Stock market investing is one of these places, and striking the proper balance of strong growth without the high price swings can be a difficult challenge. This is where large-cap funds come into play. They are a cornerstone of a good balanced portfolio, giving you that great point of growth and stability in the market.

In this post, invest wisely with large-cap funds that offer stability and growth potential. Learn how to build a resilient portfolio that withstands market fluctuations. If you are a new investor or just looking to reduce your risk while still building wealth, these funds are perfect for going down that less volatile path.

Part 1: What are large-cap funds? So, Who are the Giants of the market?

Large-cap funds are mutual fund schemes which predominantly invest in the shares of well-known, stable large-capital companies. A “large-cap” is a large market capitalization (the total dollar market value of a company’s outstanding shares). This list varies by country/market, but generally speaking, the S&P 100–200 of a given country’s most valuable companies.

Key Characteristics of Large-Cap Companies

Most times, they belong to top players in their sectors with good brand pull (Apple, Amazon, Tata or Reliance).

Stable & Mature: These firms have a history of performance that has been tested over time, are less exposed to downturns in the economy than smaller companies, and frequently have revenues from various sources.

Locust runes: the fact that they are larger and more frequently exchanged makes them easier to buy or sell without being hit in a big way.

Less Volatility: They do not have a complete immunisation to market movements but should be less volatile than mid- and small-cap companies, mostly due to their size and stability.

Regular Dividends: Large caps often distribute dividends; this provides consistent cash flows to the investors.

Part 2: The Dual Advantage, Stability and Growth

Because of their specific investment attributes, large-cap funds are an essential part of any long-term portfolio.

A Foundation of Stability

Resilient in Downturns: Many can also better weather economic recessions than smaller firms given their solid balance sheets, market share and geographical reach. Provides a similar sort of protection in more volatile times.

Relatively Lower Risk: Although no investment is risk-free, the performance of these large-cap funds is generally less volatile and more predictable than those of smaller, more speculative companies (a snowflake crashing).

Large Cap Funds are suitable for investorswith moderate and conservative risk profiles: If you look at this word, it looks simple that if you have moderate or conservative risk, but what it actually means is smaller volatility in the NAV, which reflects that if the benchmark declines by 100 points, your NAV will fall within the range of that performance.

The Engine of Growth

Secure form of appreciation: Large caps may not offer the kind of explosive growth that many small-cap companies might be able to, but they consistently provide a positive appreciation over the long term driven by continued business expansion and profitability.

Many large-cap companies are innovative, and that requires substantial investment in R&D to remain at the top of their respective markets well after generations.

Investing with Investors who have Captured Global Trends at Scale: This is a matter of scale, as having captured major global/economic trends and providing sustained growth over the long term.

Part 3: Strategic Integration, Investment In Large Cap Funds

Beginner: A Great Place to Start

Why it stands out: Large-cap funds have stability and are managed by professionals, which makes them a great starting point for first-time stock market investors.

Proper Strategy: Begin With a SIP, i.e., Those Who Have To Invest In Regular (Systematic Investment Plan). That way you end up buying at an average cost over time.

Advanced Investors: Portfolio Core

Why it’s a winner: Large-cap funds are the anchor to any portfolio, and this focused offering shows that core options can do more than hold their own.

Strategy: Buy large-cap funds for stability and ‘satellite’ mid-cap and small-cap funds (depending on risk tolerance) for higher growth potential and diversification.

Selection of a Large-Cap Fund

Quality Fund Manager: An experienced fund is generally the one whose manager can deliver returns over a period of time.

Choose funds with lower expenses: Ratio because this is the direct impact to your return

Performance History: Learn about the fund’s historical earnings and how it has performed through different market trends.

Is the fund well diversified: See if the portfolio of the fund across sectors is looking to minimize sector risk

Conclusion: The Wise Wealth Building Route

In short, large-cap funds invest in stable market leaders, which provide a powerful mix of stability via their antifragile nature and steady long-term growth.

Balance is key when it comes to these financial goals. Large-cap funds contribute that much-needed equilibrium and hence are a secure weapon in your hand to make you financially strong, which will also further increase returns.

Call to Action

Check out large-cap funds according to your requirements. Consult a financial advisor on what role large-cap funds can play in your portfolio and download the app to pick a mutual fund for beginners!

Frequently Asked Questions

1. Are large-cap funds tax-free?

It all depends on the tax laws in each jurisdiction and the lengths of time you were holding. For specific guidance, a tax advisor would be needed.

2. Large-cap funds or direct stocks of large companies?

It all depends on the tax laws in each jurisdiction and the lengths of time you were holding. For specific guidance, a tax advisor would be needed.

3. Large-cap funds or direct stocks of large companies?

Large-cap funds are better than direct investment in stocks for the reasons of diversification and professional management being possible, which adds a neat additional layer of security for most investors into other things being equal.

A depressing image of young people struggling financially, drowning in debt, and failing to save for retirement is often depicted in headlines. However, what if the narrative is evolving? Despite the stories you hear, an amazing number of young people are actually making some great decisions about saving for retirement.

To reach a wider audience — including policymakers, financial intermediaries and the general public — this article seeks to offer a hopeful, data-driven viewpoint on recent retirement savings trends. We will explain why this is happening, what we are doing and why it is working.

Explore why today’s youth are better at saving for retirement than ever before. Gain insights into their strategies for achieving long-term financial success.

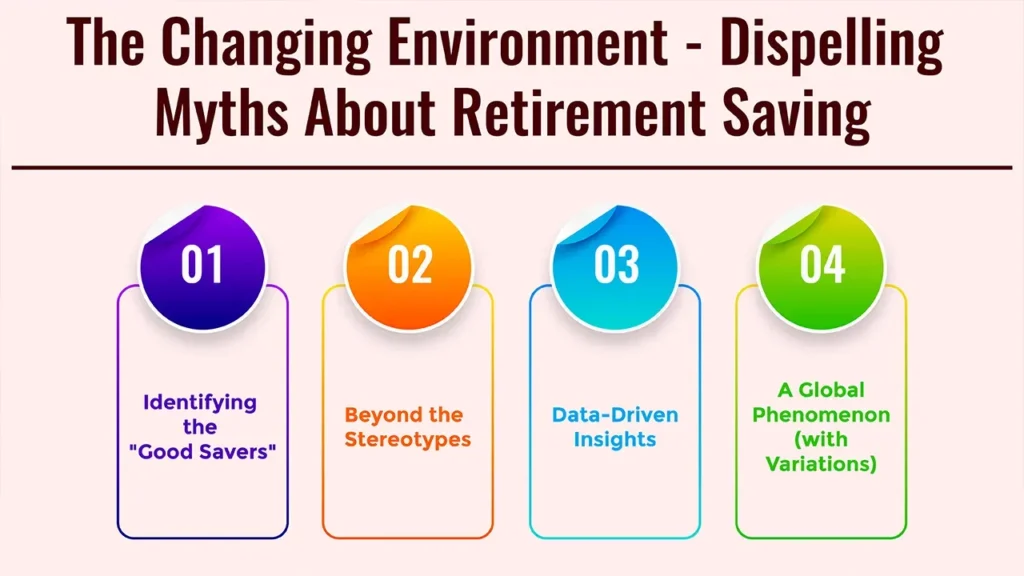

1. The Changing Environment: Dispelling Myths About Retirement Savings

Identifying the “Good Savers”

We’re not going to call out a particular generation, but there are some interesting trends happening among younger workers, specifically late Millennials and Gen Z, that suggest a move away from some of the ways retirement has been approached in the past.

“They are being more active in investing for their future, which is at odds with a lot of the narratives about how they’re buying avocado toast and eating out.”

Beyond the Stereotypes

Most of the negative stereotypes against the younger generation include over spending and complete non planning of finances. Now, new research indicates that such assumptions are out of date. Many young people are getting serious about their financial futures, and, as it turns out, saving for retirement in ways that defy popular stereotypes.

