacking

House hacking is when you live in one unit of a multi-unit property and rent out the others.

Pros and cons: This approach can save a lot on housing costs, but it might make it harder to find privacy.

How to Find Your First Investment Property Location!

Market Research

Do some in-depth market research and learn about some potential investments that look promising. Consider the following factors:

Population Growth: Find where the population is growing, which can increase demand for housing.

Employment Growth: A strong employment market can result in increased need for rentals and property values.

Median Income: Make sure the average median income is conducive to rental rates.

Neighborhood Analysis

Analyze neighborhoods by different factors:

School Districts: High school districts can have a big impact on property values and who will be drawn to the area.

Crime: Nobody wants to live in a scary neighborhood!

High Property Values: Areas with rising property values is the best play to get the best return on your investment.

Property Analysis

Do an in depth analysis of potential properties:

Cash flow Analysis: Check income against expenses to get positive cash flow.

Cap Rate, ROI, Gross Rent Multiplier: These are a few of the key metrics you need a basic understanding of to be able to gauge the potential of the property.

Property’s Condition: Evaluate the house’s condition and what sort of repairs or refurbishment it calls for.

Networking

Get to know some of the more active local agents and investors seeing what off-market properties they have available. Contacts can share information and opportunities that you won’t find out in public.

Financing Your Real Estate Dreams

Traditional Mortgages

Compare the different types of mortgages.

Conventional Loans: Usually available to borrowers with a higher credit score and down payment, these loans generally have competitive interest rates.

Loans for first-time homebuyers: These are backed by the government and include FHA loans, which require a lower down payment.

VA Loans: These loans for veterans often require no down payment and offer favorable terms.

Hard Money Loans

Hard money loans are short-term, high-interest loans used to make fast deals. They can be helpful for investors who want to buy properties in a short amount of time, but they’re also more expensive.

Private Money Lenders: Loans from people can be more flexible. Just make sure you’ve got some kind of arraignment happening, because we don’t want any insinuations.

Seller Financing: With seller financing, instead of paying a bank, you will make your payments to the seller, who is financing the purchase. This may be a good alternative if you have problems getting traditional loans.

BRRRR Method: The BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) is a formula to grow a portfolio. With this method, you can use your equity to purchase other properties.

How To Manage Your Investment – From tenant selection to property maintenance

Tenant Screening

When you’re a landlord, tenant selection is key to success. Consider the following:

Credit: Check that the tenants have a strong credit rating.

Check for Background: Research tenants’ rental history and criminal history.

Fair Housing Laws: Know what you can, can’t do to prevent discrimination as a landlord.

Lease Agreements

A detailed lease agreement is a must to protect your investment. Key clauses to include:

Term: Term indicate the length of the lease and options to renew it.

Rent Payment Notes: Specify methods of payment and due dates.

Ongoing Maintenance: Include an agreement on who will be responsible for any maintenance tasks.

Rent Collection and Evictions

Create a system for collecting rent, and be familiar with eviction laws. Get to know local laws so that you don’t break any.

Property Maintenance and Repairs

You need to maintain the value of your property. Consider the following:

Scheduled Maintenance: Set up regular check ups so that you avoid expensive repairs.

Repairs: Be ready to solve any unexpected issues rapidly with a well-thought-out emergency-response process.

Hiring a Property Manager (Optional)

If you have multiple properties, or don’t have the time to manage them on your own, consider hiring a property manager. Find someone who is experienced and has a good reputation.

Common Challenges and How to Overcome Them

Vacancy Periods

Empty dwellings affect your cash flow, as well as liberty time. To speed up this process, you can do the following:

Advertise Your Property: List your place online and on social media to find potential tenants.

Provide an Inducement: If possible, offer discounts or inducements to secure tenants faster.

Problematic Tenants: Dealing with them can be a headache. So to mitigate the risks that come with renting, screen your tenants meticulously and set clear leases.

Unexpected Repairs: Unplanned repairs can be hard on your pocketbook. To get ready, keep up a cash reserve for repairs and emergencies.

Market Downturns: Real estate markets can fluctuate. Take the long view and be willing to retain your properties in down markets.

Legal Issues: Seek advice from lawyers on any legal challenges that might arise. A good attorney can help you avoid making costly errors.

