Private equity titans KKR & Co. and Blackstone Inc. are among the buyout firms said to be part of a group offering a massive $90 billion to buy the U.S. operations of viral video-sharing app TikTok from its Chinese parent company, ByteDance Ltd., in a deal that could shake up global social media, according to various media reports.

That new push for a sale is occurring as TikTok is confronting a potential ban in the United States over national security concerns.

High-Risk Gamble Under Current Geopolitical Conditions

The stratospheric valuation is further evidence of the extraordinary perceived worth of TikTok’s U.S. business, with its more than 170 million American users and over $12 billion in ad sales in 2024. The offer is being spearheaded by a group that also involves Oracle Corp.

And venture-capital firm Andreessen Horowitz, according to people with knowledge of the discussions. This isn’t the first time the group has tried to buy up TikTok’s U.S. operations. One such transaction, which would have given new outside investors half of TikTok’s US business and reduced ByteDance’s holding to below 20%, reportedly fell through in April when China refused to sign off its approval (paywall), after the US had applied a previous round of tariffs.

The current acquisition negotiations are being held under intense pressure. A law signed by then-President Joe Biden in the past year required ByteDance to sell TikTok’s U.S. operations by the deadline of January 19, 2025, or be forced to shut it down.

Though the U.S. Supreme Court has upheld the law, U.S. President Donald Trump’s administration has continued to delay the deadline (most recently to mid-September), hoping to broker a deal that would “save TikTok” for Americans.

Oracle’s Role and Data Security

One of the linchpins of the proposed deal is for Oracle Corp. to have a minority stake and provide assurances on the security of user data. Oracle already supplies the cloud infrastructure for TikTok in the U.S. under previous agreements, which were adopted months ago in an effort to allay concerns that Chinese authorities could obtain access to information from the app.

The new deal would probably entrench and expand Oracle’s oversight of U.S. user data and software updates to meet American national security needs.

Challenges and Chinese Approval

EVEN as it is, any deal is heavily conditioned – conditional on the approval of various players, including the Chinese government and its president, Xi Jinping, who must now struggle with the mixed feelings of dealing with an American president who demonstrates enough unpredictability to be dangerous.

China has repeated its “principled position” on TikTok matters, saying business conduct, including mergers and acquisitions, must follow market rules and respect international laws and Chinese laws. Beijing has previously signalled resistance to a forced sale of TikTok, especially of its core algorithm, which it has called a national asset.

The $90 billion number is a hefty premium over earlier valuations, which had the value of TikTok’s United States business ranging from $20 billion to $150 billion, depending on what terms and technology were involved.

Representatives for Oracle, Andreessen Horowitz, ByteDance and TikTok either did not respond to requests for comment or declined to comment, and neither KKR nor Blackstone have publicly commented on the matter, but during an interview last week, President Trump said he would be announcing the group of buyers “in about two weeks’ time”.

The weeks ahead will be crucial as the two sides try to unwind geopolitical complexities and navigate regulatory impediments to consummate a deal that could set the future of one of the world’s most influential social media platforms in the U.S. market.

Fed up with your money just languishing there? Imagine it working for you, accumulating wealth as you sleep. Real estate investment represents a compelling path to wealth, and this guide will help you get started investing in real estate property.

We’ll cover the most important concepts, including the benefits of real estate and actionable tips for starting out. Whether you are a novice investor or just interested in diversifying your portfolio, this guide is for you.

Unlock the potential of real estate to diversify your investment portfolio. Find expert tips and strategies to achieve financial growth and stability.