Data-Driven Insights

Recent surveys and research by several financial institutions and retirement plan providers show improved rates of retirement plan participation, higher contribution rates, when expressed as a percentage of pay, in retirement plans, and earlier starts among younger workers in many areas. For example, a study by the Employee Benefit Research Institute (EBRI) showed that younger workers are contributing to employer-provided retirement plans at a much higher rate than they were 10 years ago.

A Global Phenomenon (with Variations)

Despite the positive trend, the strength and the drivers of the trend may differ across nations and economic context. In certain parts of the country, young people face particular challenges, such as expensive living or student debt, which may make saving difficult. But the general move toward higher retirement savings by the young is apparent universally.

2. Key Drivers: What’s Causing This Shift

A number of circumstances are helping prompt this favorable change in retirement saving habits with the young.

Heightened Financial Awareness & Education

Post-Crisis Mindset

Anecdotal evidence also points to many entering the workforce in the wake of tremendous downturns in the economy, including the 2008 financial crisis and COVID-19.

Having experienced these situations, individuals felt more financially insecure and developed a need for stability, leading to having saving for retirement as the priority.

Digital Literacy & Information Access

In today’s digital age, financial information is readily available. Young people have unlimited access to blogs, podcasts, online courses and social media conversations about personal finance. This abundance of knowledge provides them the tools to make financial decisions about their future.

Peer Influence

There is more of a climate for open discussion of goals and strategies with peers. Younger individuals are just more likely to share personal tales of saving and investing, which fosters an encouraging atmosphere facilitating sensible financial conduct.

Early Financial Education

Better educational programs in schools and offered online have educated our young people about good financial decisions. That education shows them the value of saving for retirement at an early age.

3. Technological Enablement

Intuitive Saving & Investing Apps

The growing number of user-friendly apps that automate savings, provide fractional investing and streamline portfolio management has made it easier for young adults to save for retirement. These fintech products deliver convenient features for their financial necessities.

Automated Enrollment & Escalation

Increasing prevalence of workplace retirement plans with auto-enrollment and contribution-escalation take the pain out of saving. Retirement plans are automatically enrolled, with the share of contributions increasing automatically over the length of service without additional action.

Gamification of Finance

Adding gaming features makes saving and investing more interesting and goal-driven” for many apps today. It also teaches discipline and comes with the added bonus of motivating young people to set and work towards financial goals they can enjoy.

4. Changing Workplace Dynamics

Greater Gig Economy & Entrepreneurship

The gig economy and entrepreneurship offer flexibility, but also require self-reliance when it comes to planning for retirement. A lot of people are parking their own retirement savings, the younger workers realizing they will also have to save for their future financial independence.

Demand for Comprehensive Benefits

Workers who are younger frequently want a strong retirement plan and financial wellness programs from an employer. Firms with generous retirement benefits will be better able to recruit and retain skilled workers in such a tight job market.

Previous Experience of Defined Contribution Sponsorship

As fewer of them rely on the traditional economics of defined benefit pensions, younger workers are more and more exposed to defined contribution plans, and the responsibility for saving for retirement is falling squarely on their shoulders. This change promotes the behavior of proactive saving.

5. Evolving Life Priorities & Values

Delayed Milestones

Young adults are increasingly postponing the traditional trappings of adulthood, such as buying homes and starting families. The change can potentially mean more discretionary income to contribute to retirement sooner, making it easier to save for the future.

Concentrate in FIRE (Financial Independence, Retire Early) Movement

Movements like FIRE have gained steam, encouraging aggressive saving and investing from a young age. A lot of people are beginning to think about fire (financial independence, retire early), so young folk are getting a little more serious about saving.

Emphasis on Well-being & Security

Younger generations are paying more attention to long term financial security as part of overall wellness. They know that money matters are one part of their happiness.

6. Strategies Fueling Their Success

The successful savings of these generations may be traced to some particular strategies that help boost their retirement savings.

Aggressive Early Contributions

Optimizing Employer Match: Young savers focus on contributing to a workplace plan (such as a 401(k), superannuation (Australia), or NPS (India)) in order to receive the full employer match. This manoeuvre could add a substantial amount to their retirement nest-egg.

“Paying Themselves First”: They automate savings transfers from their paychecks straight into retirement accounts so they save before spending.

Using Big Raises: Applying much of the raises in pay directly to savings enables young people to beef up their funds for retirement while not being pinched.

Diversified Investment Approaches

Adopting Low-Cost Index Funds & ETFs: By using diverse, low-fee investment solutions that provide exposure to the market at large, young investors are able to keep costs down and potential returns up.

Worldwide Diversification: Understanding that young savers should invest globally for growth and risk reduction also enables them to develop strong portfolios.

Leveraging Tax-Advantaged Accounts: Making the most of contributions to tax-favorable retirement plans (like IRAs, Roth accounts, PPF in India, Pension Schemes) helps in optimizing their saving strategy.

Mindful Spending & Budgeting

Values-Based Spending: What young savers spend is a factor they consider, many of whom put experiences or values over possessions. This way, they are able to put more money towards saving.

Smart Debt: By paying off high interest consumer debt first, this will create capital for investing, which will help young people concentrate on retirement savings.

Technology and Budgeting: Budgeting becomes easy when tech-savvy young savers use budgeting apps to keep track of their expenses and keep them on the financial goals.

7. Remaining Challenges and Future Outlook

Yes, there are some encouraging trends, but it’s important to recognize the challenges that young savers continue to confront.

Economic Headwinds

Inflation, unaffordable housing and student debt (in certain areas) continue to pose high barriers for a lot of young people. These economic barriers may cast their ability to save effectively for retirement in a different light.

Inequality in Access

Not everyone has an employer who provides access to plans or other resources for financial literacy. This inequity can lead to differences in retirement savings across groups.

Longer Lifespans

The commitment to saving for potentially several decades in retirement (30+ years) means that even good savers still have a big job ahead. Young people need to prepare for the possibility that they will have to live off their retirement savings for decades.

Navigating Market Volatility

Maintaining discipline when markets fall will be important for long term success. Young investors will need to learn to navigate emotional markets and stick to their investment strategy during difficult times.

Nonetheless, the proactive attitude and digital literacy of this generation bodes well for the future of retirement security. Their flexibility, ability to learn and use technology puts these workers in a unique position to create significant long-term wealth.

Conclusion

So, in summary, a large chunk of the younger generation(s) is showing some stellar retirement saving behavior, fueled by increased personal-finance awareness, technology resources, changing priorities and well-targeted investment.

Those trends provide a potent lesson for all generations: disciplined, educated, tech-smart saving can mean a more secure and comfortable retirement. As more young people adopt these saving habits, they are not simply securing their own financial futures but also changing the retirement savings story.

Call to Action

Get your retirement savings off the ground (or keep them moving) today! Discover automated investing tools and more for long-term wealth building!

Frequently Asked Questions

1. Which generation is saving most for retirement right now?

This will be regional, but the late Millennials and Gen Z have made considerable changes to retirement savings behavior, and often improve on participation and contribution levels compared to prior generations.

2. What are potential best retirement savings strategies for young folks?

A proper approach would be maximizing employer matching contributions, automating savings, diversified investment and using tax advantaged accounts.

3. How much should you have saved for retirement by 30?

To the extent that there is a one-size-fits-most guideline, it’s worth aspiring to save at least 15 percent of your annual income for retirement by the time you’re 30, but individual circumstances will differ.

Do you believe that only big corporations get hit by cyberattacks? Think again. Small business once again is the favourite target, seen as such easy pickings. Your digital investments are in danger. Cybersecurity isn’t just a luxury; it’s a survival requirement for the small businesses that drive America’s economy in the digital age.

Safeguard your small business with essential cybersecurity strategies. Learn how to protect your assets and ensure your data remains secure.

The Digital Battlefield: Small Businesses are Easy Targets

Perceived Vulnerability

SMEs are frequently victims, as they might have less funds and inferior capabilities to defend themselves, as well as naïve thinking that “they are too small to be in the spotlight”.

