Financial Planning for Special Needs Families (2025) is an important part of making sure that loved ones who need ongoing care and protection continue to receive the help they will need down the future.

Special families needing planning have unique financial problems, including but not limited to the cost of health care and trying to keep their loved ones eligible for government benefits as they work toward a secure financial future.

This is an article that introduces some of the most important aspects of financial planning that all families with a special needs member need, and it provides specific examples of what can be done now and over the long term in order to maintain stability today while we all also plan for a stronger future.

Essential Considerations for a Special Needs Family Financial Plan:

Financial planning is the process of setting, planning for, and achieving (if not exceeding) all goals or objectives involving money. For families with special needs, the process is not only about traditional planning goals but also about unique tools and protections.

1. Emergency Fund and Cash Flow Planning

Having an emergency fund that can cover 6-12 months of living expenses is also key in dealing with unforeseen expenses, such as a medical emergency or caregiving.

Knowing what income and expenses are now, and what they’re expected to be in the future, can provide a clearer picture of monthly cash flow—ultimately enabling educated budgeting and saving plans.

2. Special Needs Trusts (SNTs)

A special needs trust is a traditional financial planning foundation. They support the special needs person while protecting any assets from counting against him or her for purposes of qualifying for government aid (such as Medicaid and Supplemental Security Income (SSI)).

Trusts: You may have a first-party trust that is funded with your own assets, a third-party trust funded by family members, or a pooled trust where the resources of many individuals with disabilities are combined for investment purposes.

3. Government Benefits and Eligibility

Government benefits are a lifesaver, but families must strategize creatively to avoid disqualification. Programs like SSI and Medicaid are “asset tested,” so financial planning is about how assets should be saved, or held, in order to not threaten benefits. Registering for disability systems and applying for deductions in the terms are good financial decisions.

4. Insurance Coverage

Adequate insurance protections are essential. Medical and therapeutic treatments are covered by full health insurance. Life insurance policies, including specialized ones such as second-to-die policies, are another way to provide financial support after the caregivers have passed by titling them into trusts.

Disability insurance and long-term care insurance are in tune with the general risk management concept.

5. Long-Term Care and Guardianship Planning

Care continuity must be considered in the planning beyond the life of the parents. Creating legal guardians, support/supported decision-making, and trusts to provide for the care of a special needs family member.

A “Continuity of Care” plan that records daily routines and medical requirements can enable future caregivers to offer continuous support.

6. Savings and Investment Accounts

Tax-advantaged saving plans such as accounts allow families to save for disability-related expenses without compromising eligibility for benefits. Families should be careful not to directly title savings after the person with special needs, as that could jeopardize government support.

7. Professional Support

Working with financial planners versed in special needs can make it easier to navigate the complicated planning process. These experts help with trust establishment, benefit maximization, investment strategy and legal organization.

Financial Planning Tools for Special Needs Families

Planning Tool

What It Does

Reasons to Incorporate

Emergency Fund

Covers unexpected expenses

Provides a financial cushion for emergencies

Special Needs Trust (SNT)

Holds assets for the beneficiary without impacting benefit eligibility

Protects assets and retains public benefits

Government Benefits (SSI, Medicaid, tax deductions)

Income, healthcare and tax relief

Provides income, health care coverage, or tax relief

Health & Life Insurance

Long-term medical support and medical life insurance

Protects against high medical costs

Funds 529 ABLE Savings Accounts

Tax-advantaged savings account for disability-related expenses

Funds used in trust care without compromising government benefits

Guardianship & Legal Planning

Ensures proper decision-making for the child

Ensures that your child is properly taken care of

Final Words

It’s not as easy for financial planning for special needs families. It requires a series of careful steps, specialized knowledge, and ongoing commitment.

Through creating a system of financial resources that includes trusts, benefits, insurance, savings and legal protections, families can provide the means to help their loved ones achieve a meaningful and fulfilling life long after they are gone.

Early action and professional advice can help bring peace of mind, as well as financial resilience in 2025 and beyond.

This whole child strategy provides special needs families with the tools to address issues head-on, while concurrently pursuing and achieving opportunities.

Frequently Asked Questions:

1. What’s the one financial instrument that is more important for families with special needs?

There are several, but when preparing for a disabled person, the most important is the Special Needs Trust (SNT), as it shields the inheritee’s assets and does not risk loss of government benefits.

2. How much emergency fund needs to be in place for a special needs family?

It is best to have between 6 and 12 months of living expenses in an emergency fund in order to be able to handle unexpected costs.

3. Can you wrap government benefits with annuity income?

There are ways that families can save and invest without jeopardizing their benefits by planning ahead, like utilizing Special Needs Trusts or ABLE accounts.

4. When does special needs financial planning begin?

It would be ideal to start planning as soon as one can, even shortly after diagnosis, in order to take advantage of different programs and financial solutions.

5. Do I need to work with a professional to help me develop my financial game plan when someone in my family has special needs?

Absolutely, working with special needs planning advisors can help navigate multi-faceted legal and financial terrain and provide broader coverage.

In 2025, Finance reimagined Financial planning and analysis is the driver of modern business strategy, and leading organizations are looking up where to be so they can rewrite their future. With increased competition and changing markets, companies require strong mechanisms for understanding of their finances, planning for the future and taking important decision.

This article applies real-world examples to shed light on what financial planning and analysis 2025 is in real life and how its top priorities are being done in the present with sets of processes, tools, and evolving value.

Financial Planning and Analysis 2025 Definition

Financial planning and analysis 2025 Financial planning and analysis 2025 is a title for a set of processes that enable the Office of Finance to, Plan, Analyze, and Monitor its performance over time. This practice involves budgeting, forecasting, financial modeling and strategic planning as it pertains to the company’s financial health and to inform significant business decisions.

In contrast to old school accounting, which is predominantly about recording what has already occurred, financial planning and analysis 2025 is about the future. It leverages data-driven intelligence to predict market shifts, allocate resources, and point the organization in the right direction.

The Core Components and Processes

Contemporary enterprises depend on a handful of consolidated functions within the financial planning and analysis (FP&A) 2025:

Budgeting: The detailed planning of how resources will be allocated over a period of time.

Forecasting: Estimating future revenues, costs and other financial metrics based on historical trends and market conditions.

Scenario Analysis: Looking at the business implications of various economic or industry conditions.

Performance Monitoring: Observing to what extent the actual results for a specific project, program, or organizational line/comparison deviate from the budgets and forecasts as one step to recognize gaps and potentials.

It is these components that financial planning and analysis 2025 enables leaders to answer critical questions by asking whether to invest in new projects, expand geographically or change pricing strategies.

The Role of Strategy in Contemporary Organizations

In today’s highly volatile business environment and analysis 2025 is essential. By this role connects the boots on the ground work and the big picture thinking. It enables decision making based on true intelligence through leadership.

For example, CFOs and finance teams rely on financial planning and analysis 2025 to assess the implications of mergers and acquisitions, to assess the impact of market changes, and to analyze the finances behind long-term investments.

By having oversight into the entirety of the company’s finances and operations, the financial planning and analysis team can serve as a liaison to the business for all functions — enabling better alignment, more nimble decisions, and a joint focus on strategic opportunity.

The Evolution of Financial Planning and Analysis 2025

A new field is born in 2025 One of the fields which has advanced most under the influence of technological development, data analysis and shifting business needs is the field of practices, and the banking game in particular.

Cloud Financial Systems, Real-Time Data Dashboards, and Advanced Analytics have made financial planning and analysis 2025 more efficient and accurate and insightful than ever.

Key changes include:

Automation Time consuming activities such as data merging have been automated, allowing the analysts to focus on more value add work.

Integration FP&A solutions much more integrated than in the past, with the ability to bring in operational, financial and market data, providing a fuller view.

Scenario modeling Sophisticated tools for scenario analysis are available for businesses to see how a market shock, regulatory change or supply chain disruption could affect them.

The answer: Collaboration: Contemporary systems are designed to facilitate cross departmental collaboration ensuring the entire business organization enjoys the benefits of agile, integrated planning.

The Necessary Levels of Financial Planning and Analysis (FPA 2.0) 2025

FP&A professionals 2025 are technically savvy and strategically oriented. They must master:

Analytical skills (understanding financial and operating metrics)

Communication (communicating what findings mean to non-financial audiences)

c/Technical-competence (knowledge and use of modern planning tools and analytics)

Problem-solving (creative thinking to approaching forecasting and budgeting issues)

Delivery partnership (partnering with management and other teams to align resources and strategy).

