Loan underwriting has been a manual, time-consuming process for decades. With paper documents and statements in hand, humans who knew little to nothing about the person borrowing or from where they were borrowing it determined who could borrow money and who couldn’t.

Although this technique worked, it was slow, subject to cumbersome human bias and constrained by the amount of data any individual could review. Today, a new era has dawned. In short, underwriting is most definitely an arena in which artificial intelligence (AI) is making a splash in financial services.

Techniques like machine learning, predictive analytics or better data processing are basically making this faster but also more accurate and much more fair.

In this article, we consider how AI is changing underwriting and help you to get a better understanding of modern underwriting through the use of some examples with reference to risk assessment, fraud detection, and its role in an inclusive financial system, among others.

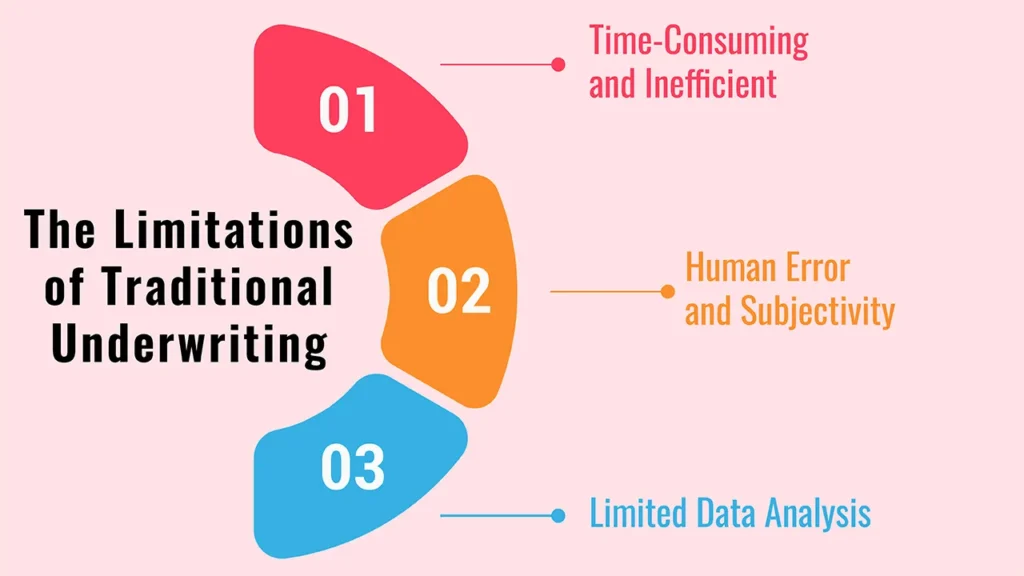

The Limitations of Traditional Underwriting

Before we could truly understand the effect that AI would have, however, we should probably consider some of the struggles with the old system. Traditional manual underwriting was painstaking and came with an array of restrictions.

1. Time-Consuming and Inefficient

Documents, rounds of credit reports and income statements could take days, if not weeks, to manually review. Well, this long-winded process meant frustrated customers through bottlenecks and inflated operational costs for lenders.

2. Human Error and Subjectivity

Even the most careful human underwriters can err. They may also be based on unconscious bias or your own opinion and can lead to inconsistent decisions. This subjectivity could have a chilling effect on otherwise creditworthy borrowers.

3. Limited Data Analysis

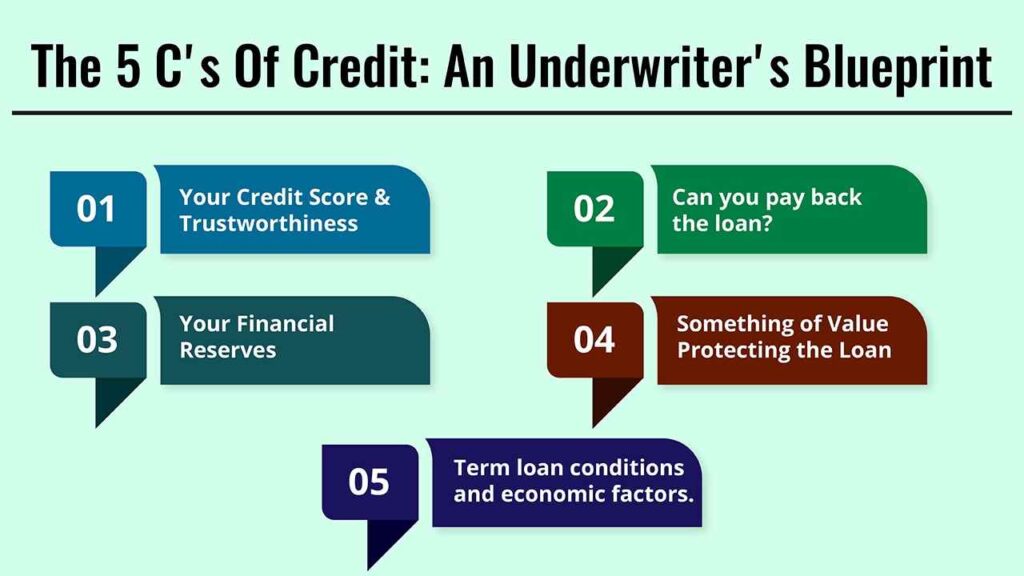

Traditional underwriting has been largely based on historical data, or the “5 C’s of Credit”. It often doesn’t take into account a borrower’s full financial planning, such as those with thin credit files or alternative income streams.