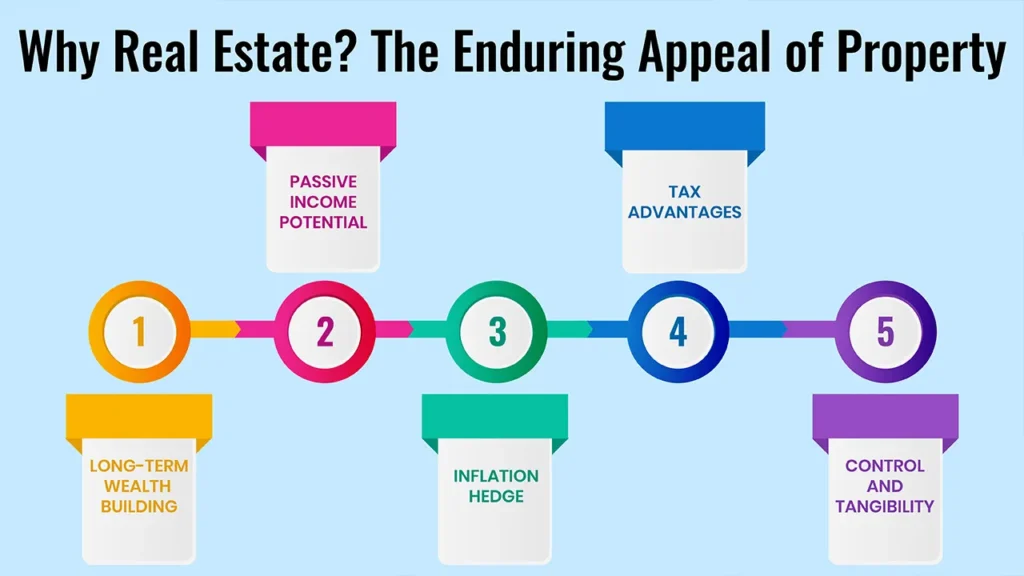

Why Real Estate? The Enduring Appeal of Property

Long-term Wealth Building: Values of property appreciate with time, leading to substantial wealth creation. Real estate investment is an excellent foundation for a solid financial future.

Passive Income Potential: Rent providing an ongoing influx of cash makes the purse strong and enables one to save and reinvest (in more property).

Inflation Hedge: Real estate can hedge against inflation, preserving your purchasing power over time.

Tax Advantages: There are potentially deductions and depreciation benefits and the rules for what are known as 1031 exchanges (there are many rules, and it is generally the best plan to seek a professional with experience in this complex manoeuvre).

Control and Tangibility:Real estate investments are physical assets you can touch, and that means stability and security.

Before You Start: Essential Foundations for Aspiring Investors

Financial Health Check

Good Debt Vs. Bad Debt: Determine the Difference Learn how to manage existing debt so that it doesn’t take away from your financial standing.

Save your Emergency Fund. Save your emergency fund and build it up to be a bit more robust when compared to the norm of 3-6 months of expenses that people stress over.

Good Credit Score: It’s important to have a credit score in good standing to receive financing at lower interest rates.

Setting Clear Goals

Define your objectives in terms of investment, such as passive income purpose, target for capital appreciation, and early retirement. Discriminate between short (and long) range objectives that will shape the strategy.

Education is Key

Invest in your knowledge by those books, podcasts, online courses and mentorship which you trust the most. It is essential to be familiar with the local real estate cycles and trends as you make critical decisions.

Assembling Your Team

Find the necessary professionals to help you on your investment path, such as a reputable realtor, an educated loan officer, an attorney, an accountant and even a property manager.

Most Popular Real Estate Investment Strategies for Beginners

1. Rental Properties (Long-Term)

Concentrate on residential (single-family, multi-family) properties as a means of income. It could be the concept of buying properties and renting them out for predictable, monthly cash flow, albeit with landlord responsibilities that can be transitioned to the use of a property management service.

2. Real Estate Investment Trusts (REITs)

Owning a portfolio of income-generating properties via the public markets provides liquidity, diversification among a range of property types, and professional management. But it can have less direct control over specific IMTs of metadata than direct ownership.

3. Real Estate Crowdfunding

This also pools money with other investors to fund large real estate projects, so you don’t have to fork over a tonne of money to get into commercial or large residential projects. But investments may be less liquid than REITs, and control is minimal.

4. House Hacking

Owner-occupied rentals – Housing costs can be reduced through purchasing a multi-unit property (e.g., duplex, triplex) in which you live in one unit and rent out the others – This also offers first-time landlords a taste of on-the-ground landlording experience. But that depends on having to live on the property, and that might pose a privacy issue.”