Practical Benefits for Organizations

Findings Companies that were ahead in their financial planning and analysis 2025 investing into robust financial planning and analysis 2025 capabilities enjoy several advantages:

Informed Decision-Making: The leadership receives clear info to help make complicated decisions.

Resilience: Companies can quickly respond to changes in the market or regulatory environment with accurate forecast and scenario planning.

Resource efficiency: Capital and labor are invested in the most valuable projects.

Sustainability to profitability: Powerful analysis uncovers cost saving opportunities and revenue generating potential.

Investor Trust: When investors and stakeholder see clear evidence of sound financial planning, they have confidence that your firm is highly reputable.

The Future of FP&A in 2025

Organizations face the challenges of a world shaped by widespread economic uncertainty, climate pressures, and digital disruption, and as these new global realities take hold, financial planning and analysis (FP&A) 2025 is responding. Coming years will see more developments:

Broader deployment of artificial intelligence to create more predictive forecasting models to give managers earlier warnings about threats or opportunities.

Integration with wider sources of data for forecasting, such as external market movements, social sentiment and geopolitical occurrences.

More attention to sustainability and ESG (environmental, social and governance) metrics in financial planning.

Businesses that adopt these are likely to experience more agility, better strategic focus and greater long-term success.

Acts to be taken towards Financial Planning and Analysis 2025

For companies wanting to improve an existing or establish a successful financial planning and analysis 2025 model, they should focus on these steps:

Establish Clear Goals: Know the financial visibility and strategic results the company hopes to gain.

Create Cross-Functional Teams: Make sure you involve finance, operations, sales, and marketing for a 360 view.

Invest in Technology: Invest in a strong FP&A software solution that can automate, analyze and collaborate.

Create Standardized Practices: Make sure that you have repeatable processes for budgeting, forecasting and reporting.

Train Employees Non-Stop: Employees need to be the latest and greatest with the tools, regulations, and analytics.

Watch and Tweak: Constantly re-check results, fine-tune artificial models, and adapt procedures when the environment shifts.

Actual Example: Financial Planning and Analysis 2025 in Practice

As the year 2025 unfolds, a major global retail organization is grappling with market velocity and uncertain consumer demand. Through financial planning and analysis 2025, its finance team constantly gathers sales and expense data from a broad range of regions, and directs automated forecasts to identify changes in demand sooner.

When a major supplier experiences a disruption, scenario analysis uncovers the extent of the financial damage to supply chains, and margins. The management are quick to react, shuffling resources and modifying pastoral plans to turn a profit, and forestall any damning losses.

That kind of agility available to companies only when financ ial planning and analysis 2025 becomes integral to the heart of business management shows the way for other organizations to move from surviving to thriving as they go forward.

Final Words

FP&A 2025 As we move forward, financial planning and analysis is not just a key finance function – it is a critical competitive driver and crucial contributor of long-term success.

Instituting financial planning and analysis 2025 as the epicenter of strategic planning enables companies to be better equipped to respond to the anticipated as well as the unanticipated, paving the way for smarter, healthier financial outlooks.

Frequently Asked Questions

1. Difference between old vs. new accounting and financial planning and analysis 2025?

The traditional accounting is primarily concerned with the recording of past transactions and events, the preparation of financial statements on the basis of that data and regulatory concerns.

FP&A 2025 is anticipatory and strategic, focused on predicting future performance, planning around the allocation of resources, and driving business decisions.

Why FP&A 2025 matters to organisations?

Make smarter decisions, faster financial planning and analysis 2025 helps business leaders make the right decisions for the future of the business, by delivering secure, consistent, and accurate information.

It opens the door for organizations to react more easily to changes in market conditions and regulations, while driving resilience and long-term growth.

What are, in 2025, the technology trends that are affecting financial planning and analysis?

Technology is helping to modernize financial planning & analysis 2025 – faster, smarter, more collaborative.

Key trends involve use of cloud-based financial software, streamlining of manual tasks, increased use of advanced data analytics, real-time dashboards and integration of scenario planning tools.

In every marriage or long-term partnership, there are two vital components — love and partnership. However, money remains one of the most frequent causes of stress in a couple. It’s difficult enough to manage your money as an individual, let alone as a couple.

Couples’ financial planning is not only about making a budget — it’s about building a shared vision. It includes getting to know the individual money habits of both partners, identifying shared financial goals and becoming skilled at handling joint income, savings, debts and investments.

This article describes the basic principles of financial planning as a couple, practical approaches to managing combined and separate monies, and how to do so with clarity in order to work together, along with strategies to realise future goals.

Here are the 10 Steps for Financial Planning for Couples

STEP 1: Talk Money Early

And all of that is built on the foundation of honest conversation about money as a couple. People’s financial backgrounds, habits and feelings about money vary. One person may be a saver, while the other is a spender. You might put a priority on investments, while I choose the safety of cash savings.

Reminder: There’s nothing wrong with either of these perspectives, but they must sync up. Money topics make trust when they’re broached openly: income, financial goals, even fears.

How to do this effectively:

Plan on having regular money talks (monthly or quarterly).

Share income details transparently.

Talk about both long-term dreams (buying a house, early retirement) and short-term wants (holidays, bills).

Establish some boundaries to prevent confusion about where you draw the line on certain things — such as how much you can spend personally without checking in with each other.

Step 2: Choose Financial Management Approaches

When it comes to handling money, most couples fall into one of three categories:

100% Joint: With this method, all income is deposited into one account, and all expenses are paid from one shared account. This method encourages complete transparency.

Completely Independent: Everyone pays for their own expenses with their own income, except for joint bills, for which contributions are agreed upon in advance. This works for couples who value keeping things separate or have wide disparities in income.

Hybrid Approach: Combines both, A portion of the incomes get put into a joint account that is used for shared expenses (rent, bills, groceries, etc.), and the remaining amount is kept as individual funds for personal use.

Best practice: The hybrid model makes sense for a lot of couples: enough teamwork but also enough freedom on our own.

Step 3: Build a Joint Budget

Tracking where money goes is key to budgeting because it prevents couples from being surprised by large expenditures. Developing a joint budget doesn’t mean micromanaging every purchase — it means setting realistic limits.

How to create a budget as a couple:

Include all sources of income together (shuffled salaries or freelance work, investments, etc.).

List out all recurring expenses (rent, utilities, groceries, insurance).

Create financial goals (travel fund, down payment on a home, emergency savings).

Divide money between needs and wants.

And leave each other room to spend a little money in their own ways, or you may start resenting others.

A mutual budget shouldn’t be a whip; it should be a guideline. In the long run, it helps couples get their spending habits in line with what they actually care about.

Step 4: Manage Debts Together

Debt is a tricky thing in relationships, especially if one partner has a large amount of student loans, credit card debt, car payments, etc. Unspoken indebtedness can become problematic in later years, so it’s best to put it all right out there.

Strategies for handling debt:

Be transparent about existing debts and credit scores.

Choose to retire debt as individuals or together.

Establish a timetable for making payments that is manageable for both of you.

Steer clear of unnecessary new debts unless they benefit both partners (a mortgage, for example).

Taking on debt as a team removes the cloak of secrecy and enables couples to concentrate on achieving mutual financial freedom.

Step 5: Create an Emergency Fund

An emergency fund is critical for everyone, but especially for couples. Life’s uncertainties — job loss, medical problems, car troubles — can threaten a relationship when there is no financial buffer.

Rule of thumb: Keep three to six months of essential expenses in an easy-access savings account.

Couples should agree on:

Where is this money to be kept?

Contributions each will make.

When to use it (only in the case of true emergencies).

This amount brings peace of mind and makes it so that you’re not knocked off track in the event of an emergency.

Step 6: Save and Invest for Long-Term Goals

Long-term dreams One of the more rewarding parts of financial planning for couples is working on long-term dreams together. These could be purchasing a home, raising kids, travelling or amassing wealth for retirement.

How to approach long-term planning:

Determine common goals: Document values, such as home ownership or college for children, or early retirement.

Establish deadlines: Determine how quickly you want to nail those goals.

Choose appropriate investments:

Real estate for property goals.

Retirement tax assets (pensions, IRAs or PF).

Mutual funds or index funds to grow your wealth.

Section 529 plans (qualified tuition plans) for children, if applicable.

All investments should be vetted and approved by both parties. Even for an account handler, both parties need to be aware of where money is headed.