The Underwriting Process Reimagined With AI

AI is not replacing the underwriter entirely but offering him a powerful new set of tools. AI helps underwriters focus on the most complex and nuanced cases by automating routine tasks & delivering deeper insights.

1. Automating Data Extraction and Document Processing

It can rapidly consume and process huge pools of structured as well as unstructured information. AI-powered systems AI — Through Natural Language Processing (NLP), a rundown of documents like pay stubs, tax returns and bank statements may be done within seconds.

It automates hours of manual data entry, reduces processing times easily by 10%, and minimises human errors.

2. Risk-based Assessment and Predictive Analytics

Credit scoring, Yes, but AI algorithms do so much more than that. Thousands of data points, from both traditional and alternative sources such as rent payments, utility bills and cash flow patterns, can be analysed to create a more holistic view of a borrower’s credit profile.

Predictive analytics enable the AI to predict what a credit RS negative indicator might look like in the future, which provides a more accurate risk assessment for lenders.

3. Superior Fraud Detection

AI fraud detection is a powerful detection tool that cannot be substituted. Through millions of past applications, machine learning models can simply notice oddities, inconsistencies, and trends that hint at fraud.

It may be fake documentation or someone stealing your identity. Because of AI’s capability to observe these patterns in real time, it could help lenders identify fraudulent applications before they lead to financial losses.

4. Improved Fairness and Financial Inclusion

One of the most hopeful aspects is how AI can reduce bias. If biased and varied data must be kept far away from training AI (and of course, it has to be trained in accordance with ethical norms), then the solution becomes ideal because it allows for uniform standards based only on financial data, where AI can make a steady, calculated choice.

That in turn can increase access to credit for under-served populations, which may include freelancers or the small-time entrepreneur.

The Benefits of AI for Lenders and Borrowers

Introducing AI enhances underwriting and benefit provisions for all stakeholders.

- And for lenders: quicker decisions, lower operational costs, decreased risk of loan defaults and having a stronger competitive position in the market.

- Borrowers: A smoother, more transparent application process, quicker approval turnaround times, targeted loan offers and a higher likelihood of fair and unbiased decision-making.

Challenges and Ethical Considerations

These benefits are undeniably appealing, but, as it usually is with everything else, the adoption of AI in underwriting comes with its own set of hurdles:

1. Algorithmic Bias

When an AI model is trained on historical data, if such data contains implicit biases, this can be carried to the AI and even enhanced in some ways.

2. Data Privacy and Security

This raises important questions of data privacy and security, as well as consent issues if vast ranges of very diverse data types are used.

3. The “Black Box” Problem

Explainability: at times the decision-making algorithms or models are so complex that it will be difficult to explain it, for a loan in specific, why this was approved and that was denied. This lack of transparency can damage consumer confidence.

4. Regulatory Compliance

The finance sector is already highly regulated. With AI booming, regulators are trying to formulate new regulations to ensure fairness and transparency, not to mention accountability.

The Conclusion: Lending Goes Collaborative

AI is reshaping the world of loan underwriting, and it means that in future, those using it will be able to size up people more quickly, with fewer errors and on more equal terms. This creates efficiency for both financial institutions — which are able to reduce risk and operational back-and-forth costs — and for the borrowers, who have an improved, smoother way of getting a loan.

This is not about replacing the human underwriter but enabling them with an X-ray machine that allows them to make a more thoughtful and fair decision.

Frequently Asked Questions

1. Are AI-based loan officers replacing my loan officer?

No, not entirely. AI was built to streamline all of the manual, data-heavy processes and allow loan officers to focus on nuanced cases where they can provide specialised guidance and build more personal relationships with their clients. While decision-making and customer service still require the human touch.

2. How does AI use my data?

AI Drives Risk Profile Completion with Your Data It may lawfully process data, including structured data (provided from credit reports and income), as well as alternative datasets (with your consent), in making this assessment.

It is a very regulated process, and your data is protected by privacy laws.

3. What is ‘alternative data’, and how does AI use it?

Alternative data are financial information not typically found in a credit report. That may mean your rental payment history, utility bills and savings habits. If you have a limited or “thin” credit file, AI can analyse this data to help determine your creditworthiness.