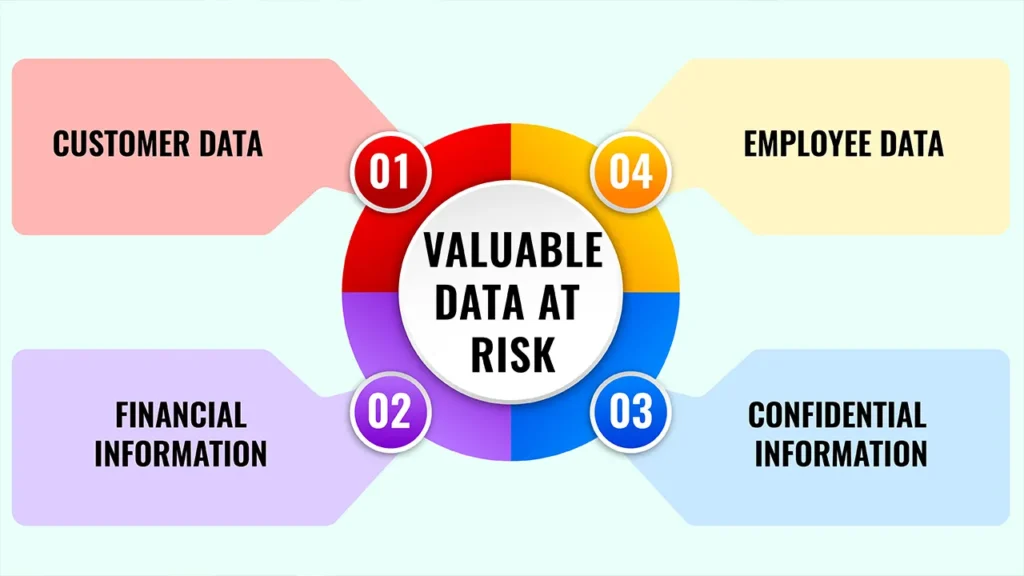

Valuable Data at Risk

Customer Data: Personal information, credit card numbers, contact information.

Financial Information: Bank accounts, transaction history, and invoices.

Confidential Information: Business plans, intellectual property, and trade secrets.

Employee Data: Payroll, personal records.

Consequences of a Breach

Monetary Damage: Theft or ransom, recoveries, legal expenses, fines.

Reputation damage: impact on trust with the customers, bad media/negative publicity, and long-term damage to brand perception.

Operational Disruption: Shut out of your business, out of service or reduced productivity.

Legal & Regulatory Consequences: Breach of data protection laws (e.g., GDPR and applicable local privacy laws in India).

Common Attack Vectors

“Phishing, malware/ransomware, weak passwords and unpatched software are the common threats.

1. Basic Principles of Cybersecurity

These are the first, non-negotiable steps every small business needs to take.

How it works: Prioritise strong, unique passwords for every account. MFA brings another layer of security (a code from your phone, for example) in addition to your password.

Actionable Takeaway: Invest in a trusted password manager. Enable MFA for all of your important accounts (email, bank, cloud), if you haven’t already.

Impact: Drastically diminishes the threat of unauthorised use.

Frequent Software Updates & Patching

How it works: Software developers often release updates to patch security weaknesses. Patching means applying these fixes.

Apply this advice: Ensure that OS (Windows, macOS), web browsers and all your business-critical applications are set to update automatically. Don’t ignore update prompts.

Impact: Blocks what are known as the zero-click hacks that have been lucrative for hackers.

Antivirus & Anti-Malware Software

How it works: It detects and removes malware, such as viruses, spyware and ransomware, across your devices.

Actionable Advice: Ensure you have a good antivirus product installed on all company devices (laptops, desktops, servers). Keep it updated and scan regularly.

Impact: Offers immediate protection against multiple digital threats.

Data Backup & Recovery Plan

How it works: Copies of your essential data are made and stored securely so that they can be restored after data is lost or a cyberattack occurs.

Actionable advice: Follow the 3-2-1 backup rule (3 copies, 2 media types, 1 offsite/cloud). Test your backups regularly.

Impact: Protecting your business by preparing for continuity and minimising data loss in a breach, hardware crash, or natural disaster.

2. Active Defense (Next-Level Defenses)

These modicums of securities make your security more and more solid.

Network Security (Firewall / Wi-Fi Protection)

How it works: Firewalls are designed to restrict the flow of data between your network and the internet. Strong encryption is employed to safeguard data in transit.

Application: Deploy A Firewall (Hardware Or Software) For Application #1-9 Would you like to add any others to this list? Lock down your Wi-Fi with strong passwords and WPA2/WPA3 encryption. Enable a guest Wi-Fi network.

Impact: Access to your network is not authorised.

Employee Training & Awareness

How it works: Human error is frequently the most vulnerable link. By teaching employees what to look for and how to identify potential dangers, you can make them the first responders.

Practical Tips: Regularly train on cyber awareness. Train employees on phishing, social engineering, and safe browsing. Create clear security policies.

Impact: Lowers the probability of successful phishing and insider threats.

Secure Remote Work Practices

How it works: Data and systems security when employees work remotely from home or other out-of-office sites.

Practical Tips: Use Virtual Private Networks (VPNs). Make certain that business devices are secured. Implement device management policies.

Impact: You now have a security perimeter outside the office.

Vendor & Third-Party Risk Management

How it works: Identifying and mitigating the security risks associated with third-party service providers that access your data or systems.

Practical Takeaway: Verify vendors’ security practices. Include security clauses in contracts.

Impact: Can avoid supply chain attacks and exposure of data through partners.

3. Responding to Incidents & Continual Improvement

Expecting the worst and always changing your defences.

Incident Response Plan

How it works: A written plan on the heritage holder’s next actions in the wake of a cyberattack or data breach.

Actionable Advice: Create a simple runbook: who to call, what to do (isolate systems, alert authorities/customers if necessary), and how to recover.

Impact: Reduces harm, accelerates recovery, brings the organisation into compliance.

Frequent Security Audits and Vulnerability Scanning

How it works: Monitoring your systems for vulnerabilities and verses and how attackers can gain access.

Practical Takeaway: Automate vulnerability scans or hire cybersecurity experts to carry out your audits.

Impact: Proactively closes security holes before they are exploited.

Compliance with Regulations (if applicable)

How it works: Compliant with data protection laws, such as India’s Digital Personal Data Protection Act, 2023 (if it applies to your business) or international laws (i.e., if you have global clients).

Actionable Advice: Know the data that you gather, maintain and process, and make sure your procedures are in line with any privacy laws.

Impact: Prevents hefty fines and earns customer trust.

Conclusion: Build a Business that Protects Your Future

In short, the basics of small business security include baseline best practices, active defence, and preparation for the inevitable. The threats we covered about the online space are relatively uniform; the only weapon small businesses possess is around-the-clock vigilance and intelligent cybersecurity strategies to safeguard themselves, their data, and their customers. It’s an investment in resilience.

Call to Action

So just get started with these security measures today! Download our free SME cybersecurity checklist and get a cybersecurity professional to protect your business!

Frequently Asked Questions

1. How Much Does Cyber Security Cost for a Small Business?

They can be quite expensive depending on the tools and services you use; there are also many solutions, some with no cost at all.

2. What is the top cybersecurity measure every SME must prioritise?

It is important to enforce strong passwords and multi-factor authentication (MFA), as it greatly mitigates the risk of unauthorised access.

3. Do I need cybersecurity liability insurance?

It is not necessary to have cybersecurity insurance, but it could offer coverage for losses suffered due to cybersecurity attacks and data compromises.

You’ve advanced in your career, you have experience, and your income is probably at its highest. In these challenging times, it’s time to speed up your financial dreams and provide for your future!!! Mid-career is a time when strategic personal finance planning can make a big impact, as you leverage both higher income and years of experience to improve your finances.

This column is for professional women in their 30s, 40s and early 50s who want to learn about money and be better investors both for themselves and for their families. Unlock your financial potential with expert mid-career planning tips. Accelerate your wealth goals and secure a prosperous future now!