Step 7: Retire Together Plan out your retirement as a couple.

Planning for retirement is a joint effort and will affect each person’s and, eventually, each couple’s long-term lifestyle. Couples should ask:

When do we want to retire?

Where do we want to live?

Where will your income come from to sustain you?

Options include:

Pension or retirement accounts.

A rental property for passive revenue.

Diversified investments for long-term growth.

The earlier the better, so growth can compound and one partner won’t be carrying an outsized burden in the later years.

Step 8: Insure Each Other From Your Crap

Insurance is one of the most neglected aspects of a couple’s financial planning. It serves as a cushion in the case of unforeseen financial hardship.

Types to consider:

Health insurance for medical costs.

Life insurance to ensure the surviving partner is covered if the couple is separated by loss.

Insurance for joint assets, as property or renter’s insurance.

Review policies side by side each year to ensure coverage aligns with your changing life.

Step 9: Establish or Update Estate Planning Documents

Estate planning prevents financial insecurity after the tragic doomsday cracked earth event. It’s an awkward topic to talk about, but we’ve got to talk about it.

Steps:

A will can determine how assets will be divided.

Designate recipients for accounts and insurance.

You could look into a power of attorney that would enable you to make decisions in emergencies.

This measure avoids power struggles and respects both partners’ will.

Step 10: Plan Financial “Check-Ups” Now and Again

Relationships and finances are dynamic. Moving up in the company, having children or making lifestyle changes can affect financial aspirations. That’s why regular money check-ups are so important.

Best practice: Have quarterly financial reviews as a couple, updating budgets, monitoring investments and realigning on goals. They don’t need to be hard sessions — they could be as simple as including dinner in the process.

Conclusion: Building Financial Unity

Financial planning as a couple is about Team You, not just managing money but managing life together. By talking, sharing the same goals, creating an emergency plan, and investing wisely, couples can curtail money stress and get back to building dreams.

Challenges are a part of every relationship, but a strong financial plan can also provide couples with stability and freedom — the ability to face unknowns together and slowly work toward collective visions.

It’s not just about responsibility but a testament of love, partnership and future-forward vision together.

Frequently Asked Questions

1. How can couples begin to talk about money without fighting?

The secret to peaceful money talks are openness, respect and timing. Choose a peaceful moment to talk finances as a couple; don’t listen with your finger ready to point in judgement, and make common goals instead of seeking individual faults in one another.

Establishing a regular practice of talking about money and creating a safe space for honesty diminishes the drama and deepens trust over time.

2. Is it better for couples to have joint or separate bank accounts?

There’s no one answer that fits all. Some couples like the convenience of joint accounts for paying bills and managing a budget, while others find it more convenient to have separate accounts and pay for things independently.

Plus, many choose a hybrid approach that includes joint accounts for bills and personal accounts for discretionary spending. It all comes down to communication, lifestyle and financial compatibility.

3. How can couples strike a balance between saving for the future and enjoying life today?

The best financial planning combines long-term goals with the need to enjoy your life now. There is potential for a couple to save and invest some earnings while still budgeting for leisure and getting fun money.

Submit realistic budgets, agree on “fun money”, and revisit goals regularly so saving feels like a long-term win, not a present-day sacrifice.”

When you get a new credit card, one of the first things you notice is the credit limit. This figure is also the most you can borrow on the particular card. It may sound like just a number, but your credit limit is also a powerful force and an increasingly important component of your financial life. It is a direct reflection of a lender’s confidence in your capacity to repay debt, and it helps determine your overall credit health.

Knowing how your credit limit is calculated, what it means for your financial life and how you can work to raise it sooner rather than later, is a life skill for anyone who’s building a solid financial foundation. This ultimate guide to both topics will give you all the understanding and practical steps you need to make your credit limit a tool to work with rather than against.

What Is a Credit Limit?

To put it simply, a credit limit is the most you can borrow on a credit card, line of credit or other revolving credit account. When you swipe your card, you reduce the available credit, and when you make the payment, all or some of that available credit is added back, up to the credit limit.

For instance, if you have a credit card with a $5,000 credit limit and make a $500 purchase, you would now have $4,500 available credit. Once you have paid off the $500 balance, you will again have $5,000 of available credit. It’s a flexible borrowing tool, but it’s not a set amount of cash that you have available; it’s the maximum amount you can borrow at any given time.

Accounts with an available credit limit The most popular accounts with an available credit limit are:

Credit cards: Best known of the type, each card has a discrete limit.

Lines of Credit: A loan with a predetermined amount of funds made available to you as needed.

Home Equity Lines of Credit (HELOCs): A line of credit secured by your home’s equity.

How Your Credit Limit Is Decided

Credit limits aren’t just pulled out of a hat. They also nearly all use a thorough process called underwriting to gauge your level of financial health and calculate the amount of risk they’re taking on. This entails considering a number of important factors when determining how much credit you will extend.

Your Credit Score: This is the 800-pound gorilla. Your credit score is a three-digit number that reflects your creditworthiness. A high score (say, above 740) tells lenders that you are a safe bet, a responsible borrower who has a history of paying debts on time. This, in turn, makes lenders far more willing to give you a higher credit limit. A lower score, on the other hand, indicates a higher risk of default and could result in a lower limit — or outright denial — of your application.

Your Income and Debt-to-Income (DTI) Ratio: Lenders do not want to see that you have a regular, stable income that allows you to make your monthly payments. Your gross monthly income is the most important factor. They also evaluate your Debt-to-Income (DTI) ratio, a percentage representing your total monthly debt payments divided by your gross monthly income. Low DTI ratio Your debt-to-income ratio is typically a key indicator of financial health and a low DTI ratio (generally less than 36%) tells a lender that you’re not over leveraged in borrowing and that you can likely afford to borrow more if a lender is willing to lend you more money.

Past Payment History: The banks will examine your credit report to see how regularly and timely you have paid your past as well as current loans. One of the biggest drivers of a credit score is a history of on-time payments, and it is an effective signal of your abilities as a borrower. But a history of tardy or missed payments will probably lead to a lower credit limit.

Current Debt and Credit Utilization: A lender will consider how much you owe on all credit accounts. One indicator they look at is your credit utilization ratio (CUR), or the percentage of your total available credit you are currently using. For instance, if your total line of credit is $20,000 and you owe $2,000, your CUR is 10%. Low CUR (preferably below 30%) is a positive signal. If you are using the majority of your available credit, a lender might not want to extend your credit further.

The Lender’s Policy: Each lender has its own risk appetite. Two different lenders might look at the same financial numbers, but one may offer you a $5,000 limit while the other might offer you $7,500. It’s a good idea to apply for a personal loan with multiple lenders so you can compare offers.

Why Your Credit Limit Matters

Your line of credit is significant for two key reasons: how much financial flexibility it affords you, and, more importantly, how it affects your credit score.

Impact on Your Credit Score

Your credit limit plays a direct role in your credit utilization ratio (CUR), which is one of the most significant factors in your credit score — representing about 30 percent of your total score. The higher your CUR, the worse. “By having a high credit line and a low balance, you have a very low utilization ratio,” says Ulzheimer.

Someone with a $1,000 credit limit and a $500 balance would have a 50% utilization ratio, which is high. Another person with a credit limit of $5,000 and the same $500 balance has a 10 percent utilization ratio. Even with the same debt, the higher limiter would score better, because he or she is using a lower percentage of their credit available.

Financial Flexibility and Emergency Fund

The higher the credit limit, the more financial leeway and a safety net you have. Emergency fund — It can serve as a fund for emergency expenses such as an unforeseen major car repair or sudden home repair. So having a high limit allows you to manage those expenses without maxing out your card or needing to take on more expensive loans.

How to Raise Your Credit Limit

Bumping up your credit limit is a wise financial decision, and it can be approached in a few different ways.