5. Market Research

Evaluate the critical factors — such as population growth, job growth and median income patterns. Look into rental demand, average rental prices and vacancy rates, and the amenity and future infrastructure plans for the area.

7. Neighborhood Analysis

Evaluate factors such as the quality of school systems, the area’s crime rate and property value history. Find out if there are any planned development projects in the area.

8. Property Analysis

Do a complete cash flow analysis—projection and calculation of the rental income against every expense. Familiarise yourself with terms such as ‘Cap Rate’, ‘Return on Investment’ (ROI), and ‘Gross Rent Multiplier’. Closely inspect the condition of the property itself and figure out what real estate repairs or renovations you’ll need to make.

9. Networking

Network with local real estate agents, other investors, and residents for leads and insights.

Funding The Dream Of Real Estate: How Various Strategies Stack Up

Traditional Mortgages: Consider such options as conventional loans, FHA loans and VA loans (if you are a veteran). Know the minimum down payment and interest rate.

Hard Money Loans: These are short-term, high-interest loans that will be used for quick acquisition and rehab deals.

Private Money Lenders: People often have more flexibility when borrowing from individuals than from a traditional bank.

Seller Financing: Under this collision, the property seller is turning out to be the lender, thereby lowering the vast dependence on banks.

BRRRR as in “Buy, Rehab, Rent, Refinance, Repeat: this dynamic system gives you the ability to grow your real estate portfolio using the equity from the properties you acquire.

Taking Care of Your Investment: From Tenant Selection to Residential Maintenance

Tenant Screening: I’m assuming you have the service right out of the leg iron; no suggestion that you have no screening, just trying to help you. You should, of course, always protect Fair Housing laws when you screen.

Lease Agreements: Prepare comprehensive lease documents covering all the important terms and legalities to save your property investment.

Rent Collection and Evictions: Create procedures for swift rent collection and learn the laws and numbers to evict when necessary.

Property Maintenance and Repairs: Establish a maintenance schedule, and have plans for emergencies and how to locate trustworthy contractors.

Hiring a Property Manager (Optional): If you’re too busy or you live a great distance from the property, you may want to hire a property manager. Learn what to consider when choosing a qualified property management company.

Common Challenges and Strategies for Overcoming Them

Vacancy Periods: Put measures in place to reduce downtime between tenants, for example, strong marketing and proactive tenant retention.

Problematic Tenants: Learn your legal recourse and how to prevent problems in the first place during the screening process.

Unexpected Repairs: Keep a good reserve fund for emergencies and unexpected costs so you can take care of major repairs without going into debt.

Market Downturns: Take the long view and make sure you have the financial staying power to survive swings in the economy.

Legal Issues: For any complex dispute or question of compliance, contact attorneys to preserve your investment.

We take a closer look at why multitasking is not an asset when it comes to investing in real estate (or anything for that matter).

Conclusion

All in all, beginner real estate investing is realistic, and there are many opportunities to do so. With the tactics provided in this guide, you can open the door to financial independence through real estate investment.

Call to Action

Get the ball rolling on your real estate dreams! Get the real estate investment checklist for FREE and subscribe to get the best tips!

Frequently Asked Questions

How much can I invest in real estate with little money?

The investment minima can range from hundreds to thousands of dollars, but some crowdfunding sites let you get started with just a few hundred dollars.

Is investing in real estate risky?

It is easy to take issue with the pros and cons of the matter, but here’s what I can clarify: Like any investment, real estate comes with risks — market fluctuations, tenant problems, etc. However, if properly researched and managed, these risks can be minimised.

When do you start to make money in real estate?

There is a range of returns based on the nature of the investment, but many investors start seeing cash flow from rental properties in just a few months from closing on said property.

TOKYO/HONG KONG: Asian stock markets were mixed Thursday as investors tried to digest the latest US inflation data and navigate shifting trade policies while technology companies pushed higher on Wall Street.

Particularly in the semiconductor sector, for pockets of optimism. Explore the latest market movements as Asian stocks dip after CPI data while tech gains: markets wrap, while tech stocks gain traction. Get the full analysis in our market.