The Mid-Career Financial Terrain: Opportunities and Obligations

Key Opportunities

Peak Earning Potential: Higher income provides more opportunity to save and invest.

Experience/Network: Use your experience & network for more income.

Longer Time Horizon than Late Career System: There is great time left for compounding to affect wealth.

Established financial habits (hopefully): Creating habits based on current budgeting and saving discipline.

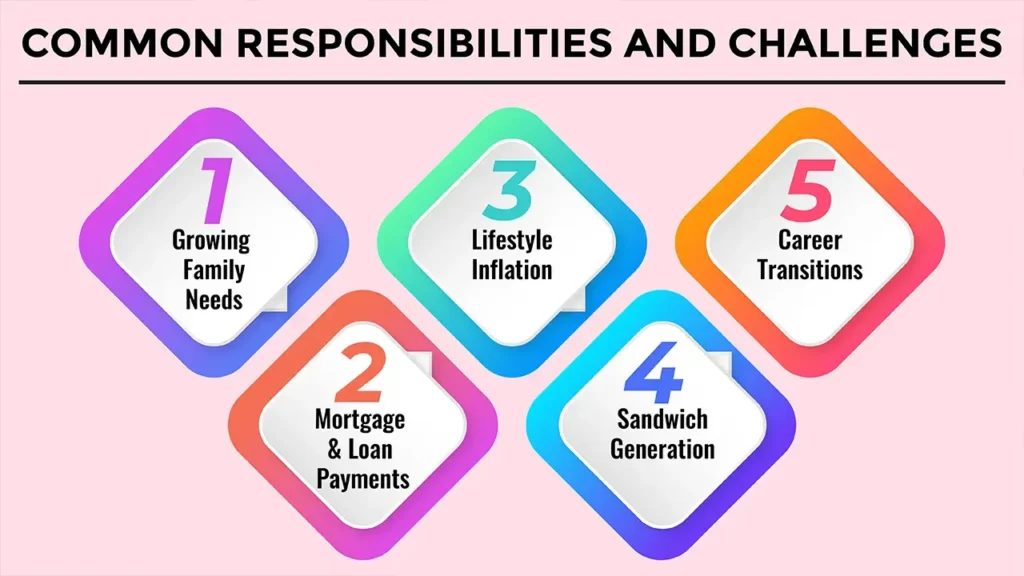

Common Responsibilities and Challenges

Growing Family Needs: Child’s education, wedding, medical expenses.

Mortgage & Loan Payments: Usually high debt loads.

Lifestyle Inflation: When you spend more money as you earn more money.

Sandwich Generation: Could be taking care of kids and elderly family members.

Career Transitions: Transitioning jobs or starting a new business venture.

Pillar 1: Cash Flow and Savings Optimization

Deep Dive into Budgeting (Revisited)

Take tracking a step further: Learn how to turn spending categories on their head for big savings. Locate “cost leaks” and how to slash them.

Aggressive Savings Strategies

“Pay Yourself First”: Set up automated savings upon income crediting.

Goal-Oriented Savings: Set aside money for specific goals (like your child’s education, your second home down payment and retirement).

Use Bonuses & Raises to Your Advantage: Personally save i.e invest a major percentage of any surprise money or raises.

Emergency Fund Reinforcement

Make sure you have a good-sized emergency fund with 6-12 months’ worth of essential living expenses aside, especially if you have growing dependants or less job security.

Pillar 2: Dealing With And Using Our Debt Wisely

Prioritize High-Interest Debt Elimination

Concentrate hard on eradicating all credit card debt, personal loans and any other borrowing at a high cost.

Mortgage Acceleration

Think of ways in which you can prepay your home loan (say, pay extra EMIs, increase your EMIs a little) and try to become debt-free faster. Explain the virtues of arriving at retirement day debt free.

Distinguishing Good vs. Bad Debt

Point out that some types of debt (a home loan, an education loan that allows you to earn more, for instance) can be a tool, while high-interest consumer debt is destructive.

Strategic Use of Debt (Cautiously)

For which it will be used to invest (raid) in such things as real estate or business expansion, etc., and only after fully assessing the risk involved.

Pillar 3: Sophisticated Growth Strategies

Reviewing Your Asset Allocation

Re-evaluate your risk appetite in relation to time until retirement and growing wealth. Realign the balance ratio between stocks and debt in your portfolio based on your new objectives and current market realities.

Diversification Beyond Basics

Equities: Contribute to a mix of sectors, market caps (large, mid, and small), and geographic locations (international exposure).

Debt Instruments: Consider fixed deposits, government bonds, corporate bonds and debt mutual funds for stability.

Real Estate: Direct property, REITs, or commercial real estate for diversification and income.

Alternative Investments (With Care): Give a passing nod to private equity, venture capital or gold for even greater diversification, but stress doing your homework and incurring more risks.

Maximizing Retirement Savings

Employer-Sponsored Plans (EPF, VPF, NPS): Invest more, especially if you get an employer match. Look at VPF for more tax-efficient savings.

PPF: Keep investing maximum yearly amount for tax free growth.

ELSS (Equity Linked Savings Schemes): If you want to save tax invoking Section 80C, with an element of equity in your investment.

Direct Equity/Mutual Funds (Without Retirement Accounts): To build wealth outside of retirement.

Investing Tax Efficiently: Plan to mitigate the impact of taxes on your investment gains and income.

Pillar 4: Protect Yourself, Your Wealth and Your Legacy

Comprehensive Insurance Review

Insurance Needs: Consider whether the family has enough life insurance considering family responsibilities, debts and future needs. Consider adequate term life insurance.

Health Insurance: Have adequate cover for you and your family, because health costs are shooting up, and critical illnesses are now `younger too! Explore super top-up plans.

Disability Insurance: Safeguard your greatest asset – your income – if you are unable to work.

Property & Asset Insurance: Cover your home, vehicles and other valuable assets sufficiently.

Estate Planning Essentials

Will & Nomination: Make sure that a valid will is in place and is kept up to date. Designate beneficiaries for all financial advisors.

Power of Attorney: Choose those you trust to make financial and medical decisions.

Territorial Imperative Succession Planning: Think about how to transfer wealth to the next generation in the most tax-efficient way.

Children’s Future Planning

Education Planning: Have separate funds (using SIP in an equity mutual fund) for higher education.

Wedding Fund: If you know you will eventually be getting married, save for it now!

Pillar 5: Monitoring and Continuous Adjustment

Regular Financial Reviews

Have an annual or bi-annual meeting with yourself, or your advisor, to do a “comprehensive financial review.” Track progress towards your goals.

Adapt to Life Changes

Modify your strategy for career changes, new dependents, health concerns or major market fluctuations.

Stay Informed

Stay current on the economy, changing tax laws, and investment opportunities.

Professional Guidance

You may also hire an SEBI-registered RIA or a CFP to get unbiased, thorough advice. They can help you steer through intricacies and remain on course.

Conclusion: Create Your Legacy, Protect Your Future

In short, mid-career financial planning is a combination of accumulation, protection and having a strategic growth plan. This phase provides a unique opportunity to establish financial independence and position the latter years for a comfortable retirement and beyond.

Call to Action

There is no time like now to step into your mid-career money. Get our financial planning checklist and meet with a financial professional who can help you confidently achieve your goals.

Frequently Asked Questions

1. What are some typical investing mistakes that young savers make?

Mistakes include not spreading investments around, underestimating the importance of retirement saving and not changing your financial plans as your life changes.

2. When should I start planning for my child’s college education?

It is best to start thinking about these costs as early as possible, ideally when your child is in the early years, with the opportunity of compounding growth in special education savings accounts.

3. Is it too late to change careers mid-career from a financial standpoint?

Changing careers may be tough to do, but it is possible and can pay off financially if it is strategically planned to account for potential income shifts and the need to invest in education or training.