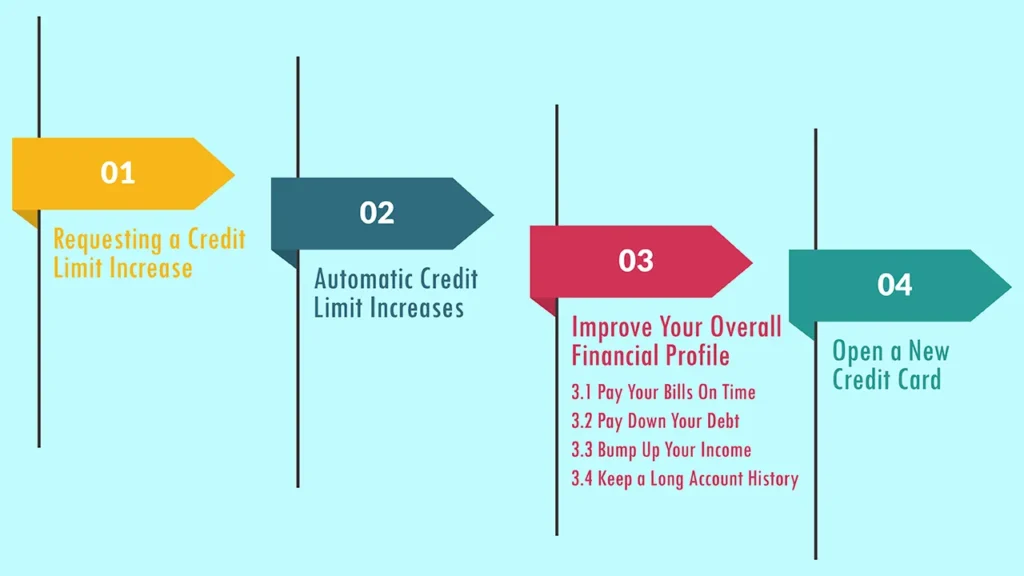

1. Requesting a Credit Limit Increase

This is the simplest way to raise a limit. After you get the card, you can ask your credit card issuer to increase your credit limit after you’ve had the card for a few months (six months to a year). Some banks now let you make this request online or on their mobile app, or you can call their customer service phone line. Before you apply, make sure you’ve the got the following:

You’ve had a history of on-time payments with that card.

You’ve been using the card regularly, but responsibly.

You now make more than when you first applied for the card.

Your credit score has improved.

The lender will probably do a hard pull on your credit report when you ask to borrow more. That can lead to a temporary, small dip in your credit score, but the long-term benefit of having a higher limit almost always surpasses this very small drop.

2. Automatic Credit Limit Increases

Many credit card issuers will periodically review your account and give you a credit limit increase without you having to request one. These are known as soft inquiries, and they do not dent your credit score.

Such automatic increases are frequently a reward for good behavior. The lender can tell from your track record of timely bill payments and responsible card use that you’re a good credit risk, and they choose to give you more credit in that spirit of trust. To activate that, just keep managing your credit well over time.

3. Improve Your Overall Financial Profile

This may be the most impactful long-term strategy for boosting your credit limit and your financial health. When you give attention to those, you simply end up being a more appealing borrower for just about any loan provider.

Pay Your Bills On Time: This is the number one most important factor with regards to your credit score. Having a perfect payment history shows lenders that you are a good risk as a borrower.

Pay Down Your Debt: The less you owe compared with what you earn, the greater your capacity for new credit. Especially concentrate on getting rid of your high-interest debt first.

Bump Up Your Income: If you’ve received a pay raise, you should let your credit card issuer know. They have a higher income, which would show an ability to handle more credit.

Keep a Long Account History: The older a credit account is and the more positive history there is, the better. This demonstrates to lenders a consistent long-term practice of responsible financial behavior.

4. Open a New Credit Card

A new credit card will also add to your total available credit, so your credit utilization ratio overall will be lower. If you have, for example, 1 card with a limit of $2,000 and a $1,000 balance (50% CUR), then you would get a new card with a limit of $3,000 bringing up your new credit to $5,000. Your $1,000 debt would then be an ultra-ultra-low 20% CUR and your credit score would jump right away.

Just be aware that opening a new account generates a hard inquiry and can lower slightly the average age of your credit accounts, which are low-level negatives on your credit score. It is a strategic move that one should engage in responsibly, and not too often.

Conclusion: Your Road to Financial Independence

Your credit limit is a big part of your financial identity. It’s more than just a limit on spending; it’s a snapshot of your financial health that’s a significant factor in the formula used to calculate your credit score. By learning what factors affect your credit limit, by adopting responsible financial behavior, and by asking for specific increases, you can turn your credit limit from a number on a card to a tool you can use to build your wealth and gain financial security.

Credit limit management is not only about debt management, it’s also about building a trustful relationship with creditors and your financial future.

Frequently Asked Questions

1. What is a high credit limit?

There is no one “good” credit limit. Even more important is your credit utilization ratio. You’ll only benefit from a high limit if you carry a low balance. A limit that is high enough that you can keep your CUR below 30% — and ideally less than 10% — is the right limit for you.

2. How frequently can I request a credit limit increase?

Many lenders will let you ask for an increase every six months to a year. But you should probably avoid it until you have a very good reason: a huge increase in income or a recent history of paying down a large debt.

3. Can a credit limit be decreased?

Yes, a creditor can reduce your credit limit. This may occur if you have been habitually late with your payments or stop using your card, or if your credit score undergoes a significant drop. The lender may be doing this to hedge their own risk.

Q: What is a high credit limit?

A: There is no one “good” credit limit. Even more important is your credit utilization ratio. You’ll only benefit from a high limit if you carry a low balance. A limit that is high enough that you can keep your CUR below 30% — and ideally less than 10% — is the right limit for you.

Q: How frequently can I request a credit limit increase?

A: Many lenders will let you ask for an increase every six months to a year. But you should probably avoid it until you have a very good reason: a huge increase in income or a recent history of paying down a large debt.

Q: Can a credit limit be decreased?

A: Yes, a creditor can reduce your credit limit. This may occur if you have been habitually late with your payments or stop using your card, or if your credit score undergoes a significant drop. The lender may be doing this to hedge their own risk.

Q: Will closing a credit card lower my credit limit?

A: Yes, it would reduce your total available credit to close a credit card. This could push your credit utilization ratio up, which could hurt you in credit scoring. That is why financial experts often advise us to keep our old, unused credit cards open, particularly if they come with no annual fee.

Is it better for my credit score to have one card with a high limit or several low limit cards?

Both can be beneficial. A high-limit card makes it easier to maintain low utilization. But more than one card can act as a safety net and boost your total available credit. The key is using all of your accounts responsibly and keeping balances low.

Multigenerational living is hardly a new concept; it’s a tradition that has defined societies for centuries across the globe — and Even if this living arrangement has become an outcast in the last years, particularly in the western world.

The reasons for it are varied, but include an increasingly unaffordable cost of living and housing, the need to provide assistance to aging mothers and fathers, and an increasing valuation of the emotional and social benefits of living in close family networks. Although this is the backbone that keeps me going, it’s also one hell of a puzzle to figure out how I can make it all work.

Melding disparate incomes, spending tendencies and life visions takes a proactive, transparent and nice AF approach. The Family Financial Planning handbook is a road map of sorts, guiding you toward establishing a financial framework that is sensible, just, and sturdy, and one that provides harmony and security to each member of your household.

The Financial Scene: Its Advantages and Disadvantage

Before getting into the guts of financial management, it’s important to appreciate the multi-generational reality of the full range of potential finances. Recognize the big wins, and inevitable roadblocks.

Financial Benefits of Pooling Resources

Big Housing Savings: For most families housing is their greatest expense. Combine homes: The great thing about a multigenerational household: the cost savings is huge when it comes to rent or a mortgage, property taxes, and insurance. Just the savings from this category alone can be huge for each family unit to reappropriate funds into other financial goals.

Lower Childcare and Caregiving Costs: That built-in babysitting can be a boon for a family with young children, offering a reliable, well-vetted, and often free childcare option and crossing one of the biggest household expenses off the list. On the reverse side, adult children can provide everyday services for elderly parents, reducing or postponing expensive in-home or assisted living care.

Faster Financial Plans: By sharing costs, single people and families are able to multiply the opportunities to immediately convert their earnings. This extra money can be used to pay down high-interest debt, stockpile a super strong Emergency Fund, save up for a downpayment on another house much faster than you would be able to on your own.

Possible Money Issues: Let’s Get Real

Different Financial Philosophies: Money tends to be a very private matter. A generation may be focused on paying down debt, while another is living with a spend-now splurge-now philosophy. If not addressed and openly discussed, these different worldviews can cause tensions.

Unequal Contributions Instances: where all adults contribute equally to the household are few and far between.” Figuring out a fair way for each party to contribute can be a source of tension, particularly if it seems like someone is doing more than his or her share.

No Financial Privacy: Sharing confined living spaces can confuse the lines between individual and collective finances. An absence of privacy might breed judgment or resentment if one partner’s spending habits are always under a spotlight.