Conclusion

So in sum, investing in real estate can be a tremendous generator of wealth and a real way toward financial freedom. So, with some clear levers to work on, you can begin your journey to being a successful investor in real estate by taking control of the path that works best for you with the help of this comprehensive guide. Don’t forget to learn, have clear goals, and form a strong support team.

Call to Action

Begin your real estate experience now! Get our complimentary real estate investment checklist and subscribe to the newsletter for more tips pages and resources!

Frequently Asked Questions

1. How much do you need to start investing in real estate?

The minimal amount to begin real estate investing can differ according to the strategy and geographic location.

But with creative financing, that’s not impossible, you can even start investing in real estate with no money down.

2. Is real estate investment risky?

Real estate investing comes with its risks, like any investment. But with the right knowledge, preparation and risk reduction, you can make the downside as small as possible.

3. How long does it take to make money in real estate?

Returns in real estate take time (how much depends on the strategy and the market it is in). But with a well-considered investment, you can begin to see returns in a matter of months to several years.

4. Do I need a real estate license to invest?

No, you do not need a real estate license to invest in real estate. But a license will give you more access and information.

5. What’s the best kind of property for a beginner?

I find a good type for an beginner will depend on their goals, budget, and local market conditions. But for many investors, single-family homes and small multiunit complexes provide an entry point.

ESG Investing Is Changing for Programmes Aimed at changing American businesses and business practices Nowhere is that change more apparent than in the world of ESG (Environmental, Social and Governance) investing in the United States.

Adopted on July 10, 2025, these regulations are designed to provide transparency and to give investors more consistent and emphasized information on how ESG-focused funds are classified and marketed.

The Push for Greater Transparency

For years, the rapid rise of ESG investing has been dogged by worries of “greenwashing” – where funds are marketed as environmentally or socially responsible while not actually incorporating ESG factors into their investment strategies.

The SEC’s new rules respond to these developments and aim to codify and enhance the disclosures of investment funds that allege to take ESG considerations into account.

At the heart of the new rules is a requirement for enhanced and standardized disclosure on the integration of ESG factors into a fund’s investment process, including the approach to the fund’s investment objectives, strategies and principal risks.

Funds will now have to explain how they define and measure ESG factors, which data sources they use and how they apply this understanding in investment decisions. The aim of such a measure is to enable investors to make better-informed decisions so that their investments truly reflect their sustainability preferences.

Redefining ESG Fund Classifications

One of the most important parts of the new SEC rules is the way it could change how ESG funds are categorised and viewed. The rules put in place more clearly delineatethe various types of ESG funds:

“Integration Funds” are new challenges about how they consider ESG factors vis-à-vis all other material factors in their investment process.

While “ESG-Focused Funds” (those that view ESG as a primary investment strategy) will be subject to more prescriptive guidance, including, where possible, measurable indicators about how such funds are incorporating ESG as part of investment processes. These might be specific environmental metrics (like carbon footprint), social metrics (like diversity statistics), or governance metrics (like board independence).

Impact Funds (i.e., funds that seek to achieve specific, measurable ESG outcomes alongside returns) – whose disclosure obligations should be much stronger (i.e., providing full disclosure of their impact objectives, the methods by which their impacts are measured and periodic updates on actual impact).

Analysts expect this tiered approach to prompt a rethink from many fund managers about their existing ESG claims and perhaps result in some existing funds being reclassified to fit under the stricter definitions. Funds unable to comply with the additional disclosure required for greater ESG categories could avoid making higher ESG claims or work towards deeper ESG integration.

For Investors and Fund Managers

The new rules offer a quantum leap in the clarity and comparability of ESG products, to the benefit of investors. They will be in a stronger position to tell the truly ESG-oriented funds from those that pay mere lip service to ESG. This greater visibility should help increase confidence in the market for ESG investment.

For fund managers, the new standards require a full review of your current ESG policies and procedures, marketing materials and how data is captured internally. Compliance will necessitate significant investment in resources for data management, reporting, and knowledge in ESG analysis.

Though difficult in the short run, it is in the long term likely to lead to truer and stronger ESG integration across the industry, which should help to buttress the credibility and long-term health of ESG investing. The S.E.C.’s action represents a sign of maturity for the E.S.G. market, which has been moving beyond broad claims to deliver impacts that can be measured and held to account.

Chip behemoths NVIDIA and Advanced Micro Devices (AMD) are getting frothy with investor excitement, both seeing record stock prices after soaring Q2 2025 financial results.