Are you ready to move past borders with a Canadian virtual home for your real estate portfolio? Large real estate investments worldwide give you a world of opportunities you can use to improve your investment plan.

This article is for knowledgeable investors, HNW individuals, and capital allocators who are seeking opportunities outside of their local markets. We will also discuss the major advantages, challenges, tactics, and logistics of international real estate investments.

Why Go Global? The Strategic Imperative for International Real Estate

1. Enhanced Diversification

Diversified Market Cycle Exposure: Various national real estate markets operate on their own economic cycles, which act as a strong hedge against one’s domestic market downturn. For instance, while a European market is weak, the Indian market may be strong and vice versa.

Geographic Risk Mitigation: Diversification internationally mitigates concentration risk in any single economy or regulatory domain.

2. Access to New Growth Markets

Identify areas with potential for significant growth and up-and-coming economies or any demographic trends in a country that will result in larger returns than what you would have at home.

Some of these fortunes might find their footing in sectors or innovation hubs in foreign countries.

3. Capitalizing on Currency Fluctuations

A favourable exchange rate, upon entry or exit, can boost returns or contribute to additional income.

4. Inflation Hedging (Global Scale)

Values of property and of rents in different economies can serve as a hedge against inflation in diverse currency areas.

5. Higher Yields and Appreciation Potential

There might be some markets that provide better yields or capital growth than the home market, where it’s just very crowded.

Political and Economic Instability

Changes in government policies and macroeconomic instability (e.g., inflation, recession) may affect property values and rental revenues. Do some good due diligence on political stability and economic projections.”

1. Regulatory and Legal Differences

Differential ownership laws, taxes (local and international), zoning and inheritance laws and more can make for complex investment structures. Retaining local attorneys for this type of foreign investment is necessary.

2. Currency Risk

Negative currency moves can erode returns or add to costs. Think of FX hedging to hedge currency risks – or even consider exposing yourself to stable currencies or natural hedges (matching income/expenditure in the same currency).

3. Market Illiquidity

Real estate is typically an illiquid investment, and international markets even more so, particularly in less developed areas. A long-term investment horizon and good exit planning are important.

4. Taxation Challenges

Double taxation and capital gains, rental and property transfer taxes between two different countries can muddy your investment waters. Seeking out international tax advisors who can grasp your home country’s and target country’s tax laws is essential.

5. Cultural and Language Barriers

Communication can be challenged by cultural differences and not understanding local customs. Working with local authorities and linguists will help address these gaps.

6. Distance and Management

It’s tough to manage properties from a distance. Engaging with trusted local property managers or using passive vehicles can remove some of the overhead.

Strategies for International Real Estate Investments

Elite (Active & High Capital) Direct Ownership of the Asset

Residential Assets: Purchasing flats, villas or houses for rental income or capital appreciation is a common investment in steady, high-demand cities (like London, Dubai, New York, Singapore, Lisbon)

Commercial properties: Office buildings, retail space and industrial properties can bring in more returns but generally are more expensive to get into.

Development Projects: Investing in a new build or redevelopment can potentially generate greater returns but is high risk with a longer time horizon.

Direct Ownership Considerations: This approach involves having large amounts of capital, a deep understanding of local markets with active management (or management you can trust), and the ability to get through intricate legal and tax regulations.

Secondary & Second-Hand International Real Estate Exposure (Easier Bar and more Liquid)

Global REITs: Investing in REITs that are traded on stock exchanges (publicly traded REITs) and own and manage properties all over the world (office buildings, shopping centres, hotels, apartments and so on) provides a high level of liquidity, the benefit of owning and managing properties in numerous countries and property sectors around the globe and professional management.

Global Real Estate Mutual Funds/ETFs: Several funds invest in a diversified portfolio of international real estate companies and REITs for broad diversification and professional management.

International Real Estate Crowdfunding/Syndications: Investing in large international projects through pooling in funds with other investors on platforms, investors are able to get access to higher value international deals and generate passive income.

Important Considerations for Investing in the International Real Estate Market

Define Your Investment Goals

Clearly define what you hope to achieve, be it capital appreciation, rental income, diversification or tax benefits.

Thorough Market Research:

Macro Analysis: Research how the world’s economy is performing, geopolitical stability and large capital flows.

Analysis of economies per country: Analysis: GDP growth, inflation, interest rates, and demographics towards investment-friendly policies.

City/Region Insight: Delve into the local supply and demand, rental yield, infrastructure developments and property value trends.

Due Diligence on the Ground

Employ experienced agents, property managers, attorneys and accountants based in Japan. Wherever possible, you should view your target market and buildings.

Understand Tax Implications

Consult international tax specialists to help you through the double taxation treaties, capital gains tax, rental income tax, and the potential repatriation of dividends.

Secure Financing

Investigate possibilities of financing in the host country (domestic banks, foreign creditors) or use of home wealth.

Risk Management

Structuring currency hedges, managing political risk and planning exit strategies.

Exit Strategy Planning

Think about when and how you will ultimately unload the property (market conditions, tax considerations).

Case Studies and Emerging Markets (A Brief Review)

Stable Markets: More traditional safe havens in the US, UK, and Germany are still key markets for long-term stability and relative liquidity, albeit potentially with less on offer in terms of returns.

Growth Market: (e.g., Vietnam, Philippines) cities (in Latin America) or geographic areas (Eastern Europe) with higher growth but also carry higher risk.

Specialized Niches: There are few global trends, with opportunities in student housing, senior living, logistics/warehouses and data centres, for example.

In Conclusion: The World is Your Real Estate Portfolio

So, to win at global real estate investment, you have to know the benefit of the strategy and the key steps to get it right. Not without its complexities, global real estate can – with good preparation, investigation and professional assistance – become a transformational aspect of your investment portfolio.

Call to Action

Discover our world of real estate investment insights! Talk to our team of overseas property experts for your consultation today and get your free cross-border investment checklist!

Frequently Asked Questions

What is the minimum global real estate investment amount?

That really depends on the strategy, but with some crowdfunding platforms you can get started with as little as a few thousand dollars.

Is it a good idea to invest in foreign property for safety?

Sure, there are some not-so-nice parts of the globe, but some homework and intelligent choices can help minimize the various risks.

So how do foreign property taxes work?

Depending on the country, international property taxes can include several taxes such as capital gains tax, rental income tax and property transfer taxes. You should consult with a tax advisor.

Florida seaside property owners are experiencing a new kind of sticker shock as a new state law now requires at least $1 million in hurricane insurance on any home that is sited along the state’s hurricane-vulnerable coast.

The law for new policies and renewals that take effect on or after Jan. 1, 2026, is intended to build the state’s financial strength against another year like 2020, when large numbers of powerful storms battered the Sunshine State.

Bolstering Protection Amidst Rising Risks

The bill is a long-awaited reaction to Florida’s enduring property insurance disaster, as evidenced by soaring premiums, shrinking carriers and the increasing burden policyholders face from violent storms and the like.

Wind damage is typically covered by standard homeowners’ policies, though most exclude flooding – a significant gap, as most of the greatest natural disasters in the U.S. are flood-related.

And this new minimum of $1m means that coastal properties will have a fair amount more in coverage when it comes to damage that hurricanes can bring, be it wind or water.

But the FEMA National Flood Insurance Program (NFIP) only covered up to $250,000 for single-family homes – a sum which would not be enough for those owning high-value coastal real estate in Florida.

Although the new law is specifically targeted to windstorm coverage, it brings to the fore just how much the need for flood insurance in areas vulnerable to extreme weather systems continues.

Consequences for Homeowners and the Insurance Market

Lifting the requirement to $1 million would also have substantial impacts on both homeowners and the insurance industry:

High Fees: For a lot of homeowners along the coast, especially those with low existing coverage, this rule probably means a drastic spike in insurance premiums. Florida already has some of the most expensive home insurance in the country, in part because of its vulnerability to hurricanes.

Increased Financial Stability: The good news is that the law offers homeowners an added layer of protection and the opportunity to avoid deep financial despair if they suffer catastrophic hurricane damage. It is designed to prevent homeowners from being underinsured and unable to rebuild or repair damaged properties.