Serious Legal and Tax Consequences: There may be complex legal and tax issues associated with the financial transaction. The merging of assets, shared home ownership and potential gifting can impact taxes, inheritance and legal rights.

Phase 1: The Foundation – A Collaborative Vision and Formal Agreement

Before any bills start getting paid, the household needs to build some trust and have clear expectations in place.

1. Hold a Formal Family Meeting

This is not dinner-table kibitzing. Arrange a sit down chat with ALL the adults who contributes financially. The agenda should include:

Common Goals: Talk about what each party wants to get out of the situation— maybe it’s to save for a home, pay down debt, or just get on top of money matters.

Personal Needs: Everyone should share what you need in terms of your own finances and limitations – any debts you already have to be paid off, the savings goal you’re hoping to hit, and any expenses that you absolutely cannot compromise on.

Communicate: Decide how and when you’ll talk about money in the future. Frequent checks (down to monthly) will help you avoid little problems before they turn into big ones.

2. Create a Formal Written Agreement

Word of mouth, as well-meaning as it is, is easily forgotten, or misheard. Draw up an informal written agreement — a Household Financial Agreement — that dictates the terms of your cohabitation. Thos agreement should be read through and signed by all parties. It should include:

Contributions to Housing: Who is covering the mortgage, rent or property taxes, and how are they being covered?

Expense Split: Clearly defined: who is pay for each shared expense.

Emergency Fund Plan: A plan for how you would address unforeseen costs — say, a major home repair or a family member losing their job.

Exit Strategy: What if a family member wants or needs to leave? Having a solid plan up front can prevent a lot of headaches later.

Phase 2: Construct the Budget and Determine the Split of Expenses

It’s about transforming your shared vision into a functional succuessful budget that every one will be able to follow.

1. Establish a Shared Household Budget

Draw up all of your joint costs into one, grand budget. It should be told not just in dollars but in money this country spends on:

Cost of Housing: This is the major one. Calculate the costs involved in owning your home, including the mortgage and home insurance, and any HOA fees.

Utilities: Account for all your recurring bills, including electricity, gas and water, WiFi and subscriptions.

Groceries and Household Supplies: Set a monthly or weekly budget for food and shared items such as toiletries and cleaning supplies.

Emergency and Savings Fund: Determine whether you’ll each put money toward a joint emergency fund for household-related emergencies.

2. The Art of Fair Contributions

Now that you’ve figured out the total budget, you need to decide how to allocate that budget. The most common methods are:

Equal Split: The easiest way, but it’s fair only when all adults make comparable wages. If two adults are making about the same income, each pays half. All right, where there were three, they pay a third portion each.

Proportional Share: When earnings differ, this is frequently the fairest solution. The contribution is a proportion of an individual’s take-home pay. Of this then, for instance, if the income of the family will be $10,000 and of this the man earns $6,000, he will bear 60% of the total costs of the common expenses. This is in order to prevent giving too much to one family member.

Dividing Expenses:This is just assigning bills to individuals. For instance, Person A covers the mortgage, Person B covers the utilities, and Person C buys all the groceries. It can feel less clear and needs careful tracking to ensure it is fair.

To take care of a shared budget, set up a shared checking account just for bills or opt for a digital tracking app such as Splitwise, which helps you keep a log of expenses and split the costs at the push of a button.

Phase 3: Long-Range Money Management for Everyone and Every Generation

The ultimate power of a multigenerational household is the chance to lock in the financial future of everyone living under one roof.

1. Retirement and Long-Term Care

And millennials for whom a multigenerational home can mean hundreds of dollars in savings each month will have a chance to supercharge their retirement savings. For the elderly, it allows their retirement savings to stretch further by lowering their living expenses.

It’s also that time to have a direct discussion of long-term care needs. See if a parent has long-term care insurance; if not, how would the family handle potential health costs together, in the future?

2. Estate Planning and Inheritance

It’s a touchy but crucial issue. A clear agreement must be in place at the outset to ensure that there will be no future disputes as to the ownership of the property.

If the home is being purchased by the younger generation, and a parent (or parents) is contributing to the purchase, is that contribution a gift, a loan or a share of equity?

Meets with an attorney to make sure everyone’s desires are legally documented, whether in the form of a will and/or trust, or other estate planning mechanisms.

3. Shared Investments and Goals

You could pool your resources and start a collection for shared, long-term goals. This might be a vacation fund, a home renovation fund, or perhaps even a college fund for the next generation of offspring. When you are working together to achieve something for real, you foster an essence of teamwork, and that leads to collective success.

Phase 4: How to Have those Tough Talks & Keep the Peace

Life happens, even for the most well-laid plan. Finances can change and there can be disagreements.

1. Addressing Changes in Income

A job loss, a medical calamity or a career shift can undermine the financial plan. The written agreement should specify what occurs in such an instance. You can establish the understanding that either contributions will be temporarily reduced or responsibility will be shifted until they are back on their feet.

2. Handling Financial Conflict

Should any issues or disputes arise, you can simply refer to the written contract. This letter takes the emotion out of it – you can stick to the facts. If that doesn’t solve the problem, think about enlisting a neutral third party, like a financial planner or family friend, to help mediate.

3. Make Sure to Have Regular Financial Check-ups

“Just like you would with a business, you have to have regular financial check-ins. Gather once a month to go over the budget, upcoming expenses and make sure everyone’s still on board with the deal. It stops little problems from becoming huge stress-inducers.

Conclusion: Communication and Compassion

At the end of the day, what successful multigenerational families both have in common comes down to two things: open communication and empathy. A financial plan is not a binding contract — it’s a dynamic thing that should change as your family’s needs change.

Treating every money conversation with respect, transparency and a willingness to compromise is a way to create a financial system that supports everyone’s aspirations. It’s not just about dividing bills; it’s about building a sense of trust and security that grows family and community ties for generations.

Frequently Asked Questions

1. What if we’re unable to come to an agreement on a budget?

Begin with the bare essentials — a place to live, utilities and just what you need to eat. Once you’ve signed off on those nonnegotiable costs, you can move on to voluntary spending.

If a full budget feels impossible, you might think about setting up some simpler form of a “bill allocation” system, where each of you is responsible for one big bill.

2. Is it a good idea to open a joint bank account?

Do not mix your money in your account unless you’re a couple. A far better and more secure bet is to keep a separate “household” checking account. Both adults pay their portion of the communal outgoings into the account and all bills are paid from there.

This provides some financial autonomy, and makes separating finance easier in the event the two of you no longer live together.

3. Is a parent’s debt a family issue?

Adult children are not liable for a parent’s debt. But it certainly can affect the family per se from a financial perspective.

The ideal is for the two of you to have a frank discussion to come up with a plan to address all the debts without allowing that to place an undue burden on any one family member.

Enjoying the advantages that come with being self-employed, but there are also large financial responsibilities you may not have as a traditional employee. You are not just the CEO of your own business but also its accountant, HR department and financial planner.

With no regular pay cheque, employer-provided benefits, or automatic tax withholding, strong financial planning isn’t just a nice thing to have — it’s a must. The purpose of this guide is to provide you with the information and tools necessary to develop a solid financial plan while dealing with the peaks and flows of irregular income and help you confidently manage the solitude and uncertainty that comes with being self-employed.

Step 1: Laying the Foundation – The Cover of Cash Flow

Before you can make a financial plan, you need to know where your money’s been going. This is particularly important for the self-employed, as your income could be inconsistent.

1. Separate Business and Personal Finances

This is non-negotiable. Open a business payment account and secure a business credit card. It’s that simple — you’ll save yourself tonnes of headaches come tax time.

won’t commingle funds, and you’ll have a concise understanding of how much money your business made (or lost) when it comes time to assess your profitability. All your income should flow into your business account, and every business expense should be made from it.

2. Becoming a Pro at Variable Budgeting

Forget the fixed monthly budget. In the topsy-turvy realm of income variation, you want an adjustable system. This “pay yourself first” model really works. Every time you receive a payment, apply proportions to various financial buckets:

Taxes: Dedicate a portion (such as 25-35%) for estimated taxes.

Emergency Fund: Shoot for 6-12 months of living expenses.

Operating and software expenses, supplies.

Personal Pay cheque: You can pay yourself a regular “pay cheque”; even if it’s negligible, it can represent living expenses.

Savings and Investments: Stick some in a retirement or broking account.