CPI Data Takes Wind Out of Rate Cut Bets, Pharma’s Dropание

By and large, Asian shares inched down as traders adjusted the degree of interest rate cuts that the Federal Reserve would make. The US Consumer Price Index (CPI) minus volatile food and energy categories rose 0.2% from May – a modest figure, but one that provided a sign that some US companies are raising their prices to counter cost pressures due to new tariffs.

“While any tariff-induced jump to inflation is expected to be temporary, more higher tariffs being imposed means the Fed should still refrain from raising interest rates for a few months at least,” said Seema Shah at Principal Asset Management.

The cautious outlook encouraged traders to chip away at the odds of multiple Fed rate cuts this year, with the likelihood of a September cut now barely better than a coin flip, less than a 20% chance of two rate cuts this year. These revised policy bets typically bear down on riskier assets in Asia.

In a similar sector-specific drag, Asian pharma stocks fell following renewed threats by US President Donald Trump to impose tariffs on pharmaceuticals by the end of the month.

(Tech Outperforms as Chip Export Expectation Lifts Seoul)

Tech stocks across Asia, in turn, bucked the broader market decline, supported by favourable developments in the semiconductor sector. The Hang Seng Index in Hong Kong added 0.3 per cent, largely on the back of tech companies.

One big catalyst was word that US chip behemoth NVIDIA has received assurances from the US government that it will be able to resume exporting its H20 artificial intelligence accelerator chips to China.

This radical shift from an earlier position held by the Trump administration is considered quite bullish for the AI semiconductor supply chain and general US-China relations, especially when the two sides are negotiating levels of tariff amounts, which is a very positive development.

Taiwan Semiconductor Manufacturing Co. (TSMC), a critical NVIDIA partner and one of the largest global manufacturers of chips, TSMC, TSMC, Copper Tubes, TYO, 2330 c1, rose as much as 1.8% in Taipei after a media report suggested the company intends to build a second chip plant in Japan to diversify its production, including for chips used in the automotive sector.

South Korean tech companies including Samsung Electronics (005930.KS) and SK hynix (000660.KS) are also riding the wave, as Samsung Electronics ended 1.57% higher on Monday, a sign of broader optimism across the semiconductor sector.

Regional Performance Snapshot

Japan’s Topix was little changed as the Nikkei 225 edged 0.58% higher on July 15, supported by tech advances amid broader market wariness.

Australia’s S&P/ASX 200 lost 0.8 per cent, with the broader index weighed down by inflation worries.

Hong Kong’s Hang Seng index rose 0.3 per cent, boosted by its tech component. Chinese mainland markets, including the Shanghai Composite, fell slightly, down 0.1%.

South Korea’s Kospi fell 0.73% as broader worries about the economy overwhelmed technology sector optimism for the overall index.

Meanwhile the Japanese yen was 0.2% weaker versus the dollar, close to levels not seen since April, as the market considered the possibility of divergent monetary policy stances in the US and Japan. Gold, another traditional safe haven, nudged higher.

As global financial markets grapple with the prospect of inflation, interest rate assumptions and the changing world of trade, the gap between general market sentiment and the success of AI-powered tech stocks illustrates the themes dominating investment strategy decisions in mid-2025.

JGB yields have climbed to multi-decade geographical peaks, with the 10-year benchmark yielding more than 1.595% on Tuesday, July 15th, 2025, a level not seen since just before Halloween, October 2008.

Japan’s bond yields reach multi-decade highs amid rising fiscal concerns ahead of the upcoming election. Discover the implications for investors and the economy.

The spike in yields, especially on the far end of the curve, is a reflection of growing investor concern over Japan’s fiscal state and the prospects for additional government spending as preparation for the pivotal Upper House election on Sunday, July 20, heightens.

Record Highs and Market Instability

The 30-year JGB yield, a bellwether for long-term fiscal health, surged to an all-time 3.195% on Tuesday, and the 20-year yield rose to 2.65%, its highest since November 1999.

The rapid movement reflects rising strains in a Japanese government bond market that has been unusually stable in the past, anchored by the BoJ’s ultra-accommodative monetary policy. The rapid rise in yields is a troubling one for a country with the largest public debt-to-GDP ratio in the developed world, which comes in at around 250%.

