Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Retirement is creeping up on you, and perhaps you feel the ticking of the clock. But the good news is this: your later career years can actually be some of the most impactful when it comes to turbocharging your retirement savings!

This guide is intended for people in their 50s and early 60s who are nearing retirement. This stage is so important because you have a lot working for you, including peak income potential, the ability to maximize your contributions to savings and retirement, and having an idea of what retirement feels like.

Navigate the complexities of late career retirement planning. Learn how to maximize your savings and ensure a comfortable retirement lifestyle.

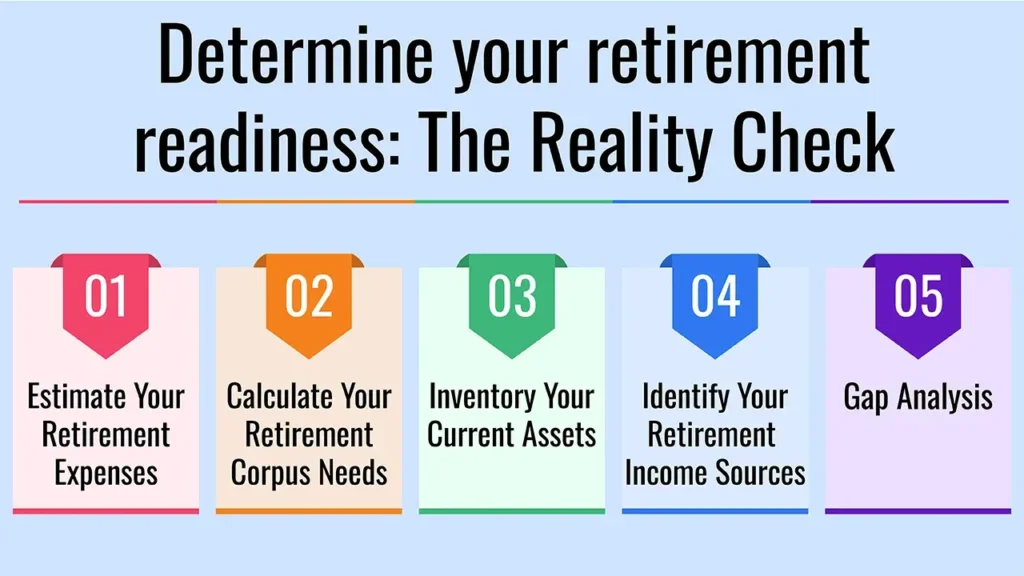

Determine Your Retirement Date: When do you want to retire versus when can you afford to retire?

Trim your discretionary spending and figure out how to raise your savings, perhaps by paying yourself first via automatic transfers.

Some things you should consider: Selling off your “extras” (like a second home or expensive cars) in order to ramp up your retirement savings.

Start the transition of your portfolio from high growth to balanced or conservative. And the aim should be to preserve capital and to grow income, not to see aggressive how-much-can-I-do growth.

Talk about the need to “rebalance” as you get older and reduce your exposure to stocks and increase exposure to debt/fixed income as retirement edges closer (i.e., you’ve got a 60/40 equity-to-debt ratio when you’re 40, but that should maybe be more like 40/60, eventually 30/70).

Debt Funds: For stability and moderate returns.

Develop a withdrawal strategy for your various accounts (taxable and tax-exempt) to reduce your tax liability in retirement.

Pay off all high-interest debt (credit cards, personal loans) before retirement.

Strive to have your home loan repaid or a substantial debt reduction by the time you retire. This will leave you with a sizeable amount of cash flow in retirement.

Be very cautious about taking on extra loans or expanding your debt as you near retirement.

Make sure you have good health insurance that carries over into retirement. Think about a super top-up or critical illness policy to meet larger medical expenses.

Although relatively infrequent in India compared with parts of the West, talk about whether it makes sense to provide for the possible cost of assisted living or nursing care.

Reevaluate whether you still need term life insurance. If your dependants are no longer depending on your income, you may have the option of scaling back or completely dropping coverage in order to cut costs.

What are you going to do when you retire? Think about hobbies, travel, volunteer work, family or a passion project.

Be sure to make time for socializing in order to improve your quality of life.

Consider downsizing, moving to a less expensive part of the country or taking out a reverse mortgage (on which you should be very sceptical and very careful and should consult experts).

Could you work part-time in retirement for a little extra income?

Review any will or power of attorney documents you have, and think about designating beneficiaries for your assets.

If you feel frazzled or have complicated financial circumstances, consider hiring a financial adviser to help with a personalized game plan.

A financial planner can help with goal identification, cash flow analysis, investment rebalancing, tax planning, estate planning and withdrawal strategies.

Identify SEBI-registered Investment Advisors (RIAs) or Certified Financial Planners (CFPs) who would provide independent advice and work on a fee-only model.

Focused action in these late working years really can make a difference in your retirement security and comfort level. And with the right moves today, you can be on the road to a full and financially secure retirement.

Begin your retirement checkup today! For help putting the finishing touches on your late-career strategy, seek advice from a financial planner — and download our retirement checklist!

It’s never too late! Although you can’t save as long, there are ways to make the most of your retirement savings.

For stability and predictable returns, you can look at vehicles such as fixed deposits, debt funds, government-backed schemes, etc.

Ideally, you should look at a comprehensive health insurance plan which includes hospitalisation and outpatient cover and also consider Super Top-up plans for additional cover.