Market Corrections: Carriers will modify their products to avoid the return of a “standard” that in the real world is a minimum. This could prompt a re-examination of risk models for the region’s numerous coastal properties and, by extension, the types of properties that are insured — at what price. For some of the smaller insurers, that much coverage may be difficult to provide.

Emphasis on Mitigation: The law should add teeth to the call for hurricane mitigation. Homeowners who adopt impact-resistant windows, strengthened roofs and other storm-hardening features may also qualify for more favourable rates — or even become more appealing to insurers looking to keep their risk portfolios in check.

Broader Legislative Context

This new minimum coverage is one of many in a set of legislative provisions in Florida aimed at restoring stability in a sometimes erratic insurance market. Recent bills have aimed to:

Decrease AOB abuse and legal system manipulation, in particular.

Simplify claim management and provide for alternative dispute resolution.

Offer grants for home-strengthening changes – My Safe Florida Home Program.

Require flood insurance of Citizens Property Insurance Corporation policyholders regardless of their property’s flood zone (phased in by 2027 according to the cost to replace the dwelling).

Although designed to build a more stable insurance market, the $1 million minimum rule, for many coastal residents of the Sunshine State, is a cash-constrained reality. But as the 2026 season approaches, coastal residents will have to consult with their insurance agents to be sure they are in compliance — and to grasp the full effect of this new, higher standard for home protection against hurricanes.

You think you need a huge down payment and lots of cash to enter the world of real estate? Think again! The prospect of coming onto the property chain with a small amount of cash has never been more realistic.

This contribution will guide you through a number of tactics and concepts of low-capital investing so that you can take the first steps to create your real estate portfolio.

Ready to invest in real estate but short on funds? Explore our guide on starting with low capital and unlock the secrets to successful property investment.

Real Estate Landscape in the Age of Low Capital Investment

Dispelling Myths

A lot of people think that only rich people get into real estate, but creative financing and different investment vehicles make it so anyone can.

Why It’s Possible

There are new models, products, and investment structures that can drive down the cash required to invest in real estate up front and finally bring real estate investing within reach.

Understanding “Low Capital”

In this context, “low capital” might mean less than ₹5-10 lakhs, or even a fraction of that, relative to typical direct buys.

Important Priorities

If you have less cash to work with, you need to have your ducks in a row, a good credit score (for financing options), an emergency fund and be open to learning about the market.

Strategy 1: Passive and Indirect Investments in Real Estate

These are ways to invest in real estate without buying property with outright ownership and are ways with little upfront capital.

1. Real Estate Investment Trusts (REITs)

How They Work:REITs are businesses that own, operate or finance income-generating real estate. They are traded on exchanges, just like stocks, and you can buy shares in a portfolio of commercial or residential real estate.

Benefits for Those with Little Capital: High liquidity (able to sell shares), professional management of properties, and diversification between real estate sectors or geographies with a not-so-high investment amount (you can buy as little as one share).

Things to note: You can’t control the physical specs, and the performance of the assets might be affected by stock market movements.

2. Real Estate Mutual Funds and Exchange-Traded Funds (ETFs)

How They Work: These funds invest mainly in shares of real estate companies and REITs, creating a diversified basket of real estate-related securities.

Advantages for Small Capital: These provide IMMEDIATE diversification with very small investment OPERATE under Professional fund managers. Easy to enter and exit.

Considerations: You are indirectly exposed, with your position hinging on the fortunes of the underlying companies rather than the value of property merely. They also are subject to management fees.

3. Real Estate Crowdfunding & Fractional Ownership Platforms

How They Work: Investors pool small amounts of cash to collectively buy shares in larger properties or development projects (such as commercial buildings or holiday homes). You own a “fraction” of a bigger thing.

Adapted to Small Budget: They allow you to invest in high-value properties you cannot afford, provide diversification to different projects, and many times they generate you regular money from rents. Some platforms may also have entry points as low as ₹10,000 to ₹1 lakh.

Benefits: Investments on these platforms can be illiquid, while returns depend on the success of the project and platform fees. Platform and project due diligence is important.

Strategy 2: Strategic Funding is Done-for-Direct

These are methods where you buy the property outright, but you utilise some sort of financing option to minimise your upfront investment.

1. House Hacking (Owner-Occupied Multi-Unit)

How It Works: Buy a multi-unit property (duplex, triplex, or single-family with extra rooms) and live in one unit/room while renting out the others.

Low Capital Good: You’ll often be able to get owner-occupant loans with low down payments and better interest rates than you’d likely qualify for on investment property loans. And the rent from other units may cover much, or even all, of your mortgage, which means it’s possible to live for next to nothing.

Considerations: It requires living on the property; thus, you become your tenants’ landlord. It also involves mindful selection of a tenant.

2. Low Down Payment Loan Programs (FHA, VA, Government Loans)

How It Works: Though it’s not as commonly available for pure investment properties in India, one might find government housing schemes or some lender programmes that have lower down payment options, especially for first-time home buyers or if you are buying certain types of property (e.g., affordable houses). Look for plans such as Pradhan Mantri Awas Yojana (PMAY) if you are eligible.

Benefits for Low Capital: These initiatives lower the amount of upfront cash, which can help make homeownership (and possibly house hacking) more achievable.

Benefits: These tend to have strict qualification requirements, and some require mortgage insurance, typically only for owner-occupied residences. Research specific lender offerings.

3. Seller Financing (Owner Financing)

How It Works: In lieu of taking a loan out from a bank, the property seller agrees to function as the lender (typically with a lower down payment and interest rate agreed upon between the two of you).

Perks for Low Capital: It’s an escape from bank standards, and it can require a smaller down payment with more relaxed terms based on your own situation.

Drawbacks: You have to find a motivated seller who is willing to provide this, and interest rates could be higher than those for bank loans. Legal counsel is essential.

These are a little more hands-on, but they provide a high payback for a relatively low investment if applied well.

1. BRRRR (Buy, Rehab, Rent, Refinance, Repeat)

How It Works: You purchase an income-producing property below its value, rehab it to raise its worth, rent it out to generate income, refinance it to pocket your original investment (and ideally a little more), then start the cycle anew.

Advantages for Small Capital: Done rightly, you are able to reinvest the very first capital and grow another Arabic copy from it. The refi step effectively transforms short-term capital into long-term equity.

Considerations: This is a hands-on strategy that would have some project management skills in place – solid rehab cost estimating and a heavy ability to finance short-term for the purchase and rehab.

2. Rent-to-Own / Lease Options

How It Works: You rent a property with the right to purchase it at a predetermined price later. Some of your rent may be credited toward the down payment.

Benefits for Low Capital: Can get control of property with low upfront option fees, can see if property/neighbourhood is a fit for you before purchasing, and can build your equity over time.

Considerations: The option fee is almost always nonrefundable, and you need a contract, written generally, that holds up in court. Fine, lenders are banking on market conditions to change and for the pre-agreed price to become less attractive.

Essential Steps Before You Invest (Regardless of Capital)

You Must Learn Relentlessly: Get stuck into books, webinars, podcasts, other investors; just learn stuff!

Grow Your Network: Meet and build relationships with real estate agents, lenders, investors and contractors. Your network is your net worth.

Know Your Local Market: Study up on neighbourhoods, demand for rentals, property values, and future development plans.

Detailed Financial Plan: Know your budget, funds available, swap script and exit plan even with a low budget.

Start Small and Learn: Don’t go for the perfect deal right out of the gate. Concentrate on getting experience and learning the process.

Conclusion

In conclusion, there are some great ways to get started in real estate with little money. Affluent investors shouldn’t be the only ones excited about no monster front-load costs.

People get started in real estate because there is so much potential to invest in one of its greatest commodities: space. Let creativity, education and planning unlock that potential.

Call to Action

Begin learning these low-capital methods today! Get our free real estate crowdfunding guide and connect with a local real estate mentor!