Although the majority of Japan’s debt is held at home, any slackening in appetite from institutional buyers, who fund themselves at a spread over the JGB market, along with the BoJ’s ongoing gradual reduction of bond purchases, is increasing the vulnerability of the market.

Fears About the Economy Before the Election

The approaching race for the Upper House is a big factor behind the bond market sell-off. Japanese Prime Minister Shigeru Ishiba’s ruling Liberal Democratic Party (LDP) and its junior coalition partner Komeito are facing a difficult challenge, with local polls indicating they will struggle to win a majority in the chamber.

The possibility of a weakened ruling coalition or political continuity is stoking fears about continued budget generosity. Opposition parties, riding the wave of platforms that promise to tackle surging living costs, are pushing for steps like consumption tax advisory reductions. Such policies, although popular with voters, would also widen the fiscal deficit, making Japan’s already stretched finances even worse.

“As the volume is building around noise going into more fiscal spending, we took an underweight on Japan in general,” said Ales Koutny, head of international rates at Vanguard, speaking to the UK bond market’s headaches in recent years.

BoJ’s Delicate Balancing Act

The Bank of Japan is in a ticklish situation. Following its unconventional yield curve control (YCC) policy exit and, now, slow interest rate hikes (the cash rate sits at 0.5%), the central bank targets a sustained 2% inflation.

But ramped-up fiscal spending could unravel all of this and leave the BoJ with little choice but to engineer monetary tightening faster than the pace most households and firms would be happy with. Even though the Ministry of Finance tried to cool things down by stating that it intended to cut 20-, 30- and 40-year debt sales to help mend supply-demand imbalances, the real issue is fiscal.

“If a demand-less market continues and if investors see no rate hikes within this fiscal year, JGB volatility will go up, especially in the long end,” said Kentaro Hatono, a fund manager at Asset Management One.

Everything now depends on the result of Sunday’s election. A major defeat for the ruling coalition may lead to another sell-off in super-long JGBs as investors bet on a massively swollen government deficit.

The surge in yields, which have been rising steadily since the summer, has the potential to raise the cost of corporate loans and mortgages, in turn dampening domestic economic growth. Japan’s bond market readies for a volatile phase, with the election set to determine its fiscal course for years.

Have you ever registered for the trip of a lifetime, only to fret that unforeseen circumstances may force you to cancel? If so, you’re not alone. A number of travellers are also dealing with unknowns that have the potential to interrupt their travel plans and cause financial damage.

That’s where Cancel for Any Reason (CFAR) insurance comes in. In this article, we’re going to define what CFAR is, discuss how it works and its potential limitations, and help you figure out if it’s worth it for you or not.

Defining CFAR

Cancel for Any Reason (CFAR) insurance is a travel insurance plan add-on that provides the option to cancel for any reason, even if it’s not listed in the base policy.

While most travel insurance plans are triggered by specific named perils, a CFAR policy lets you cancel your trip for almost anything, offering you all but psychic protection when making travel decisions.

More Than Just Standard Trip Cancellation: CFAR Explained

Standard Trip Cancellation

Traditional trip cancellation insurance generally covers specific, named perils, like illness, injury, natural disasters or job loss. For instance, if you get sick before your trip, or a hurricane is threatening your destination, regular trip-cancellation insurance can reimburse you for your nonrefundable costs.

The CFAR Advantage

The advantage of CFAR is the ability it gives you to cancel for virtually any reason, even one that is not on the list in a standard policy. Here are some scenarios wherein you might be able to cancel with CFAR to the tune of something that isn’t protected by regular insurance:

Change of plans; you’re not in the mood to go.

Job or scheduling issues that arise unexpectedly.

Unsafeness or uneasiness related to a destination (e.g., political turbulence, health reasons, such as new outbreaks).

A friend or non-“covered family member” gets sick.

Your travel partner can’t make it, and you don’t want to travel alone.

Passport delays or visa issues.

Simply changing your mind.

How Does Cancel for Any Reason (CFAR) Insurance Work?