The strong numbers highlight ongoing strong demand for their high-performance computing and AI-driven technologies, particularly in the data centre and artificial intelligence markets, which are both seeing strong growth.

NVIDIA’s Reign Of Dominance Carries Over To Record Data Center Revenue

NVIDIA (NASDAQ: NVDA) – the AI-chip leader – crushed its second-quarter fiscal 2025 earnings. The company reported record quarterly revenue of $30.0 billion, representing a huge 122 per cent rise from the same quarter a year ago and a hefty 15 per cent increase from the prior quarter.

That jump was powered largely by its data centre segment, which reported record revenue of $26.3 billion, a 154% increase from a year earlier. CEO Jensen Huang discussing the sustained high demand for NVIDIA’s Hopper architecture and “amazing” enthusiasm for its upcoming Blackwell platform.

He said the world’s datacentres are “doing a full-on refresh of the computing stack with accelerated computing and AI”, with NVIDIA on the edge of that upgrade. It also noted robust adoption of its Spectrum-X Ethernet networking platform for AI and significant scaling of its NVIDIA AI Enterprise software, indicating capabilities as a full-stack platform provider.

NVIDIA’s similar stock run – up 88% from an early-April low and 20% from the beginning of 2025 – has it now briefly pushing past a $4 trillion market cap. Analysts remain bullish, pointing to still strong demand for its GPUs as big tech companies plough ahead on plans to build out AI infrastructure.

AMD’s Strategic Investment in AI and Data Centers Is Paying Off

Well, surprisingly not to be outdone, Advanced Micro Devices (AMD) also had a strong performance for the quarter ended 2Q 2025 – coming out better than what Wall Street was looking for. Although individual Q2 2025 results are usually released in early August (in accordance with their previously announced August 5th schedule), the bullish sentiment is due to robust Q1 results and hopeful forward guidance that shot the stock to all-time high territory.

A big driver has been AMD’s focus on expanding its product portfolio and market presence in AI and data centre technologies. Its data centre small business segment has also enjoyed robust year-over-year growth on the back of the rollout of AMD Instinct AI accelerators and robust sales of its EPYC CPUs. Despite continuing headwinds like export controls in a few markets, AMD has shown that it can win share in key markets.

Investor confidence that the company can execute on its vision, especially given strong customer interest in new products, has returned. AMD’s share price has also enjoyed impressive gains, with the markets clearly buying into its long-term growth trajectory in the cutthroat chip industry.

AI Demand Fuels Semiconductor Boom

That both NVIDIA and AMD are trading at all-time highs is a reminder of the ravenous global hunger for modern semiconductor technology, especially the sort that fuels AI.

As companies around the world spend heavily on generative AI, high-performance computing, and data centre infrastructure, the two powerhouse chip makers are well positioned to capture much of that market and innovate in the years ahead.

This is the continuation of that secular trend I wrote about here and here. (Look, if you haven’t been a believer in semiconductors, you haven’t been paying attention.)

Millions of Americans with student loan debt are poised to receive huge relief after the new Biden administration on Tuesday announced that the Department of Education would significantly expand its debt relief efforts.

With the plan, an estimated 3 million borrowers are expected to see their debt forgiven, extending current programmes and fixing past administrative errors to lay out a clear way for people to attain financial freedom.

Broadening the Reach of Relief

This new release from the Department of Education offers further evidence of a sustained effort to provide relief for the student loan crisis that has affected millions of families.

The revised programme centres on a number of core components, all intended to streamline the forgiveness process and address borrowers who faced barriers or didn’t know they were eligible.

An essential element of this approach is to build on our current systems, such as Income-Driven Repayment (IDR) plans and Public Service Loan Forgiveness (PSLF). The department has taken aggressive action to identify these borrowers and provide relief to them automatically, even though their forgiveness was not automatically granted as a result of errors by the subcontracts.

These are people who have paid for 20 or 25 years, depending on their loan type, and are beginning to see their remaining balances zeroed out.

Addressing Public Service and Hardship

The plan also hits public servants hard. Although the Public Service Loan Forgiveness programme has offered a helping hand to more than a million borrowers, the details of how it was previously run have left many borrowers angry and confused.

This new expansion seeks to simplify the process and make sure that qualifying payments by teachers, nurses, government workers and other public service workers are correctly recorded, driving more rapid forgiveness after 10 years of service.

The administration is also targeting borrowers who are suffering from financial hardship and borrowers who were exploited by predatory institutions.

