Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

It is well known that the insurance industry relies on sound risk management and reinsurance functions as an essential tool in this process. How to Monitor and Adjust Ongoing Reinsurance Agreements As a general matter, insurers confront this problem in the form of balancing long-term stability with regulatory compliance and profitability.

Reinsurance enables insurers to share with other companies a portion of the risk that they have underwritten, thereby protecting themselves from catastrophic losses and truly balancing their assets. But it’s not enough to just make reinsurance agreements: constant surveillance and adjustments are essential for keeping the arrangements effective.

In this article we will show in detail how reinsurance contracts can efficiently be monitored, why adjustments are required, and the techniques by which insurers may maximize their strategies.

Reinsurance is not a simple deal but a dynamic relationship throughout market changes, loss experiences, and financial goals. Monitoring reinsurance agreements ensures that:

Without oversight, insurers could become overly exposed, in a dispute with reinsurers, and possibly in financial distress.

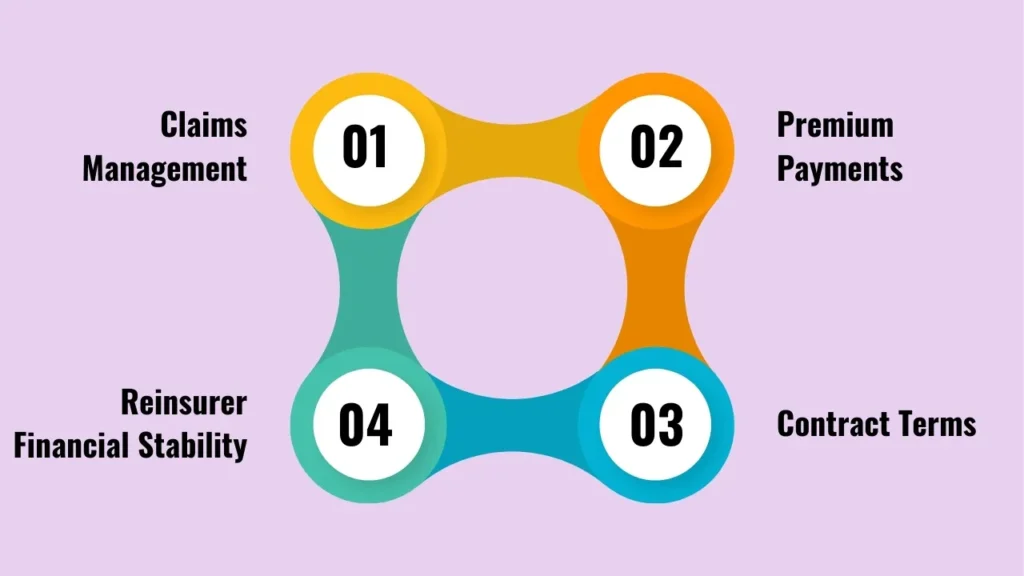

Claims are the most important trial for reinsurance contracts. Track how claims are submitted, processed, and reimbursed to be sure reinsurers meet their contractual obligations. Delays or arguments surrounding the processing of claims can put insurance companies under financial pressure.

2. Premium Payments

Superiorities must be closely examined to avoid misclassification. Late or underpaid premiums result in penalties or poor contract performance.

3. Contract Terms

Reinsurance contracts frequently contain specific conditions, exclusions, and coverage triggers. Reviewing these regularly helps to ensure that agreements continue to reflect the business requirements.

4. Reinsurer Financial Stability

A reinsurer has to be financially sound enough to pay claims. By watching credit ratings, annual reports, and solvency ratios, insurers can keep from becoming reliant on a weaker partner.

Include monthly or quarterly claims, premiums, and loss ratio reviews. This holds both the insurer and reinsurer responsible.

Monitor KPIs such as ceded premium ratios, combined ratios, and recovery timeliness. These signs are signs for early warning of imbalance.

Regularly audit to track compliance with regulations and contract terms.

4. Communication Framework

It helps to keep communication lines open between insurer and reinsurer so misunderstandings are fewer and strategies can more easily coincide.

5. Adjusting Ongoing Reinsurance Agreements

As with any financial instrument, reinsurance contracts need to adapt to market demands. Modifications are required whenever there is a change in the claims patterns or if there is an increase in market volatility.

| Area of Oversight | What to Monitor | Why it’s Critical |

|---|---|---|

| Claims Processing | Timeliness, accuracy, dispute resolution | Financial stability and cash flow |

| Premium Payments | Proper allocation, on-time payment | Prevent penalties and contraction strife |

| Financial Health | Insurer’s solvency, ratings, liquidity | Lessen counterparty risk |

| Compliance Obligations | Regulatory alignment and reporting | Legal and operational efficiency |

| Adjustments | Changes in contractual terms | Keep agreements up-to-date with business need |

That is why insurers typically employ their own dedicated reinsurance management software and advisory services.

These actions keep reinsurance contracts agile, compliant, and profitable.

Reinsurance is not just a process of spreading risk, it’s managing and sustaining durable relationships over the long term. Good oversight of reinsurance contracts will keep insurers covered from financial shocks and help them meet regulators’ and managements’ goals.

By adapting these documents as the situation demands, contracts remain current and lucrative. It is the value of this critical ability, to balance stability with flexibility, that lies at the core of effective reinsurance management for insurers.

Surveillance assures that claims are paid properly, premiums are billed correctly, and exposure is consistent with the carrier’s strategy.

Quarterly operating assessment/review; annual strategic review = maximum output.

Insurers could seek to renegotiate, transfer, or novate contracts or replace a reinsurer to lower the risk.

Sure, there can be additions or endorsements whenever risk profiles (or regulations) change.

Reinsurance management and analytics software and performance dashboards help ensure efficient oversight.