Frequently Asked Questions

1. What is the least amount of capital required to start investing in real estate?

The minimum amount when it comes to the capital required can greatly vary depending on the type of investment strategy you choose; however, some of the crowdfunding platforms may let you start with just a few thousand rupees.

2. Low-capital real estate investments are riskier?

All investments have risk, but low-money plays can be less risky due to diversifying & getting a feel without a large financial commitment.

3. How are dividends paid for REITs?

As a general rule, REITs pay dividends based on the rental income that comes from the properties they own and operate, paying out most of that income to shareholders.

In a major diplomatic and business move, Jensen Huang, CEO of leading AI chipmaker NVIDIA, praised Chinese-developed AI models as “world class” today, July 16, 2025.

His comments at the opening ceremony of the third China International Supply Chain Expo (CISCE) in Beijing were reported one day after NVIDIA said it had received U.S. government permission to sell its H20 AI chips to China.

Explore how Nvidia’s Huang hails Chinese AI models as “world class”, emphasising their significant contributions to artificial intelligence innovation worldwide.

Praising Chinese Innovation

Huang singled out AI models created by Chinese companies such as DeepSeek, Alibaba and Tencent as “world class”. AI has become “essential infrastructure, like electricity”, he said, and is “transforming every industry, from scientific research and health care to energy and transportation and logistics.”

Meanwhile, the open-source AI landscape in China serves as a “catalyst for worldwide development”, according to the CEO of NVIDIA, who has welcomed the country’s rapid progress in AI development.

This endorsement by one of the world’s most influential technology leaders further solidifies the rapid maturation of China’s AI ecosystem, which has achieved big gains in generative AI, notably in non-reasoning models. Chinese producers also innovate, and models such as DeepSeek V3 0324 have become popular worldwide.

Navigating the US-China Tech Landscape

Huang’s visit to China, his third of this year, comes at a sensitive time for Nvidia, which is trying to steer its way through the knotty and often combative entanglement between the world’s two biggest economies, which are jostling for pre-eminence in AI and other state-of-the-art technologies.

The praise for Chinese AI models, along with the now-resumed sales of the H2O chips, indicates an attempt to salvage relationships and still serve the very important Chinese market investment strategies. The H20 chip, an adaptation of NVIDIA’s high-end AI accelerators, had been built to adhere to previous US export regulations.

In the wake of enhanced legislation, its sales were suspended in April 2025. But on July 15, NVIDIA said it received confirmation from the U.S. government that licences would be provided for the export of H20s into China, with shipments set to resume “shortly”. NVIDIA is building a new, fully compatible model RTX Pro GPU for the Chinese market for purposes of nickel AI applications.

Balancing Interests and Future Outlook

Huang has long maintained that curtailing exports would undermine U.S. leadership in AI by limiting American companies’ ability to sell to developers around the world, including the large number of AI researchers in China.

His recent contacts with US President Donald Trump and other top policymakers purportedly involved talking about not allowing American technology to become the worldwide standard. The freshly restored permission to sell H2O chips – plus Huang’s public praise of Chinese AI – is an example of the relatively carefully negotiated relationship that Nvidia must maintain.

It is designed to take advantage of the huge and fast-moving Chinese market while remaining compliant with US export controls. The political tactic also underscores the interconnected reality of the global AI industry and tech giants’ overtures to political enemies in the name of tech progress. In the months ahead, we will see how this delicate balance influences the state of the market and the overall landscape of AI globally.

Retirement is creeping up on you, and perhaps you feel the ticking of the clock. But the good news is this: your later career years can actually be some of the most impactful when it comes to turbocharging your retirement savings!

This guide is intended for people in their 50s and early 60s who are nearing retirement. This stage is so important because you have a lot working for you, including peak income potential, the ability to maximize your contributions to savings and retirement, and having an idea of what retirement feels like.

Navigate the complexities of late career retirement planning. Learn how to maximize your savings and ensure a comfortable retirement lifestyle.

The Landscape of Late-Career Retirement Planning Tap Qualified or not?

Advantages You Have

Greater Income Potential: Typically this is when you make the most money.

“Catch-Up” Contributions: Designed as a way for older savers to make up for lost time, you can contribute more to retirement accounts.

Less Debt (Maybe): Some people may have paid off — or paid down — their mortgage.

Sharper Vision: You probably have a clearer vision of your retirement dream.

Specific Challenges

Time Horizon: Time for Compounding to Wonder on Miracles.

Risk of Market Volatility: Less time to recover after a large market decline.

Health-Related Expenses: A significant worry that rises as we age.

Caregiving Duties: You might have to help ageing parents or grown children.

Insecure employment: The possibility of unexpected job loss is more threatening as retirement nears.

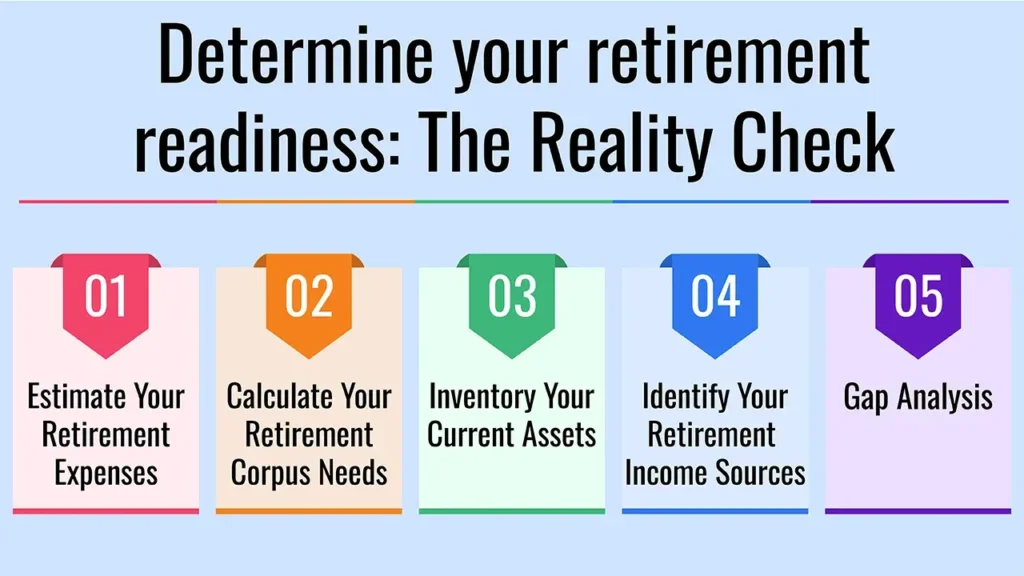

Step 1: Determine your retirement readiness: The Reality Check

Determine Your Retirement Date: When do you want to retire versus when can you afford to retire?

Estimate Your Retirement Expenses: Establish a comprehensive post-retirement budget to cover housing, food, health, travel, hobbies and entertainment. Keep in mind to adjust for inflation and the possibility that other spending niches could increase.

Calculate Your Retirement Corpus Needs: What target do you need to hit to sustain the lifestyle you want? It’s best to use rules of thumb, such as 25-30 times annual expenses, or a comprehensive retirement calculator.

Inventory Your Current Assets: Mention all retirement accounts (EPF, NPS, PPF, mutual funds, stocks, and real estate), savings and other investments.

Identify Your Retirement Income Sources: Include pensions (if any), NPS annuities, rent and systematic withdrawal plans (SWPs) from mutual funds.

Gap Analysis: Compare your estimated future needs with your existing savings and income sources to determine the “gap” you have to make up.

Step 2: Save and Contribute as Much as Possible

Supercharge Retirement Accounts

Catch-Up Contributions: Avail of such enhanced limits for above 50 category (following are the specific provisions concerning NPS, EPF or such other government/employer schemes in India)

Leverage EPF/VPF: To the extent applicable, enhance voluntary provident fund (VPF) for assured return and tax advantage.

NPS (National Pension System): Avail of tax benefits under Section 80CCD(1B) for investments over and above 80C.