Although it is still unclear about new categories for “hardship relief”, the aim is to give the Secretary of Education more discretion in cancelling the debt of borrowers with serious financial planning, which makes repayment impracticable.

That includes continuing relief for students whose schools collapsed or engaged in deceptive practices.

The Role of the SAVE Plan

One of the key pillars enabling all of this greater relief is the Saving on a Valuable Education (SAVE) Plan. The SAVE Plan has been challenged in court, and parts of it have been suspended as a result of the litigation, but the administration is implementing other parts of the plan that are not affected by court orders.

The SAVE plan reduces monthly payments substantially for many borrowers as a percentage of their income and the number of people in their family, and for those with lower initial loan balances, it offers forgiveness in as few as 10 years.

The continued work to stand up SAVE, in the midst of a legal fight, is crucial to helping millions of people in repayment manage and ultimately obtain forgiveness.

Effects on Borrowers and the Economy

For the 3 million borrowers affected, this expansion means less financial strain, more take-home pay, and the freedom to work toward other milestones in life, like purchasing a home or saving for retirement.

The action was also expected to have broader economic benefits as it encourages consumer spending while eliminating debt that has been a drag on economic growth. The Biden administration says that these moves are part of an overall strategy to fix a “broken” system of student loans, making good on the promise of higher education as a path to opportunity and not crushing debt.

Although the student loan terrain is not static, this newest plan represents a significant development in relieving those who need it most.

The time has come for new EU laws mandate companies to not only make a business case for sustainability but also to focus on a new campaign for (climate) transparency.

While investors already appreciate the strong correlation between good sustainability performance and good financial planning, the European Union is driving home this point by introducing forceful legislation that compels a more complete and open assessment of companies’ climate exposure.

Starting in 2026, more types of businesses will be mandated to disclose how climate change affects their businesses and the extent to which their operations contribute to climate risks, a huge step forward for corporate climate accountability.

The CSRD is in the Spotlight

This is accounted for by the Corporate Sustainability Reporting Directive (CSRD), which has been effective from January 2024. While the first reports for some large firms date back to financial year 2024 (reports published in 2025), the number grows significantly in number in 2026 (for FY 25) and will include a much larger sample of firms.

That means all big firms (of a certain level of employees, balance sheet, or revenue) operating in the EU. Queensland Listed Small and Medium-sized Enterprises (SMEs) will also report from the 2027 calendar year with a 2-year deferral power.

The ultimate objective of the CSRD is to bring sustainability reporting on par with financial reporting. It requires wide-reaching reporting on environmental, social and governance information (ESG), beyond that which was previously covered by the Non-Financial Reporting Directive (NFRD).

“Double Materiality” and Climate Risks

Central to the CSRD and particularly pertinent in the climate vulnerability context is the notion of “double materiality”. This forces companies to report in two places:

Impact Materiality: The influence of the company’s books and records on the environment/people (e.g., its carbon emissions, pollination).

Materiality for Financial Considerations: The company’s exposure to material financial risks and opportunities for how sustainability issues, such as climate change.

Under this structure, companies are to identify and assess their exposure to different climate risks, namely:

Physical risks: These are the direct effects of climate change, including acute catastrophes like floods, wildfires and extreme heat, as well as more chronic changes like sea-level rise and altered precipitation patterns. Businesses will also have to consider how those could impact their assets, operations and supply chains.

Transition risks: These are related to the move toward a low-carbon economy, including policy changes (e.g., carbon pricing, tighter emissions regulations), technology developments (e.g., outdated high-carbon assets), market forces (e.g., consumer preferences favouring sustainable products) and reputational considerations.

Streamlining Disclosures: European Sustainability Reporting Standards (ESRS) With a proposal to establish an EU non-financial reporting directive written in the sand, a new system is in the makings for mandatory European climate, environmental and social disclosures (ESG, sustainability report). Copyright 2021 Eagle Alpha This report was produced by Eagle Alpha, a data and analytics firm that provides investors early access to market-moving insights.

In order to have a level playing field and a fair comparison, companies under the CSRD should report in accordance with European Sustainability Reporting Standards (ESRS).

Developed by the European Financial Reporting Advisory Group (EFRAG), these’ve detailed standards which provide a comprehensive guidance for reporting on a broad set of ESG topics, with specific requirements for climate-related disclosures (ESRS E1 – Climate Change).