Step 2: Creating Your Safety Blanket and Savings

Now that you know your cash flow cold, you’re ready to craft the core of your financial safety net.

1. Prioritize Your Emergency Fund

An emergency fund is the first line of defence in the event of income lulls, unanticipated business-related expenses or personal emergencies. You should aim to have at least 6 months’ worth of your living expenses in a high-yield savings account.

For the self-employed, 9 to 12 months is even better to accommodate longer stretches of low or no income. This is the fund that lets you ride out a slow season without going into debt.

2. Get Health, Disability, and Life Insurance

As an independent contractor, the benefits are all up to you. Do not overlook this.

Health Insurance: Check your state marketplace or the AAMC website for resources like professional organisations and private plans. Shop around to find a plan that fits your budget and your needs.

Disability Insurance: This is probably the most neglected area of insurance for freelancers. It pays a portion of your income if injury or illness prevents you from working. A long-term disability policy is a necessity for protecting your financial bottom line.

Life Insurance: A term life insurance policy is a must if you’ve got dependants who need to be financially secure in case anything happens to you.

Step 3: The Long-Term Plan – Retirement and Investment

Then you should work on building long-term financial security.

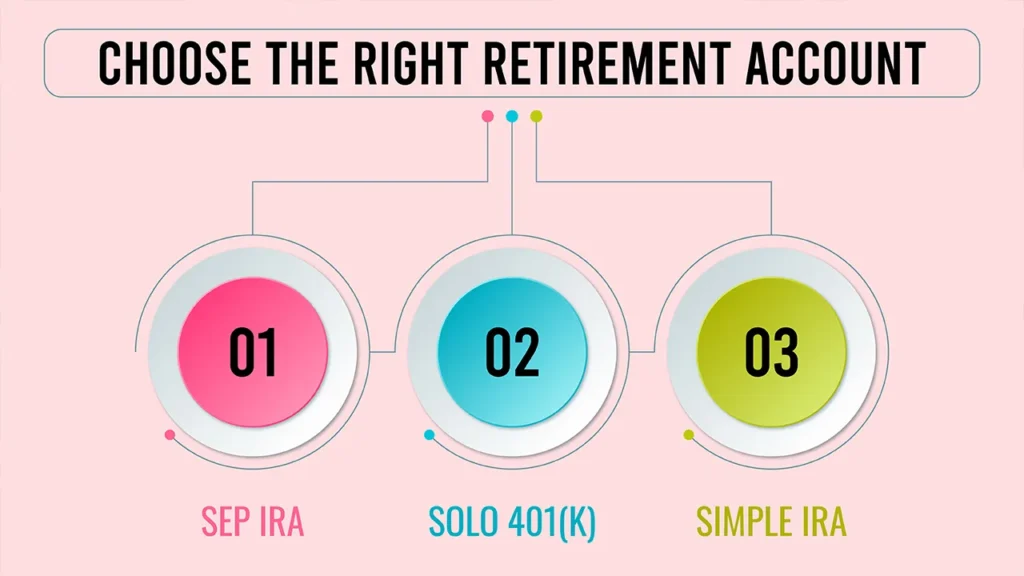

1. Choose the Right Retirement Account

Here’s where self-employment can really shine. You have access to powerful, high-contribution retirement plans available only to employers.

SEP IRA (Simplified Employee Pension): Simple to establish and permits high contributions — up to 25 per cent of your net self-employment earnings, with an annual limit.

Solo 401(k): Best for self-employed individuals with no employees other than a spouse. You can contribute as an employee and as an employer, so your total contribution can potentially be much greater than with a SEP IRA.

Simple IRA: Decent if you have just a few employees, as it has lower employer contributions.

Traditional or Roth IRA: If your business is new or has low profits, consider beginning with a standard IRA.

2. Invest Beyond Retirement

Don’t stop at retirement accounts. For buying stocks, bonds or ETFs, consider opening a regular broking account. That will enable you to build a diversified portfolio that you can access at any time for goals that will be many years away, like buying a home, funding a child’s education or saving for early retirement.

Step 4: The Tax Strategy

Taxes are perhaps the scariest segment of financial planning for the majority of self-employed people. But they don’t have to be.

1. Set Aside Money for Taxes

As I covered in the budgeting section, the simplest way to deal with taxes is to save a percentage from every payment you receive. This avoids the frantic rush at the last moment and ribbons that are always ready.

2. Pay Estimated Quarterly Taxes

Four times a year, you have to remit income tax payments as a business owner. Penalties can be incurred by missing these deadlines. Circle those due dates on your calendar and put in those payments on time.

3. Maximize Your Deductions

Track every business-related expense. From office supplies and software subscriptions to mileage and home office expenses, those deductions can add up to a sizable reduction in your taxable income. Use accounting software to make this task automatic and save yourself a huge headache come tax time.

Conclusion: Your Journey To Financial Independence

The reality is, you’re on a path to financial planning as a self-employed professional, not a race. It begins with basic steps — dividing your finances, establishing a flexible budget, and building a rock-solid safety net.

From there, you can move on to smart investments, long-term retirement planning and a streamlined tax strategy. And, by mastering these essentials, you’re not only managing your money — you’re setting up a sustainable, secure future for yourself — one free from the stress of financial insecurity that can accompany self-employment.

Frequently Asked Questions

1. What’s the most successful way to manage money where income isn’t the same each month?

You just have to budget for that or budget for the low end, whatever your lowest month is on average. The same goes for a high-income month—use the surplus to save and pre-fund your lower-income months. This provides a layer of support.

2. Should I be a sole proprietor or set up an LLC?

A sole proprietorship will be the easiest to start but offers no liability protection. An LLC (Limited Liability Company) offers you legal protection by creating a barrier between your personal and business obligations. It depends on the size and risk of your business.

3. What’s a good percentage of my income to save?

The old rule of thumb of saving 15% of your income to support yourself in old age still stands. You’ll probably want to target even more than that, maybe 20% or more, as a self-employed person to also cover your savings for insurance and other benefits an employer typically offers.

4. Can I run my business from a personal account?

Technically yes, but it’s highly discouraged. It makes the accounting a nightmare and can lead to legal and tax headaches. It also makes your business appear not as professional. It’s never too early to start with business and personal finances being separate from day one.

College and university life is a dream come true for many, offering up excitement and challenges – as well as new financial responsibilities. This is the first time for many students to be on their own and with money. Create financial goals from freedom, not deprivation.

This is the difference between simply surviving and genuinely thriving. Setting goals makes it easier to spend your money while lowering the stress and helping you realise truly impactful things, both little and big.

Discover essential financial goals for students to achieve financial independence. Learn budgeting, saving, and investing strategies tailored for your success.

Part 1: Why bother having financial goals?

Financial Peace of Mind

Goals and a plan for money relieve anxiety and tension. You can see where your money is going, which helps you feel more in control. Like, you know you have a portion of money for textbooks or to fix your car in case it breaks down—so no need to panic if either one happens.

Motivation and Discipline

Goals make high-level concepts like saving money something real, concrete and actionable. Progress Tracking is Bit of a Reward Being able to see that savings account number rise for a study abroad or new laptop is motivation enough to learn how to say no to small, unnecessary expenses.

Establishing a Framework Going Forward

Budgeting, saving and not getting deep into debt are habits that we wish to continue for the rest of our lives. Now, learning to keep a credit card in good standing is setting you up now to be able to secure a car loan or an apartment later.

Part 2: How to Set Goals (A Step-by-Step Guide)

The SMART Framework

Smart: an acronym that is used in a famous technique in goal setting

Remember: What exactly is it you want? One specific goal (I want to save $500 for a new laptop) is clearer than the very vague :I want to save money

Measurable: In what way can you measure your progress? For example: “I will save $50/month.”

Attainable: Does this goal really work for you? Saving 50 over 10 months is really true, hey.

Relevant: Do you need that new laptop for school, or is it another way to avoid paying down a high-interest-rate credit card?

Time-based: What is the deadline? They could be something along the lines of “by the end of the semester” or “by December 1.

Create a Financial Snapshot

It is essential to clarify your present financial condition before enumerating goals. This involves:

Listing any income you have (i.e., a part-time job, allowance, etc.).

Tracking all your expenses for a month (rent, food, subscriptions, etc.).

Thanks to helpful tools like budgeting apps or simple spreadsheets, this task should not be all that difficult.

Prioritize and Categorize

Redefine your targets in accordance with short-term, medium-term and long-term so that they do not appear as a burden.