PPF (Public Provident Fund): Invest the maximum every year and get tax-free returns.

ELSS (Equity Linked Saving Schemes): For 80C tax benefits along with exposure to equities, you may consider this.

Aggressive Savings

Trim your discretionary spending and figure out how to raise your savings, perhaps by paying yourself first via automatic transfers.

Convert Non-Earning Assets

Some things you should consider: Selling off your “extras” (like a second home or expensive cars) in order to ramp up your retirement savings.

Step 3: Refine Your Investment Plan

Risk Reassessment

Start the transition of your portfolio from high growth to balanced or conservative. And the aim should be to preserve capital and to grow income, not to see aggressive how-much-can-I-do growth.

Asset Allocation

Talk about the need to “rebalance” as you get older and reduce your exposure to stocks and increase exposure to debt/fixed income as retirement edges closer (i.e., you’ve got a 60/40 equity-to-debt ratio when you’re 40, but that should maybe be more like 40/60, eventually 30/70).

Income-Generating Investments

Debt Funds: For stability and moderate returns.

Fixed Deposits (FDs): Safe and sure income, but no tax benefits.

Senior Citizen’s Savings Scheme (SCSS): The SCSS is a government-guaranteed scheme for regular post-retirement income (if you were eligible).

Annuity Plans: Explain about them being the source of providing guaranteed income for life but also their drawbacks (no liquidity, low returns)

Tax-Efficient Withdrawals

Develop a withdrawal strategy for your various accounts (taxable and tax-exempt) to reduce your tax liability in retirement.

Step 4: Strategic Debt Management

Goal: Debt-Free Retirement

Pay off all high-interest debt (credit cards, personal loans) before retirement.

Mortgage Strategy

Strive to have your home loan repaid or a substantial debt reduction by the time you retire. This will leave you with a sizeable amount of cash flow in retirement.

Avoid New Debt

Be very cautious about taking on extra loans or expanding your debt as you near retirement.

Step 5: Critical Insurance and Healthcare Planning

Health Insurance

Make sure you have good health insurance that carries over into retirement. Think about a super top-up or critical illness policy to meet larger medical expenses.

Long-Term Care (LTC) Insurance

Although relatively infrequent in India compared with parts of the West, talk about whether it makes sense to provide for the possible cost of assisted living or nursing care.

Life Insurance Review

Reevaluate whether you still need term life insurance. If your dependants are no longer depending on your income, you may have the option of scaling back or completely dropping coverage in order to cut costs.

Step 6: Retirement’s Non-Financial Impacts on Households

Define Your Retirement Lifestyle

What are you going to do when you retire? Think about hobbies, travel, volunteer work, family or a passion project.

Social Connections

Be sure to make time for socializing in order to improve your quality of life.

Housing Decisions

Consider downsizing, moving to a less expensive part of the country or taking out a reverse mortgage (on which you should be very sceptical and very careful and should consult experts).

Part-Time Work/Encore Career

Could you work part-time in retirement for a little extra income?

Estate Planning

Review any will or power of attorney documents you have, and think about designating beneficiaries for your assets.

Step 7: Importance of Seeking Professional Help

When You Need a Financial Adviser

If you feel frazzled or have complicated financial circumstances, consider hiring a financial adviser to help with a personalized game plan.

What a Financial Planner Can Offer

A financial planner can help with goal identification, cash flow analysis, investment rebalancing, tax planning, estate planning and withdrawal strategies.

Choosing the Right Advisor

Identify SEBI-registered Investment Advisors (RIAs) or Certified Financial Planners (CFPs) who would provide independent advice and work on a fee-only model.

Conclusion

Focused action in these late working years really can make a difference in your retirement security and comfort level. And with the right moves today, you can be on the road to a full and financially secure retirement.

Call to Action

Begin your retirement checkup today! For help putting the finishing touches on your late-career strategy, seek advice from a financial planner — and download our retirement checklist!

Frequently Asked Questions

1. At age 50-something, is it even worth saving for retirement?

It’s never too late! Although you can’t save as long, there are ways to make the most of your retirement savings.

2. What are the best low-risk investments for someone about to retire?

For stability and predictable returns, you can look at vehicles such as fixed deposits, debt funds, government-backed schemes, etc.

3. What are the best health insurance options for retirees

Ideally, you should look at a comprehensive health insurance plan which includes hospitalisation and outpatient cover and also consider Super Top-up plans for additional cover.

Swiss Re Institute predicts that a potential impact of rising US tariff policy is slower global economic growth. The reinsurance colossus’ most recent “World Insurance sigma” report, published July 9, 2025 says these protectionist steps will not only hinder global GDP expansion but will also inhibit insurance premium growth internationally.

Explore how US tariffs are set to impact the global economy and insurance premium growth, as analyzed by Swiss Re. Stay informed on key economic trends.

Tariffs to Trigger “Stagflationary Shock”

The global average rate (real GDP growth) is expected to slow to 2.3% in 2025 and 2.4% in 2026, having stood at 2.8% in 2024. This slowdown has been primarily caused by the widening US tariff policy which is causing a ‘stagflationary shock’ to the US, and by extension the broader global economy, and is designed to obliterate policy uncertainty worldwide, the report states.

Jérôme Haegeli, Swiss Re’s Group Chief Economist, pointed to the short-term effect. “US consumers will be the most affected by US’ tariff policy and cut their consumption because of increased prices. This will in turn bear down on US growth which is largely driven by household consumption.” Swiss Re expects a slowdown in US GDP growth to just 1.5% in 2025 after 2.8% in 2024.

“Additional tariffs would lead to structurally higher inflation in the United States” as supply chains become less efficient and domestic industries face reduced competition from other countries, the report said. This mix of weaker growth and accelerating prices creates a thorny new world for businesses and consumers.

Insurance Premium Growth to Halve

There’s to be a ripple effect from a lightened global growth and increased uncertainty, and the insurance sector like no other will suffer. Global insurance premium development will slow down considerably to 2% in 2025, about half of the 5.2% seen in 2024, according to projections by the Swiss Re Institute. In 2026, a low partial recovery to 2.3% is expected.

Premium growth down in both life and non-life segments:

Nonlife growth of premiums is forecast to fall to 2.6% in 2025 from 4.7% in 2024 as competition in personal lines and softening market in some commercial lines.

The pace of growth in life insurance, in particular, will cool even more sharply, with premiums rising 1% in 2025, down from a 6.1% increase in 2024 — higher interest rates are set to moderate.

US tariff policy is another step toward increasing market fragmentation longer-term, which would decrease insurance affordability and availability, and thereby global risk resilience, Haegeli cautioned.

Trade barriers potentially leading to higher claims costs for insurers and supply chain disruptions, and cross-border flow of capital restrictions on reinsurers that may lead to capital allocation inefficiencies and higher capital costs and, ultimately, higher insurance pricing, are cited in the report.

Uneven Impacts and Emerging Opportunities

While the tone is in general cautious, the report states that the impact of tariffs on the insurance sector is likely to depend on geographic regions and lines of business.

US Motor Physical Damage This insurance sector is anticipated to bear the brunt of the tariff rise with auto parts and new/used cars prices surging and hence higher claims severity. Swiss Re predicts US motor damage repair and replacement costs will rise by 3.8% in 2025.

Our commercial property and homeowner and engineering lines in the US could also experience an increase in claims severity coming from higher costs for the intermediate goods, machinery, and commodities.

Tariffs outside the US are usually thought to be more disinflationary and could reduce claims pressure.

But the added uncertainty and economic disruption could also present opportunities, and credit and surety insurance that guard against economic disruption might be in higher demand. Alives could affect marine insurance as well, given changes to trade routes and supply chain realignments.

Notwithstanding the decline in premium growth, Swiss Re says that the overall profitability position of the global insurance industry remains robust, benefiting principally from ongoing investment income gains.

Yet the report is a stark reminder of how international trade policies and protectionism can have such widespread economic implications for wider global growth and important sectors, such as insurance.