Companies will have to decide their climate transition plans, targets for reducing emissions (including “Scope 3” emissions emanating from their entire value chain) and strategies for building resilience to the physical effects of climate change.

And that will take proactive data collection and scenario analysis, with transparent disclosure of climate-related governance, strategy, risk management and performance metrics.

Driving Transparency and Resilience

The EU New Mandate aims to offer market participants, including investors, consumers, companies, and policymakers, transparent, comparable, and robust indicators to measure companies’ sustainability performance and their resilience to climate risks.

It aims to avoid “greenwashing” and direct investment into genuinely sustainable economic activities while drawing in line with the wider objectives of the European Green Deal and the EU Taxonomy for sustainable finance.

While implementation will require substantial effort and investment from the business community, it should encourage greater responsibility and innovation to adapt to and mitigate the impacts of climate change and help support the construction of a more resilient and sustainable European economy.

The United Arab Emirates (UAE) has been removed from the European Union’s list of problematic states in terms of its financial regime for money laundering and terrorist financing (AML/CFT).

This long-awaited removal, officially approved by the European Parliament on July 10, 2025, is further proof of the strong commitment of the EU toward the UAE’s efforts regarding fighting financial crimes and its adoption of international standards.

A Comprehensive Turnaround

The move follows a year of scrutiny and a raft of reforms carried out by the UAE. The country was originally put on the grey list of the Financial Action Task Force (FATF) in 2022, which subsequently led the EU to place the UAE itself on its list of high-risk states in March 2023. These classifications subjected EU financial institutions working with Emirati entities to higher due diligence levels that made transactions slower, costlier and damaging for reputations.

The UAE reacted strongly and quickly, however. The country undertook a comprehensive revision of its AML/CFT regime under the instructions of leadership.

This included various legislation, new regulations, substantial fines against non-compliant parties, and stepping up enforcement in high-risk sectors, including real estate, gold and precious metals, and corporate services providers.

These proactive initiatives led the FATF to remove the UAE from its grey list in September 2024, noting “significant progress” in several compliance-specific areas.

Tangible Benefits for European Business

For the EU, the decision to delist matters not only symbolically, but also in concrete and practical terms for European businesses and investors. EU banks and companies will also be able to stop carrying out additional due diligence on Emirati clients and transactions.

These cuts in red tape will result in fewer compliance costs, shorter timeframes for the transaction, and improved movement of capital between the jurisdictions. The shift is likely to restore a great deal of market confidence for overseas investors, particularly in banking, fintech and property.

With the move, the profile of the UAE as a secure and transparent place for foreign direct investment will be elevated yet further. This comes as good news for businesses planning to set up in the UAE that are looking at smoother sailing with less red tape to navigate.

Creating Opportunities for More Fulfilling Relationships

Outside of finance, the delisting will also help lift trade negotiations between the EU and the UAE. The UAE’s earlier listing on the high-risk register had complicated discussions about a bilateral free trade agreement.

Its withdrawal leaves more room for extreme conservatives to have a deeper discussion on macro policy, including energy, AI, digital services, raw materials and other strategic sectors, so as to further strengthen economic cooperation and wrapped development.

As Minister Al Sayegh said, “We are thrilled to unlock the full potential that exists between the UAE and the EU as we build toward an even closer constructive relationship, with greater prosperity and collective security for our regions and nations.”

Continued Vigilance

As the UAE marks this major achievement, it has not lost sight of the fact that it will not be easy to uphold a strong AML/CFT framework. The jurisdiction remains steadfast in its ongoing development of its protections to combat the progression of threats, such as those involving virtual assets and multi-jurisdictional money laundering.

This delisting reflects the UAE’s commitment toward safeguarding the global financial system against such risks, as well as demonstrating the country as a secure and dependable partner for international exchanges.

New York – What does it take to reach the lofty goal of feeling “financially comfortable”? That elusive figure varies widely by generation, the survey found, with Millennials saying they’ll need an impressive $847,000 to feel secure. This figure is higher than the national average and exposes the differing financial hopes and circumstances of varying generations.

The most recent Charles Schwab Modern Wealth Survey 2025 (published July 9, 2025) makes that generation gap plain, detailing the net worth each group thinks is needed to feel financially secure. The average American now estimates it takes $839,000 to be financially comfortable, more than the $778,000 of last year.