Part 3: Specific Financial Goals for Students

Goals for the Next 12 Months or Less

Building a baby emergency fund ($1,000 for unexpected expenses)

Textbook and School Supply Savings

Saving with a specific goal or purchase intention (phone, concert ticket, clothes)

Reunification Visit or Holiday Weekend Save for

Medium-Term Goals (1-3 years)

Summer internship or a semester abroad savings.

Making a down payment on a pre-owned car.

Other examples include payment of a certain student loan or paying off credit card balance(s).

Setting aside money to put down a security deposit on your first apartment post-graduation.

Long-Term Goals (3+ years)

Down payment on a house

Creating a retirement fund (such as an IRA)

Majorly paying down or paying off student loans

Part 4: Real Items and Actual Tools for Genuine Results

“Pay Yourself First”

Separate savings account: Set up an automatic transfer of a portion of each pay cheque to another account before ever spending. This ensures you prioritise saving.

Budgeting Apps and Tools

Check out apps tailored for students that are popular, such as Mint, PocketGuard, or YNAB, so everyone knows how much they’re spending, and Splitwise to not only help people in 50/50 situations but also in shared arrangements. These tools allow for simplifying budgeting and tracking.

Student Discounts and Smart Spending

Students can save money by utilising student discounts, cooking at home more often and taking care to avoid “lifestyle creep”.

Track Your Progress

Keep your eyes on the prize and check in on those goals often to remind yourself of where you are headed. This way you keep on the hook and in line with your goal.

Conclusion: Begin Your Financial Future Today

Financial goals go a long way in helping you stay stress-free and motivated and also help build a strong financial foundation for the future. Every tiny advancement you make now – even if it is just your first $100 saved or your very first budget created – is serious leverage on you in 10,000 days. Choose one target and start immediately!

Frequently Asked Questions

1. How do I create monetary objectives when I have unpredictability about my earnings?

You can still have financial goals even without a pay cheque. Put your efforts into tracking your spending – this will give you insights into where your money leaks.

Maybe you have a goal to cut a specific amount of money from your monthly costs, or maybe it is saving $10 from every gift & odd job you get.

2. I have student loans. Do I need to pay them off first, or is that another type of saving?

What can people do to take care of their mental health in the meantime? A: To keep away from going into additional debt, begin a small emergency fund for any surprises.

From there, concentrate on high-interest debt like credit cards ahead of more student loan obliteration. You could make an objective to pay just a little more than the minimum payment each month in order to lower the total interest you’re on track to repay over time.

3. What happens when one falls off the track and fails to meet a goal?

Don’t beat yourself up! Financial setbacks happen to everyone. But the key is this – getting RIGHT back on track.

Take another look at your budget, give yourself more time to reach this goal if you need it and try again. Each morning is a chance to do something right.

Ever feel like your money is controlling you? Wish you had a better understanding of where your money is going and what will make it grow? If so, you’re not alone. It’s not unusual to find people feeling overwhelmed, stressed and anxious around their money. There is, however, one solution: Personal Finance Management (PFM).

PFM is a process of effectively managing your money to accomplish your financial goals. In this article, we’ll discuss what PFM is, key concepts related to PFM, the instruments that can be used and how it can be applied in everyday life. After tackling it all, you’ll know how to regain control of your financial future and feel empowered to take charge of your financial destiny.

1. What is PFM?

Personal Finance Management (PFM) is the act of planning, organising, directing and controlling monetary activities such as budgeting, personal financial planning, cash flow, savings and spending by an individual. It includes all your financial life, how you earn, spend, save, invest and protect your financial resources.

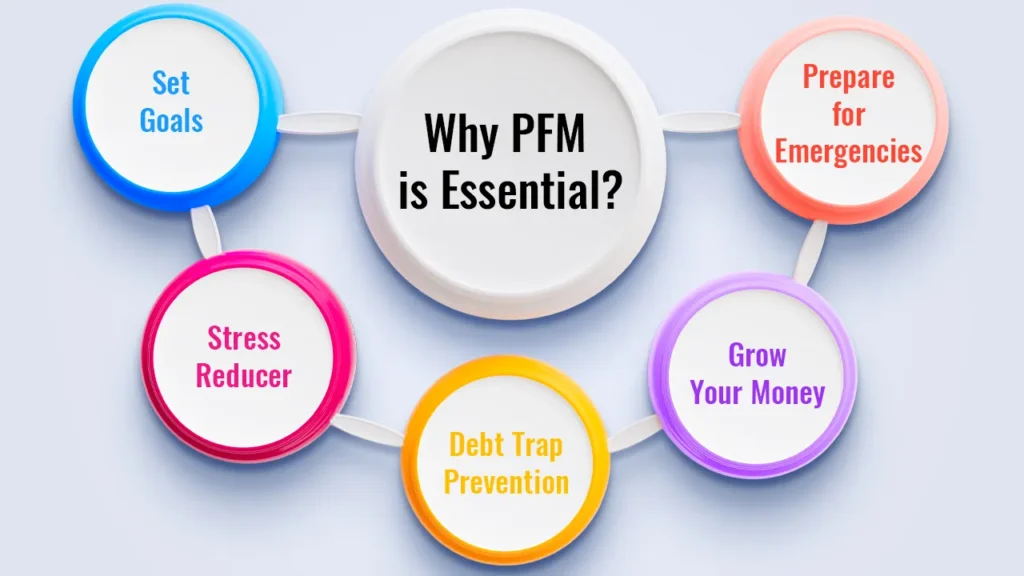

Why is PFM Essential?

Set Goals: ‘PFM tooling provides a path to achieve short-term (e.g., holiday, new gadget), medium-term (e.g., down payment, education fund) and long-term goals (e.g., retirement, financial independence).’

Stress Reducer: Gain financial clarity and control to cut money-related stress. Knowing where your money is going and having a plan in place can help relieve anxieties about surprise costs.

Debt Trap Prevention: By keeping track of expenditure vs income, PFM avoids borrowing unnecessarily. It promotes living within one’s means and financial responsibility.

Grow Your Money: PFM provides the structure for regular savings and smart investing, allowing for the accumulation of wealth over time. It further helps you figure out what you should be investing in that matches your money goals.

Prepare for Emergencies: PFM gives you the cushion you need when life puts challenges in your way, whether it’s an accident or injury or losing a job. Being prepared with an emergency fund will help you feel secure and at peace about your financial life.

Key Principles of Effective PFM

Goal Setting: The first and most effective part of PFM is thinking through what you want to accomplish financially. Clear objectives give motivation and direction to people.

Tracking & Awareness: It’s all about knowing what’s coming in and what’s going out. Continuously monitoring your income and expenses keeps you aware of your monetary position.

Budgets: Pre-planning your expenses helps you survive financially. If nothing else, a budget goes a long way in helping you prioritize the things you need and when you are able to save for future goals.

Discipline: A plan has to be followed and choices have to be made for PFM to work. It’s a test of discipline against the urge to spend without thinking.

Review & Adapt: It’s important to regularly review and adjust your position. Life is dynamic and situations change, so your financial plan should be a dynamic, living document.

2. How Personal Finance Management is Used – Main Components

RGS is not a single action but a loop that goes through many interconnected parts:

1. Income Management

Knowing all forms of income (wages, freelance gigs, investments, passive income) and optimizing earning potential.

How it’s Used:

Finding Your Income Streams: Knowing where money is coming from tells your financial story.

Scheming for More Money: Learning new skills, taking on side-hustles, or asking for raises to improve your cash flow.

Knowing the Tax Impact: Knowing how different sources of income are taxed can help you plan better.

2. Expense Management & Budgeting

Being in charge of your money and establishing a plan for spending it.

How It’s Used:

Tracking: Tracking every expense to see how and where you spend obviously helps you see where you are spending your money.

Categorisation: Groupings of expenses (i.e., housing, food, clothing, transportation, and entertainment) lend to better analysis and control.

Budgeting: Planning how much to spend in each category (for example, the 50/30/20 rule or zero-based budgeting) helps keep your spending in check.

Saving Money: It’s easy to find places where you can reduce excessive spending.

3. Savings & Investment Planning

Setting money aside to be used for future needs and wants and allowing it to grow.

How It’s Used:

Saving with a Purpose: Setting aside money for targeted goals to prepare for future expenses.

Creating an Emergency Fund: Having an emergency funds goes a long way to financial safety.