1. Add-on, Not Standalone

CFAR is usually an “upgrade” to a standard travel insurance policy, not a stand-alone policy. That’s because you’d be required to purchase a standard travel insurance policy first, and then buy supplemental CFAR coverage.

2. Purchase Timeline

It’s also worth mentioning that there’s a limited amount of time when you can buy CFAR; typically, it’s 10-21 days after you make your first trip deposit. That is, you must take action soon after booking your trip.

3. Insuring 100% of Trip Costs

The majority of CFAR plans stipulate that you need to insure 100% of your prepaid, nonrefundable trip costs in order to qualify for coverage. Therefore, you are fully protected if you need to cancel.

4. Cancellation Window

Most CFAR policies have a deadline for cancellation and it’s almost always a cancellation at least 48 hours before your planned departure.

5. Reimbursement Percentage

Unlike traditional cancellation policies, which would pay 100% of the cost of your trip if you have a covered reason to cancel, CFAR plans generally provide on 50%-75% of your insured trip costs.

6. Claim Process (Simplified)

In general, filing a CFAR claim is simple. You will need to submit a report of cancellation notice and other proof you consider necessary to justify your claim.

Advantages of Having CFAR Insurance

1. Unmatched Flexibility

The single greatest feature of CFAR is the incredible flexibility it provides. You can cancel for ANY reason up to the day before you travel and still get 100% of your money back (even if you have “I do not want to book a trip” coverage).

2. Financial Protection

CFAR protects a large portion of your non-refundable investment, so that in case you have to cancel, you don‘t lose the money you worked hard for.

3. Peace of Mind

CFAR insurance takes the stress and worry out of planning costly trips so far in advance. Plan your travel with confidence, knowing that you have a safety net.

4. Ideal for Uncertain Times

In a world of potential global uncertainty, CFAR is extremely timely today. It’s a cushion for travellers finding themselves in a precarious situation.

5. Protects High-Value Trips

CFAR can be most useful for costly international trips, cruises or tours – when the financial risk management is greater.

Downsides and Caveats to CFAR Insurance

1. Higher Cost

One of the downsides of CFAR is that it can significantly hike up the price, usually making the policy 40-60% more expensive than regular travel insurance.

2. Partial Reimbursement

It’s worth noting that CFAR doesn’t pay a 100% refund. In most cases, you will get only a portion of your trip costs back.

3. Strict Eligibility Requirements

CFAR policies have stringent eligibility requirements, including timing on when you bought the insurance and a requirement to cover the entire cost of the trip.

4. Not Available in All States/Regions

Both availability and terms may vary by insurer and location, and some states may not offer CFAR insurance at all.

5. Exclusions

“Any reason” is a big field, but there might be some or two rare exceptions. Don’t forget to read the fine print to know what’s not covered by a policy.

Who Should Consider CFAR Insurance?

1. Travelers with High Non-Refundable Costs

If you’re an individual or family whose flights, tours or accommodations are costly, then you may want to invest in CFAR to cover your investment.

2. Those with Unpredictable Schedules

Business travellers, people with high-pressure jobs, or those with family obligations that may be subjected to change could also appreciate CFAR’s flexibility.

3. People with Health Concerns

Traditional policies are good for illness that is not known of ahead of time, CFAR is a safety net for non health specific conditions, or pre-existing conditions (if no waiver is signed).

4. Anyone Seeking Maximum Flexibility

Those who appreciate the flexibility to change their mind without an egregious financial penalty stand to benefit most from CFAR.

5. Those Planning Far in Advance

The further in advance the planning, the more ability there is to absorb unanticipated events, so that was prudent (IMO) for the early planners to do.

How to Choose a CFAR Policy

1. Compare Providers

Compare CFAR policies from different insurance companies to ensure you have the greatest coverage for your unique requirements.

2. Understand Reimbursement Percentages

Seek the most variable percentage, such as 75%, rather than 50%.

3. Check Eligibility Requirements

Double-check that you meet the purchase timeline and full trip cost insurance requirements before purchasing a policy.