Millennials Leading the Pack

For the most part, Millennials (29 to 44 years old, in this case) are looking for the highest comfort level. Their request for $847,000 is symbolic of a generation wrestling with such seismic economic forces as student loan debt, escalating housing costs and inflationary pressures, all while also carving out their own paths in the workplace and at home.

Their own journeys into work in the aftermath of the financial meltdown of 2008 may also give them a different sense of how much capital it takes to achieve security.

Gen Z: Lower Threshold, More Positive

And Gen Z (ages 21-28) has set the leanest bar for financial comfort, saying they need $329,000. Gen Z may be dealing with their own economic issues – however, there’s a lot of optimism coursing through this generation.

43 per cent of Gen Z and 42 per cent of Millennials think they will become wealthy (or already are), at rates far higher than other generations. In addition, this younger generation is more likely to have written down their financial plans, suggesting that they approach financial wellness more consciously even though they are less comfortable.

n X and Boomers: Different Needs, Greater Averages

Generation X, also known as the sandwich generation because many in that age group support children and ageing parents, says it needs $783,000 to feel financially well. This number is a bit lower than the national average, but 2 million people is still a tonne of people.

And Baby Boomers (ages 61-77), most of whom are approaching or are in retirement, believe that they need surprisingly the highest amount among all generations to feel comfortable: $943,000. They do this because they want to ensure they live a financially comfortable retirement in the face of spiralling medical costs and longer lives.

Beyond the Numbers: Defining Wealth

The survey also looked at what Americans think is “wealthy” and found it to be much more than a number. No comment about your physical or mental health or personal relationships: Unfortunately, while the average net worth to feel “wealthy” is $2.3 million by 2025 (or so think the survey-takers), they also place just as much weight on happiness (45%), physical health (37%), mental health (32%), and strong personal relationships!

The changing definitions of financial comfort from generation to generation illustrate how economic security is anything but static in a shifting world. The actual numbers might be different, but the need to be secure in one’s position and to be able to live without constant financial anxiety is universal.

Washington, D.C. The World Bank’s Global Economic Prospects report predicts that this year will see the world economy slow to its weakest level since the 2008 financial crisis, but that a global recession can be prevented if rising trade disputes are settled.

Released on June 10, 2025, the sobering outlook points to widespread economic downgrades and a dire outlook for the remainder of the decade, particularly for developing economies.

A Decade of Reduced Development

Worldwide growth is poised to decelerate to 2.3 per cent by 2025, a shade higher than half a point below its original forecast at the end of last year. It is not being predicted that there will be a full-blown global recession – but if forecasts prove accurate for the next two years.

The average global expansion in the first seven of the 2020s would be slower than in any decade since the 1960s. This extended period of sluggish growth implies that headwinds for global economic dynamism remain entrenched.

Causes of the Recession

Elevated trade tensions and policy uncertainty are the main factors in the gloomy sentiment. The report indirectly points to an increase in trade barriers – such as tariffs – that have increased costs and prompted retaliatory steps around the world.

It’s holding back investment and demand for capital goods, which account for over a quarter of aggregate demand. There are other issues beyond trade, including tighter labour markets driving inflation and a slowdown in global trade volumes, at work, too. Investment growth, meanwhile, has also decelerated despite record high levels of global debt.

Impact on Developing Economies

The slowing is especially troubling for emerging economies. Average annual growth within these countries has steadily ratcheted down over the past three decades, from north of 6% in the 2000s to below 4% in the 2020s.

This trend reflects the fall in world trade. The report forecasts a deceleration this year in almost 60% of all developing economies; their rate of growth is unlikely to exceed 3.8% in 2025. This is more than a percentage point lower than the decade average. Slower growth mechanically undermines the ability of these countries to generate job creation, extreme poverty reduction and per capita income convergence with the advanced world.

Average per capita income in developing countries is expected to grow by 2.9% in 2025 – 1.1 percentage points lower than the average of the twenty-first years of the century. But the World Bank cautioned that to the extent that developing economies (excluding China) grow at a projected 4% GDP rate in 2027, these and other countries would need another 20 years to recover their pre-pandemic growth trajectory.

Path Forward: Cooperation and Reform

The World Bank is calling on policymakers to act decisively to help to combat these risks. Wrapping up current trade disputes, for example, by cutting tariffs to half of their level in May 2025, would raise global GDP by an average of 0.2 percentage points in 2025 and 2026. The report urges renewed progress on integration with partners, further pro-growth reforms and strengthening fiscal resilience.