Investment Strategy: Investing through appropriate investment vehicles (stocks, bonds, mutual funds, real estate) based on your risk tolerance and the time frame you’re working with are the drivers of wealth growth.

Compounding: Using returns to generate more returns can be a powerful way to boost your savings over the long term.

4. Debt Management

Tactically managing borrowed funds to reduce interest, as well as pay down debt faster.

How it’s Used:

Debt Prioritization: Determining which debts to pay off first (e.g., high-interest debt like credit cards) reduces overall interest costs.

Debt Payoff Tactics: Apply a variety of strategies, such as the debt snowball or debt avalanche, to speed up repayment.

Monitoring Credit Scores: Knowing how debt affects credit scores and wanting to improve it for future borrowing is necessary.

Preventing Detrimental Debt: Educated decisions about future borrowing are a way to avoid getting buried under the weight of debt.

5. Risk Management & Insurance

You would have protected you and yours from financial loss brought on by the unexpected.

How it’s Used:

Insurance Needs Assessment: For both individuals and businesses, not all of our life and the life of our business is covered by insurance.

Policy Choice: Selecting the right insurance policies and understanding their terms mitigates the risk.

Backups: You need to be able to withstand potential job loss or big unexpected expenses to be in decent financial shape.

6. Tax Planning

Tactically manoeuvring the funds to either minimize tax or maximize for tax benefits.

How it’s Used:

Knowledge Of Tax Laws: Keeping up-to-date with income tax, capital gains tax and other taxes that apply to you will allow you to effectively plan.

Leveraging Deductions & Exemptions: Using what is legally at your disposal for reducing your taxable income can save you money.

Tax-Sensitive Investments: Selecting investments that provide some tax advantages can add value to your overall plan.

3. Tools and resources to help you manage your money

Various tools make modern PFM easier:

PFM Software & Apps

Features: budgeting, expense categorization, goal-setting, calculating net worth, bill reminders.

Examples: Popular apps include Mint, YNAB (You Need A Budget) and Personal Capital, PocketGuard, or region-specific apps like Cred, ET Money and Groww.

Spreadsheets

Features: Customisable for more detailed budgeting, tracking and financial modelling (e.g., Google Sheets, Excel).

Benefit: Provide flexibility for people who like to work with numbers by giving them more control of their own financial planning.

Traditional Methods

Notebooks/Ledgers: There’s no better way to track income and expenses than getting your hands dirty (but not really).

Envelopes: For taming cash for flex spend categories, to keep spending in check.

Financial Advisors & Planners

Role: Offer personalized advice, assist with complicated goal setting, create full financial plans and provide ongoing guidance.

When to Use: Major life decisions Complex financial planningWhen you need to talk to an expert, unbiased person.

Educational Resources

Books, blogs, podcasts, online courses and workshops are full of great advice about managing personal finances.

Conclusion: Take Control of Your Financial Future with PFM

It is an all-inclusive and an ongoing process which includes everything from income, expenditures, savings and investments to debt, risk and tax planning. Smart PFM is not about strict stricture, but about making clear, intentional choices that serve your values and vision.

It’s the ultimate guide to money – not just the amount you need to learn and the amount you need to earn, but what you need to be in order to earn it and keep it. So take charge of your finances with PFM and set yourself up for a safe, prosperous future.

Call to Action

Get your PFM journey off the ground with our budget template! Discover powerful PFM apps that make it effortless to take control of your finances: start on the road to financial freedom!

Frequently Asked Questions

1. What are the 5 areas of personal finance?

Earnings Spending Saving & Investing Protecting Borrowing There are 5 pillars of personal finance.

2. What makes personal finance hard?

No, it can be difficult, especially when getting started, but once you adopt a routine, it gets easier, and you begin to use the appropriate tools.

3. What is the best starting PFM tool?

Software like Mint and YNAB (You Need A Budget) are relatively easy to use and work well for those who are just starting to manage their finances in a meaningful way.

Ever get the sense your money flows through your fingers like water? Or have you wished you had a greater say over your financial destiny? Accountability is the bedrock of one’s well-being and realising goals in life.

This post will outline the basics and things you can actually do to get control of your financial life. Keep in mind, financial prudence is a teachable skill for anyone – regardless of your circumstances.

Discover essential principles of financial responsibility. Learn budgeting, saving, and investing to secure your financial future and achieve your goals. Learn about insurance claims, including their definition, operational process, and the different types, to ensure you understand your coverage options.

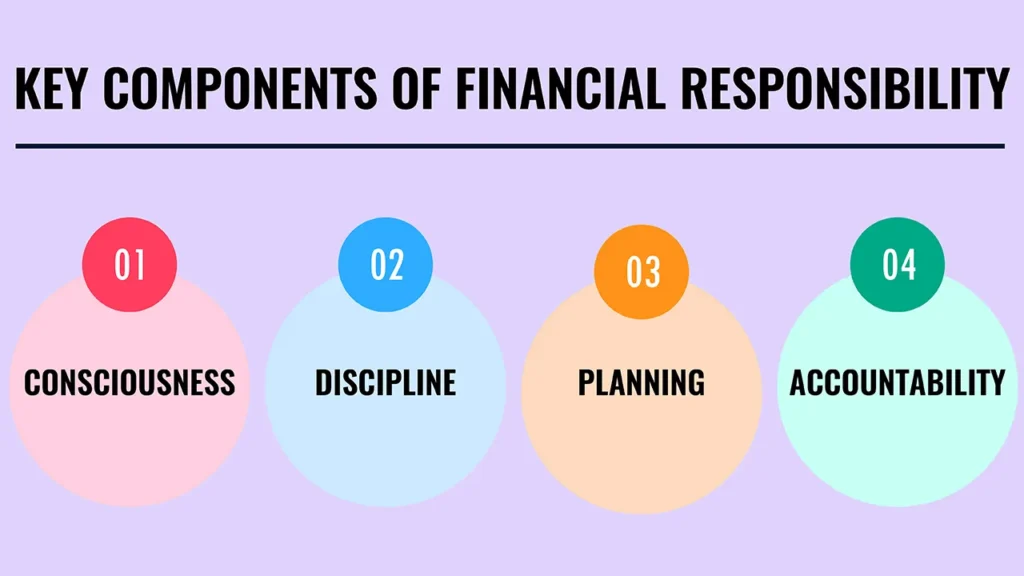

What is financial responsibility? Defining Control and Conscious Choices

Taking responsibility for your financial well-being and managing your money to provide the life you want for yourself and your family. What It Means: Financial responsibility is making sure all your expenses can be paid for and learning how to invest properly, whether that means saving for retirement or putting together a rainy-day fund.

Key Components:

Consciousness: Being clear on where your money comes from and where it goes.

Planning: Establishing targets and working out the path.

Accountability: Responsibility for your financial situation.

Why it Matters

Being financially responsible is the difference between getting relief from stress, creating wealth, meeting goals (house purchase, retirement, etc.), and dealing with emergencies.

1. Get Clear on Your Income & Expenses (The Budgeting Blueprint)

Know Your Income

Relate gross income (before deductions) and net income (take-home pay).

Calculate all of your regular sources of income (salary, freelancing, side hustles).

Track Your Expenses

The first step that matters: where is your money actually going?

Segment spending: Fixed Expenses – rent/EMIs/subscriptions VS Variable Expenses – groceries/personal, entertainment and dining out.

Create a Budget (Your Money GPS)

Purpose: A system for how you will spend and save your own money.

Zero-Based Budgeting: Tell every rupee where to go.

Envelope System: A tactile take on money management for variable expenses.

Tools: If you can, suggest software apps or spreadsheets, or advise that they, at minimum, write everything down.

Budgeting tips: Be realistic; review regularly; adjust as your life changes – and be prepared to make mistakes and learn.

2. Establishing your financial safety net (the emergency fund)

What is an emergency fund?

An appropriated fund of liquid cash designated for unexpected life happenings.

Why You Need One

Protects against the loss of a job, a medical emergency, unexpected repairs to the home or car, or a sudden family demand. It shields you from taking on debt during crises.

How Much to Save

Target saving 3-6 months of essential living expenses (or more depending on job stability and obligations).

Where to Keep It

In another readily available account, such as a high-yield savings account or a liquid fund. The target is liquidity and safety — not high returns.

3. How to Use Debt as A Strategy (Keys to Financial freedom)

Understanding Different Types of Debt

Good Debt: Debt taken for buying such a thing of value that appreciates over time and a loan for education/career point of view (house loan, education loan)