4. Read the Fine Print

Do remember to read the policy document for exact terms and conditions and any small print exclusions to avoid surprises at a later stage.

5. Consider Your Trip Details

Match that policy to your individual travel needs and your potential for risk, so you aren’t left without coverage.

Conclusion

In conclusion, travel insurance with CFAR allows for a special form of protection that affords flexibility and peace of mind to travellers. Though it may be an added cost, you’ll have peace of mind along with the ability to cancel for any reason. If you have a trip and want to protect your investment, look into CFAR.

Call to Action

Review CFAR benefits for your next journey, get a free quote now and learn more about TravelSafe’s comprehensive travel insurance coverage to support your trip. CFAR travel insurance, peace of mind travel, protect your vacation

Frequently Asked Questions

1. Can I purchase CFAR insurance after I’ve paid for my trip?

Normally you have to have purchased CFAR insurance in 10-21 days of you first payment.

2. Is CFAR available for pre-existing conditions?

Indirectly, CFAR allows you to cancel for issues which may be related even when you do not have a waiver in place, but it is not medical coverage itself.

3. Is CFAR insurance actually worth the extra cost?

It’s really down to your personal risk tolerance, the cost of the trip and how much flexibility you need. For lots of folks who spend time on the road, the peace of mind is worth the cost.

The US House is headed for key “Crypto Week” from today, July 14, 2025, with historic votes planned on a number of bills for digital asset legislation. This regulatory push is the result of attempts to implement clearer regulations for the developing crypto industry.

At the same time, U.S. home buyers continue to see stubbornly high mortgage rates that are making homes less affordable and discouraging the home buying process.

House’s ‘Crypto Week’ Begins

After years in which the crypto industry has called for clarity from regulators, the House is now preparing to take major steps. Members of Congress are set to vote on three pieces of legislation:

Digital Asset Market Clarity Act (CLARITY Act): This legislation would create a path for digital assets to be offered and sold as securities and identify how these assets are treated under securities law and is also meant to resolve conflicts between the SEC and the CFTC. This bill has been reported by both the House Financial Services Committee and the House Agriculture Committee with overwhelming bipartisan support.

Guiding and Establishing National Innovation for US Stablecoins Act (GENIUS Act): The GENIUS Act would establish the first federal statutory framework for payment stablecoins and would require payment stablecoins to be one-to-one backed by cash. This bill has already been approved overwhelmingly by the Senate, and House passage would send it directly to the desk of President Donald Trump, who might sign the first large crypto law into effect.

The Anti-CBDC Surveillance State Act: This bill would prohibit the Federal Reserve from issuing a central bank digital currency (CBDC), amid worries from certain lawmakers about privacy and potential government abuse.

The “Crypto Week” schedule reflects a desire among many in Washington D.C. to move forward with digital assets and establish the U.S. as a global leader in financial technology, an effort that President Trump is personally directing. Market participants are watching these votes closely for a more favourable and predictable environment to conduct a crypto business or invest in one.

Hotel Loans: Soness At Hotel Maturities Return – Mortgage Rates Still Near Highs

Meantime, the U.S. housing market faces high borrowing costs. Average rates for a 30-year fixed-rate mortgage increased slightly this week to 6.72 per cent, according to Freddie Mac data released on July 10, 2025, in what had been a five-week string of loosening. The average on the 15-year fixed-rate mortgage increased to 5.86%.

These stubbornly high levels — they’ve largely been between 6.5% and 7% for much of 2025 — are more a function of external economic conditions, such as the Federal Reserve’s monetary-policy setting and the movement of the 10-year Treasury yield. Yet despite some hopes for interest rate cutbacks later in the year, most economists say mortgage rates are likely to stay in the 6% to 7% range in the coming months unless there’s a dramatic change in inflation or economic reports.

The higher borrowing costs remain a major headwind for potential buyers, in particular for first-time buyers, and have led to a sales downturn in the housing market that commenced in 2022. There is plenty of demand for housing, but plenty of obstacles, too, both in the form of high interest rates and high home prices, which are keeping many on the sidelines. Refinance activity also has been tepid, with rates not low enough compared with the existing level of rates that many homeowners have.