“Dialogue between the major economies could lead to a more stable and prosperous path for the world economy”, said World Bank Group Chief Economist Indermit Gill, who added that a cooperative workout is necessary more than ever, and the world urgently needs to cut down on trade barriers and policy ambiguity.

“For the developing countries, the report recommends that investment and trade links should be fostered, diversified trade should be sought and domestic revenues mobilised and customised to spend more on vulnerable households.

The message is both stark: the challenges are immense – but collective action and reforms that are strategic can still help guide the world economy to a more resilient and equitable future.

ROME, Italy – Agrifood systems are the basis of global workers, currently providing employment for about 40% of the population. The result is an estimated 1.2 billion young people who will enter the workforce in the next decade and a growing consensus of the critical need for greater and smarter investment in these systems.

That was the loud and clear cry from the 13th edition of the annual FAO Investment Days 2025, a two-day forum from 9 to 10 July on the theme “Investing for More and Better Agrifood Jobs”. The event underscored the great potential of agrifood systems to help meet the rising challenge of youth employment and to drive sustainable development globally.

Why FAO Investment Days 2025?

Organized within the frame of the FAO Investment Days 2025, the Summit was an essential platform that congregated stakeholders from different backgrounds: forward-looking minds, successful entrepreneurs, innovators engaged in production and both public and private investors from all over the world.

They had a common objective: to jointly reflect around specific trajectories and proposals for action so as to transform agrifood systems into solid drivers of inclusive growth and decent work. The forum provided a forum for rich discussion, shared experiences and exchanged best practices on how investing now can change the future for rural and urban young people.

Key Focus Areas and Themes

Deep-dive discussions during FAO Investment Days 2025 did just that, examining the complex landscape of agrifood employment in developing countries. Themes discussed included the critical role of productivity growth from technology utilization and environmentally sustainable activities; the implications of demographic change for labour supply and demand; and the dynamics of labour migration within and between borders.

Access to finance for smallholder farmers and agribusinesses, especially for youth-led projects, was a common theme, as was the changing skills requirement amid rapid technology improvements. Participants also considered supportive policies and enabling environments, such as strong legal protection and streamlined regulation, as actively promoting job creation and innovation.

An important thrust was to promote local value addition and enterprise development through agrifood value chains, which have great potential for providing decent employment, particularly for youth.

Statements from Key Figures

“The distance between the youth labour market and the constraints it faces in the job market is simply alarming,” said FAO Director-General QU Dongyu, adding that “we need to think bigger and deeper” to reactivate the “we reach time urgent” to reach the youth labour market.

He pointed out the FAO remained committed to linking agricultural producers, rural entrepreneurs and agribusinesses with the financing and markets they need to build resilience in fragile communities and foster sustainable growth.

Relevant FAO Work and Reports

Key attention was also brought to the lasting commemoration of FAO’s commitment to investing in agrifood systems during the event. The FAO Investment Centre has a proven track record and is celebrating 60 years of successful operations.

Last year alone, the Centre supported the development of 51 public investment projects across 36 countries, worth a total of $7.3 billion, and ongoing projects worth more than $49.5 billion. One recent significant FAO report, “The State of Youth in Agrifood Systems”, offered a stark context for the talks.

The report exposed that 44% of working youths globally are working in agrifood systems. It pointed out that more than 20% of the world’s 1.3 billion young people (15-24) are currently classified as not in employment, training or education (NEET), and that young women are twice as likely to be NEET in comparison to young men.

The report’s conclusions estimate the creation of only some 400mn new jobs in all sectors over the coming ten years, a figure that pales in comparison to the swelling number of young people who will soon need a job. This wide chasm sounds the call to interventions. Most significantly, the report indicates that with smart interventions, agrifood systems alone could generate 87 million new jobs.

Potential Impact and Forward-Looking Statement

As Investment Days 2025 came to an end, the message of investment strategies and inclusive action rang true among the participants. The forum confirmed (once more) that the transformation of our agrifood systems is not only an economic must but a profound societal imperative.

In doing so, we pave the way to a future that is more food secure, more resilient, and more prosperous for all.” “Through building sustainable growth, boosting productivity and working to provide more and better jobs to the increasing population of young people, we can leave behind a more food-secure and more prosperous future for everyone.

The commitment offered today shows the world’s determination to unlock the great potential of agrifood systems to respond to very real job opportunities and make the world a place where every young person can find their place.